")

")

Are interest rates the only game in town when it comes to property prices?

Much has been made of the link between interest rates and property prices, but will home values necessarily go up if interest rates peak and start to decline over the coming 12 months?

While the sharp rise in rates has certainly moved the property market backwards, many commentators are telling us that interest rates alone can predict where the market will be in a year or two.

Is that correct?

What is the property impact of interest rate rises?

Interest rate rises impact the market in three ways.

The first is to discourage banks from lending more money to property buyers.

Rising rates also crimp the amount people can borrow, cutting what they can spend at an auction or sale.

The third way is to price borrowers who would have been marginal, only just able to afford a loan at lower rates, out of the market.

These factors combine to reduce the number of home loans. You can already see this at work with an increasing number of borrowers deciding now is not the time.

Source: G Jericho.

But we need to place this fall in context. As you can see, while there has been a significant fall this year, the volume has only reverted back to the previous trend line.

Won’t higher rates force people to sell?

It is true that rising interest rate rises are likely to cause some distressed property sales.

This is most likely to be focused within the 850,000 Australians facing the “mortgage cliff” (coming off low fixed rates and on to higher 2023 variable rates) over the next year or so.

For borrowers on low incomes and with low equity in their home, their position could become more tenuous if their new level of repayments is above what they have been assessed as able to afford.

Most of these fixed rate borrowers are first time home owners but there are others, including business owners who refinanced during Covid and recently separated people who have concluded a family law settlement.

As we move towards the end of 2023, distressed buyers will get a lot of attention, but this will not be the entire story.

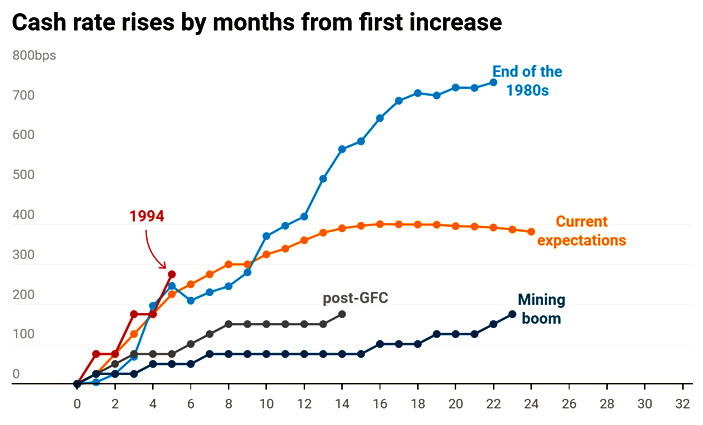

If we look at the most recent periods of sharply rising rates, house prices did fall back marginally but the vast majority of borrowers were able to absorb the increases.

Source: G Jericho.

For mortgage holders who have been in the market for years, cutting back spending and savings will allow most to weather the increase.

A good metric to keep track of these borrowers is the amount of money held in mortgage offset accounts. If this level drops precipitously, then the market has a difficult road in front of it.

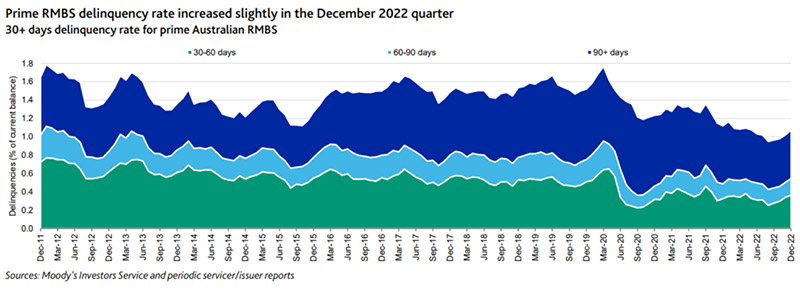

The other metric to keep an eye on is mortgage arrears reported by banks. To date, there have been small spikes in arrears, but this has come off a record low.

The other point to make here is that for a small yet significant percentage of investors who have been in the market for years, increased rates may prove a positive.

