")

")

RBA lifts interest rates for seventh month in a row

Australian mortgage holders have been dealt a seventh consecutive rate hike and can expect to pay hundreds more in interest per month following the RBA's Melbourne Cup day announcement.

The Reserve Bank of Australia (RBA) has responded to persistent inflation with another 0.25 per cent rise in the official cash rate.

On the same day protesters tried to sabotage Flemington racecourse and the Melbourne Cup, inflation has sabotaged the economy and driven interest rates to 2.85 per cent.

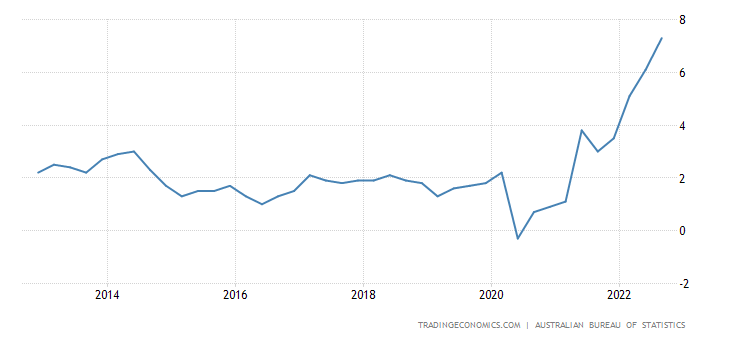

The inflation horse has clearly bolted, having climbed to 7.3 per cent in quarter three of 2022, from 6.1 per cent in the second quarter of 2022, and above market forecasts of 7.0 per cent.

Economists had unanimously backed an interest rate rise on Melbourne Cup Day, although opinion had been divided on whether it would be a standard 0.25 per cent rate hike or a supersized increase.

Retail spending is only fuelling the inflation spiral that is in turn propelling the interest rates juggernaut.

The Australian Bureau of Statistics on Monday (31 October) released its retail trade figures showing sales had increased another 0.6 per cent month-on-month (for September) and by 17.9 per cent compared to a year ago.

For borrowers, the seventh consecutive rate rise will mean a borrower with a $500,000 loan before the hikes started in May could soon be paying a total of $760 more a month. This month’s increment adds another $74 per month onto that debt level.

CBA: +0.25% in Nov, +0.25% in Dec, peaking at 3.10%. Two 0.25% cuts in Aug and Nov 2023.

Westpac: +0.25% in Nov, +0.25% in Dec, peaking at 3.60% in March 2023. Four 0.25% cuts in 2024.

NAB: +0.25% in Nov, +0.25% in Dec, peaking at 3.60% in March 2023.

ANZ: +0.25% in Nov, +0.25% in Dec, peaking at 3.85% in May 2023. Two 0.25% cuts in 2024.

International issue

It’s not just the Melbourne Cup field that has an international flavour.

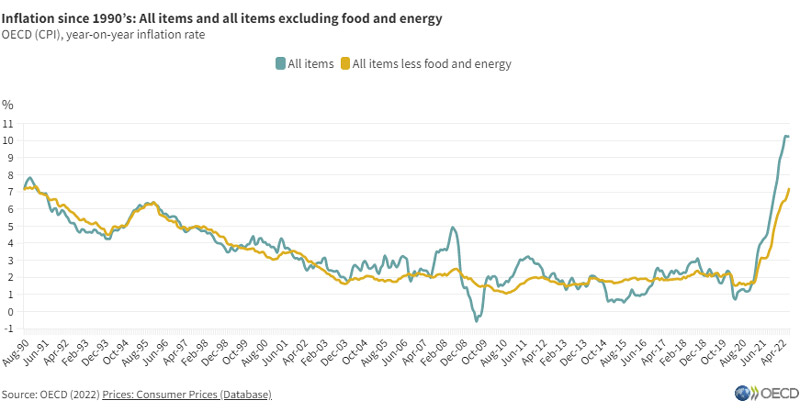

The inflation rate in Australia is actually relatively low compared to many Organisation for Economic Co-operation and Development (OECD) countries.

Australia’s high inflation rate is largely the result of global economic influences, from the war in Ukraine, high energy prices around the world, and recovery from Covid’s emergency economic stimulus measures.

