")

")

Fewer loans and more distressed sales as interest rates bite

Escalating interest rates are driving people away from the property market, with new home loans and building approvals plunging and distressed sales by indebted homeowners rising sharply.

Rising interest rates are deterring potential borrowers and driving many existing ones to the financial brink.

Mortgage lending in Australia has fallen for the fourth month in a row, with first-home buyer loans fell 9.3 per cent, while investor loans fell 6 per cent during the period, the Australian Bureau of Statistics (ABS) revealed on Wednesday (2 November).

For existing borrowers, the continual run of interest rate hikes is driving many to sell their homes at a loss as they struggle to meet higher loan repayments.

The number of distressed listings has risen by more than 15 per cent since interest rates started climbing in May, according to data from SQM research.

Queensland saw the largest increase in the number of distressed sales, up 26.7 per cent, or 588 homes, to 2,791, according to SQM Research. Distressed listings spiked 38.7 per cent to 1,265 in New South Wales, while Victoria’s share of distressed listings jumped 1.49 per cent to 765.

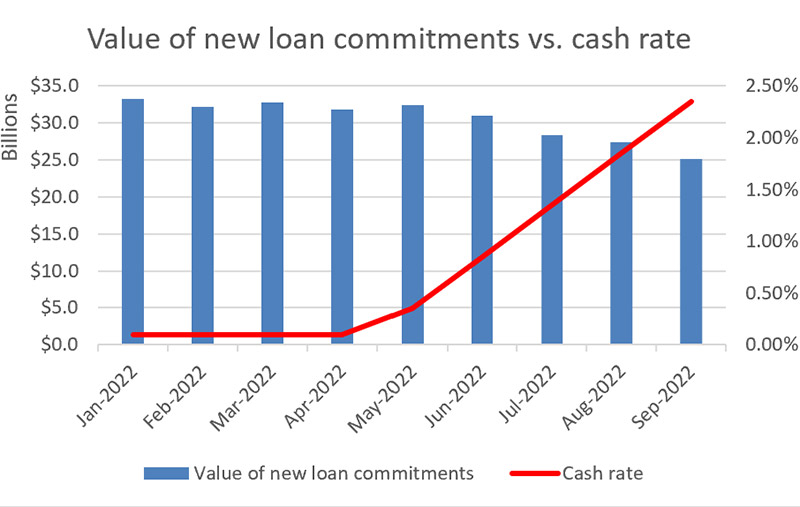

Source: RateCity.com.au. ABS Lending Indicators September 2022, released 2 Nov 2022, seasonally adjusted data. Annual change is Sept 2021 to Sept 2022. Excludes refinancing.

Canstar money expert Effie Zahos said households would not have had their finances stress-tested for repayments at these testing new levels.

“The serviceability buffer that banks would have assessed you on has now been fully absorbed by the rate hikes,” she said.

“Each repayment now has not been factored into households’ serviceability.”

Katherine Keenan, ABS Finance and Wealth Spokesperson, said the value of new loan commitments for housing fell 8.2 per cent to $25.1 billion in September 2022, after a fall of 3.4 per cent in August.

“Although housing lending has fallen for four consecutive months, the value of loan commitments in September remained well above pre-pandemic levels,” Ms Keenan added.

“Owner-occupier loans in September were 23 per cent higher than in February 2020, while investor loans were 60 per cent higher.”

Senior economist Maree Kilroy from BIS Oxford Economics told the ABC that the fall in first home buyer loans was “the steepest monthly decline on record”.

“We ultimately expect a nationwide all-dwelling median price peak-to-trough fall of 11.5 per cent,” she said.

Real Estate Institute of Australia President, Hayden Groves, said the patterns in lending are consistent with what agents are experiencing on the ground.

“Listings are being hard fought, with investors and homeowners taking their time in making purchasing decisions.

“This is not dissimilar to pre-pandemic market conditions with activity still above what it was, however, the question remains, will lending trends hit a plateau or continue to decline to even pre-pandemic levels?

“With the RBA signalling more rates rises to come, if inflation is not kept in check we may very well see further declines in lending.”

Building momentum stalls

Builders, meanwhile, are also confronting a bleak medium-term outlook.

While the nation’s construction industry is working its way through a backlog of work now, the total number of dwellings approved fell 5.8 per cent in September, in seasonally adjusted terms, following a 23.1 per cent increase in August, according to additional data released Wednesday by the ABS.