Many haven’t seen an after-tax benefit (negative gearing) for some time but the recent rise back to more “normal” rates will allow some of them to regain this tax break.

Interest rates not the whole story

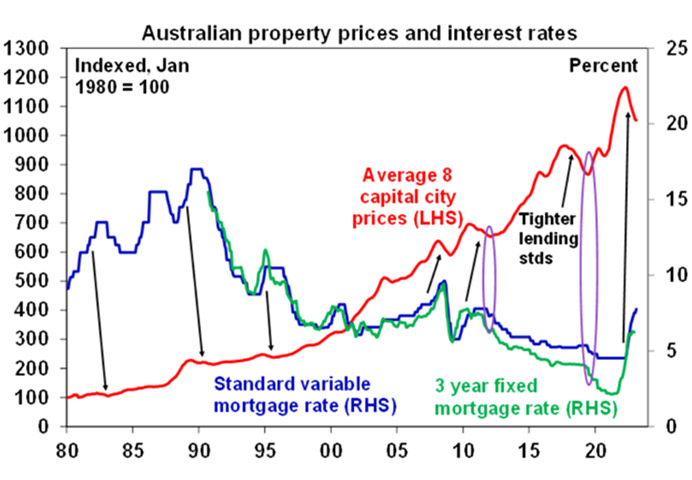

To put things in perspective, let’s take a look at the long term history of the property market compared to prevailing interest rates.

As we can see, when we strip everything else out, the market has defied high interest rates to keep growing (in the 1990s) with growth accelerating over the last 20 years.

Source: RBA/ABS.

While falling interest rates undoubtedly played a role, the higher growth over the last two decades is more related to tax changes for investors brought in by the Howard Government at the start of the millennium.

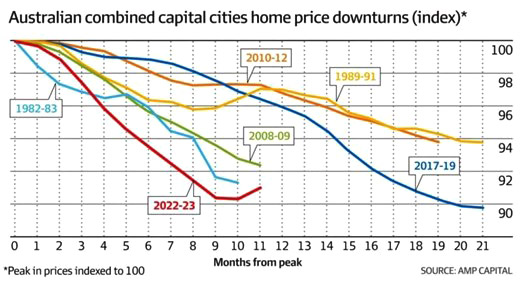

When will the current downturn end?

Many will tell you the recent rises in March show the market has already bottomed out.

It’s arguably too early to make this call.

While the recent lift in prices has been encouraging, most of this small upward turn in the property price indices came from the top end, particularly in Sydney.

This appears to be a case of more expensive properties hitting the market in autumn - traditionally one of the best times to sell pricey real estate - rather than a whole of market movement.

Still, there are other indicators pointing to a rebound in property prices.

The supply-demand dynamic is working in housing’s favour, with a decline in the supply of properties for sale and a significant increase in migration rates.

Over the next year or so, we are also likely to see new home completions fall back.

These changes to the supply-demand equation are feeding into historically tight rental markets. With rental returns rising, more investors are likely to be encouraged to buy in.

Of course, a sharp deterioration in GDP or employment could spoil the party but most economic indicators show a slowing economy, not a falling one.

So, will property take off?

It’s certainly possible but it may take some time.

The outlook for house prices the rest of this year remains bumpy.

It’s an even money bet as to whether rates have peaked or if there are still more rises to come. In any event, the likelihood is we will see falling rates in 2024.

But the impact of falling rates - like rising rates - can take time to filter through.

The mortgage cliff will likely dampen growth but most of this impact will be felt in the outer suburbs of major cities – much like what happened to the expensive parts of the market in 2022 when the official cash rate took off.

For investors eyeing property in capital cities, there are plenty of opportunities for buyers who stick to investment-grade quality and take a long-term perspective. Investors still need to understand that A grade properties are still in demand and in short supply, so may generate outlier price results.

Ditto for large regional centres like Caboolture, Ballarat, Bendigo, Albury-Wodonga and Geelong. We expect these cities will be well placed to ride the next upturn in the cycle.

")