")

")

Trick or treat? RBA hints at scary supersized hike or an interest rates pause

The central bank's latest board minutes reveal it came tantalisingly close to raising rates by double the amount they eventually settled on this month, but in the same policy meeting raised the possibility of leaving the official cash rate on hold.

The Reserve Bank of Australia has left Australian mortgagees guessing what its next interest rates move is likely to be, with the release of their decision-making process covering all bets.

On the one hand, the RBA Minutes on Tuesday (15 November) made it clear they have come perilously close to unleashing a supersized 0.5 per cent hike two weeks ago. At the same time, RBA Governor Philip Lowe and his Board have said they may keep rates on hold while the seven successive rate increases take effect.

The RBA board this month lifted its key cash rate by 0.25 of a percentage point, taking the cash rate from 0.1 per cent in May to 2.85 per cent now, the fastest pace of increments in decades.

The shock of a 7.3 per cent annual inflation rate result in September very nearly prompted the RBA to go large with its rate rise this month, yet it also raised the prospect of giving borrowers a breather in December.

“Acknowledging the (inflationary) uncertainty, members did not rule out returning to larger increases if the situation warranted,” the Minutes of the Monetary Policy Meeting of the Reserve Bank Board noted.

“Conversely, the Board is prepared to keep rates unchanged for a period while it assesses the state of the economy and the inflation outlook.

“Interest rates are not on a pre-set path.”

Before the release of the minutes, investors were rating a 59 per cent chance the RBA would make it eight successive rate rises on 6 December. The central bank is then scheduled to take its traditional January break before its next rates meeting on 7 February.

With one eye firmly on other international economies, the RBA offered a second glimmer of hope to borrowers that they may hit the pause button, at least temporarily.

“In their discussion, (board) members noted that many major central banks had been raising policy rates quickly and were more likely to err on the side of doing too much rather than too little.”

With inflation still an international issue, many still expect a 0.25 per cent rise in December rise to precede a holding pattern in early 2023.

The board’s tightrope call on whether it should have lifted rates by 0.5 per cent this month lends support to that view.

As was the case in October, the arguments for an increase of 50 basis points stemmed from the current inflation environment and the upside risks to inflation from the labour market, rents and energy costs.

“Inflation was at a 30-year high in advanced economies and was broadly based,” the RBA noted.

“The tightness of the labour market, with the unemployment rate at its lowest level in almost 50 years, suggested wages growth would pick up further.

“A risk to the inflation outlook over the medium term was the possibility that price- and wage-setting behaviour would shift, resulting in domestic inflationary pressures becoming more persistent.”

Lack of energy

The RBA minutes made it clear about where it saw inflation emanating.

“Members discussed the outlook for energy prices, noting the very large forecast increases in electricity and gas prices that had been outlined in the October 2022–23 Australian Government Budget, and which had been factored into the Bank’s revised inflation forecast.

“Members noted the likelihood of second-round effects on inflation from higher energy prices.”

Higher electricity and gas prices were expected to slow the return of inflation to the target range.

“Any new supply shocks – including in energy markets – could push inflation even higher than forecast in Australia,” the RBA Board said.

The Bank’s latest forecast is for CPI inflation to reach 8 per cent by the end of 2022 (revised up from 7.75 per cent previously) and for underlying inflation to be 6.5 per cent (revised up from 6 per cent previously). Both headline and underlying inflation were then expected to decline to a little above 3 per cent by the end of 2024.

On the housing supply issue, the news for renters not good.

The RBA observed that recent rapid growth in advertised rents had led to a pick-up in rent inflation across the country, which was forecast to continue.

“On the other hand, demand for new detached housing had fallen considerably since the start of 2022; prices for established housing nationally had declined by around 5 per cent since their peak in April.”

Fixed rates take flight

The RBA’s uncertainty over the direction interest rates from here is shared by Australian households, many of whom are facing mortgage stress, while the property market sees buyers and sellers in a standoff as they try to time the market.

But one apparent certainty in an uncertain economic environment is the upwards trajectory of fixed rate loan interest rates.

ANZ on Wednesday (16 November) hiked fixed rates by up to 0.30 percentage points for owner-occupiers and property investors.

ANZ is not hiking fixed rates in isolation. Analysis of the RateCity.com.au database shows over 40 lenders have hiked at least one fixed rate in the last month.

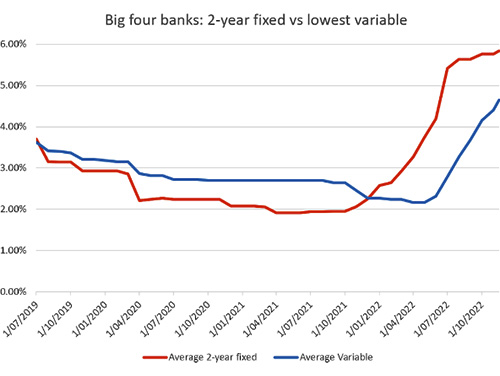

Source: RateCity.com.au. Rates are the lowest rates for owner-occupiers paying principal and interest. Some LVR requirements apply.

RateCity.com.au research director, Sally Tindall, said “fixed rates continue to defy gravity.”

“While the size and pace of the fixed rate hikes have slowed considerably, there’s little sign of a market-wide turnaround just yet,” she said.

“After 2.75 percentage points of cash rate hikes, the gap between fixed and variable has narrowed, however, there’s still a considerable amount of daylight between the majority of these rates.

The average gap between the big four banks’ lowest two-year fixed rates, and their lowest variable rates, is 1.19 percentage points.

“Interestingly, CBA and Westpac’s four-year fixed rates, at 5.49 per cent and 5.64 per cent respectively are lower than their two- and three-year rates for owner-occupiers.

“These longer-term rates appear to be a bid from Australia’s two biggest banks to lock in customers for the next four years.

“While fixing can provide some customers with certainty to help them budget, anyone looking to lock in their rate would do well to shop around.”

")