Inflation in Germany, Europe’s biggest economy, shot up to 11.6 per cent. In Italy, it rose to 12.8 per cent, while France’s rate climbed to 7.1 per cent. US consumer price inflation, by comparison, was 8.2 per cent in September.

In May 2020, the OECD inflation rate was just 0.71 per cent. It has since taken a near-vertical trajectory to its current 10.25 per cent.

In announcing the latest rate hike, RBA Governor Philip Lowe said that, as is the case in most countries, inflation in Australia is too high.

“Over the year to September, the CPI inflation rate was 7.3 per cent, the highest it has been in more than three decades.

“Global factors explain much of this high inflation, but strong domestic demand relative to the ability of the economy to meet that demand is also playing a role.

“Returning inflation to target requires a more sustainable balance between demand and supply,” he said.

More pain ahead

While savers will be rejoicing about the increase in interest rates, there’s seemingly much more pain ahead for borrowers.

Mr Lowe and the RBA quietly lifted their expectations around inflation in the latest Monetary Policy Decision.

Mr Lowe said they had decided to up the rate by 25 basis points because inflation is now forecast to hit eight per cent by the end of the year.

Australian inflation rate over 10 years:

Interest rates that are already at a nine-year high are tipped to rise further over coming months and into 2023.

“The Bank’s central forecast is for CPI inflation to be around 4.75 per cent over 2023 and a little above 3 per cent over 2024.”

“The Board expects to increase interest rates further over the period ahead.

“It is closely monitoring the global economy, household spending and wage and price-setting behaviour.”

Speaking later on Tuesday in Hobart at an RBA Board dinner, Mr Lowe branded inflation “evil”.

“It is a scourge. High inflation devalues your savings. It worsens inequality in our society and it undermines our living standards. It hurts us all by impairing the functioning of our economy,” he said.

“If this were to happen, the evil of inflation would be with us for longer and the eventual increase in interest rates needed to bring it down would be greater,” he said.

“This would increase the risk of a severe recession and a sharp rise in unemployment.

“It would be much better to avoid such a costly outcome and so we have acted strongly to avoid it.”

This cash rate increase will be significant for many homeowners who took advantage of cheap loans two years ago and could create even more mortgage prisoners.

People who got an ultra-low 1.79 per cent mortgage in 2020 will be moving onto a much higher variable rate and will be looking to refinance.

Lance Goodman, CEO of Compare Club, said it’s also going to get harder to refinance a home loan.

“For example, Sydney property prices are down 8.1 per cent over the past year, somebody who had a 70 per cent loan-to-value ratio (LVR) 12 months ago may now be edging closer to an 80 per cent LVR, which would mean they’d also have to pay an additional cost of Lenders Mortgage Insurance when they refinance,” he said.

“So, somebody looking to refinance a $600,000 mortgage with an LVR of just over 80 per cent could be looking at an additional $3,000 in Lenders’ Mortgage Insurance.

“Some lenders also take LVR into account when setting their interest rates, so another cash rate increase, combined with a continued decrease in property prices, means refinancing is only going to get more difficult.”

Renters collateral damage

While it’s homeowners footing the bills on the mortgage debts, renters are also set to feel the heat as investors shy away from the property market at a time when a lack of rental properties has driven vacancy rates to record lows around the country.

Property Investment Professionals of Australia’s (PIPA) Chair, Nicola McDougall, said the significant uptick in rates in such a short period of time has resulted in many borrowers, and especially investors, not being able to secure lending to add to their portfolios – or even purchase one rental dwelling.

“Many of these borrowers are stuck on the sidelines due to the servicing buffer of 300 basis points still being applied to lending applications, even though interest rates are significantly higher now than when APRA announced the measure in October last year,” Ms McDougall said.

“Of course, there is an element of déjà vu about this situation, with a similar circumstance occurring when caps on investment lending as well as higher rates more generally for investors wiped out lending possibilities for many during the 2010s.

“The flow-on effect from that decision was the continued reduction in investment activity – especially from 2017 – which hit rock bottom at the start of the pandemic, when the percentage of investors active in the market was just 22.9 per cent compared to a long run average of nearly 35 per cent.”

A staggering 16.7 per cent have also sold at least one dwelling over the past two years, Ms McDougall said.

“While opportunities clearly exist for homebuyers and investors in the current market, it they are unable to secure finance then we are likely to see a further reduction in prices as well as sustained downward pressure on vacancy rates for some time yet,” she said.

")