")

")

RBA's next interest rate movement should be downwards - or else

API Magazine columnist Michael Matusik has lambasted the Reserve Bank of Australia (RBA) for singling out borrowers as the scapegoat for high inflation and risking a recession.

Well, if you ask me the Board of the Reserve Bank Australia really does need a broom through the joint.

As we all know there was another 0.25 per cent lift in the Australian cash rate in May – making it 11 hikes in just 12 months – on some pretence that doing so will somehow reduce inflation.

Inflation isn’t being instigated by the consumer but largely by a range of ill-conceived government policies and actions.

And the May federal budget just added further fuel to the fire.

If widespread consumer largesse was the main culprit, then why not lift the rate of GST rather than just punish mortgage holders?

Furthermore, it is the lucky one-third of households – mostly older Australians – that own their homes outright who are unaffected by the RBA’s aggressive interest rate hikes.

Meanwhile, it is the older generations who are driving Australia’s household consumption and have forced the RBA to continue to lift interest rates, which is negatively impacting renters and mortgage holders.

Additionally, when you survey Australia’s employment situation correctly – using Roy Morgan’s work and not the dubious ABS survey – the number of unemployed people across Australia has lifted by 326,000 or 27 per cent since the first interest rate hike this time last year.

The number of under-employed folks is up 178,000 or 15 per cent since May last year.

Overall, some 500,000 Aussies are worse off jobwise since the RBA decided to start lifting the cash rate. Remember the assurance there would be no rate rises until 2024?

Before May’s surprise decision - and as shown in my table - some 10% of Australians were unemployed and another 9% work but would like more hours.

Unemployed and under-employed estimates

| Quarters | Unemployed | Underemployed | Total |

|---|---|---|---|

| Estimated numbers | |||

| Mar 2002 | 1,187,000 | 1,193,000 | 2,380,000 |

| June 2022 | 1,325,000 | 1,232,000 | 2,557,000 |

| Sept 2022 | 1,270,000 | 1,387,000 | 2,657,000 |

| Dec 2022 | 1,361,000 | 1,431,000 | 2,792,000 |

| Mar 2023 | 1,513,000 | 1,371,000 | 2,884,000 |

| Change since 1st interest rate increase | |||

| Number | 326,000 | 178,000 | 504,000 |

| % increase | 27% | 15% | 21% |

| % labour force | |||

| Mar 2002 | 8.2% | 8.2% | 16.4% |

| June 2022 | 8.5% | 8.5% | 17.0% |

| Sept 2022 | 8.6% | 9.3% | 17.9% |

| Dec 2022 | 9.2% | 9.6% | 18.8% |

| Mar 2023 | 10.1% | 9.1% | 19.2% |

Source: Matusik + Roy Morgan

More, now, will join the jobless queue and work less hours in the months ahead.

Yet this tale of woe has a positive note.

Looking ahead, the financial markets are betting that official interest rates will fall.

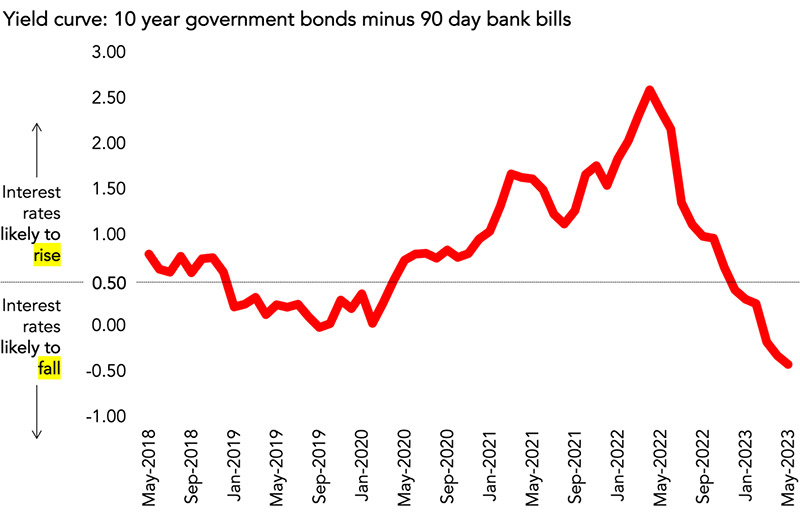

My next chart shows the yield curve – the difference between the price of long money versus short term returns – and it is a great bellwether when it comes to the future direction of official interest rates. It typically leads by between three and six months.

Source: Matusik + RBA.

So, by the end of calendar 2023 the financial markets are strongly suggesting the RBA cash rate should start to fall. And just like the overzealous hikes of late, the decline could also be steep.

It will probably need to be, or recession here we come.

For mine, I reckon the next interest rate movement will be down – well it should be – and that fall could be by 0.5 per cent and in November 2023.

By the middle of next year, I also think that the cash rate is likely to be around 2.5 per cent, where it will probably rest for some time.

Best get used to 5 to 6 per cent mortgage rates for some time to come.

")