Daniel Rossi, Director of Construction Statistics at the ABS, said the fall in approvals was driven by private sector houses, which declined 7.8 per cent. Approvals for private sector dwellings excluding houses fell 1.8 per cent.

Across Australia, total dwelling approvals fell in South Australia (-19.7 per cent), Tasmania (-10.8 per cent), Western Australia (-9.3 per cent), New South Wales (-8.8 per cent), and Queensland (-6.2 per cent). Victoria was the only state to record an increase, rising 3.4 per cent.

Approvals for private sector houses fell in all states: Western Australia (-11.4 per cent), Queensland (-8.6 per cent), New South Wales (-7.9 per cent), Victoria (-4.7 per cent), and South Australia (-4.3 per cent).

“Less activity in both existing housing inventory and building approvals and completions is not a good sign for housing supply,” Mr Groves said.

Rates biting hard

The total increase to mortgage repayments on a $500,000 loan is now $760, according to RateCity. A homeowner with a $750,000 loan has seen monthly repayments increase by $1,140 since rates began to rise.

RateCity.com.au research director, Sally Tindall, said although prices are dropping it’s still an uphill battle for first-home buyers trying to enter the market.”

“The properties they’re inspecting might be getting cheaper, however, the entry price for many first-home buyers is still out of reach, particularly now the cost of borrowing money is significantly higher,” she said.

Some existing borrowers are being forced to accept lowball offers in order to quickly offload their property in a falling market.

AMP Capital chief economist Shane Oliver said the number of distressed or forced sales could spike significantly by early 2023.

“There is an increasing risk that we’re going to see more forced selling through next year as people’s buffers would have been used up by then,” he was quoted as saying by the Financial Review.

“Right now it’s early days and most people still have jobs, so owners who may be suffering mortgage stress will probably be handling that at the moment by cutting back on spending in other areas where they can, but as we go into next year, the interest rate serviceability of 2.5 per cent that was applied up until October of this year would have been used up, so people who are assessed to have free cash flow and be able to keep making the payments, I think would be increasingly on the edge.”

Wage growth and continued low unemployment, on the other hand, could stave off any significant rise in mortgage defaults.

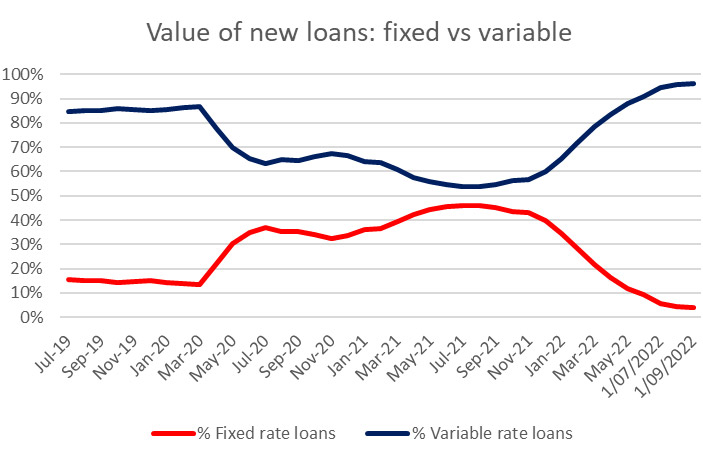

Fixed out of favour

New borrowers are completely shunning fixed rate home loans.

At its peak in July 2021, when borrowers could still lock in rates under 2 per cent, 46 per cent of all new and refinanced loans were fixed.

Now, in dollar terms, a meagre 4 per cent of new and refinanced loans are at fixed rates.

Source: RateCity.com.au. ABS Lending Indicators September 2022, released 2 Nov 2022

“It’s no surprise to see borrowers continue to snub fixed loans,” Ms Tindall said.

“These rates skyrocketed well before the RBA hikes began and show little sign of coming back down any time soon.

“Twelve months ago, the big four banks were offering two-year fixed rates as low as 1.99 per cent - fast forward to today, and the lowest two-year fixed from a big four bank is currently 5.49 per cent,” she said.

After hitting a record high in August, the value of refinancing dropped by $1.55 billion in September, however, compared to September 2021, refinancing is still up 7.4 per cent.

")