")

")

RBA 'unneccesarily' tipping economy towards recession: Deloitte

Deloitte, one of the so-called Big Four global accounting firms, has branded this year's RBA interest rate hikes as unnecessary and said they risk driving Australia's economy into a recession.

The world’s largest professional services firm has launched a broadside at the Reserve Bank of Australia (RBA) over its past two interest rises and the likelihood it will impose more soon.

Deloitte slammed the decision to keep raising interest rates at a time when “Australia is facing the weakest rate of economic growth outside of the pandemic since the recession of the early 1990s”.

Releasing its March 2023 edition of the flagship Business Outlook report on Tuesday (17 April), Deloitte Access Economics Partner and report lead author, Stephen Smith, said mortgage holders and renters alike were increasingly squeezed by higher rents, and with little respite in sight.

“Our view remains unchanged – the additional 50 basis points of increases earlier this year were unnecessary, and have prompted a further downgrade in Australia’s growth outlook.

“That downgrade is centred on our households, and a consumer recession is now forecast in 2023, with household spending expected to finish the year below where it started.

“At a cash rate of 3.6 per cent, most Australians will be just fine.

“Many, however, will not. In just 10 months, the cost of servicing an average $600,000 mortgage will have risen by more than $14,000 per year once those rate hikes are fully passed through.

“But that’s just the average, and there are plenty of mortgage holders on either side of those numbers.”

At least 300,000 Australian households may currently be experiencing negative cash flow (and) that should shock all of us.

- Stephen Smith, Deloitte Access Economics

He added that renters were being hit from every angle.

“We are building far too few dwellings and, with a myriad of supply side challenges unresolved, that is unlikely to change in the near term.”

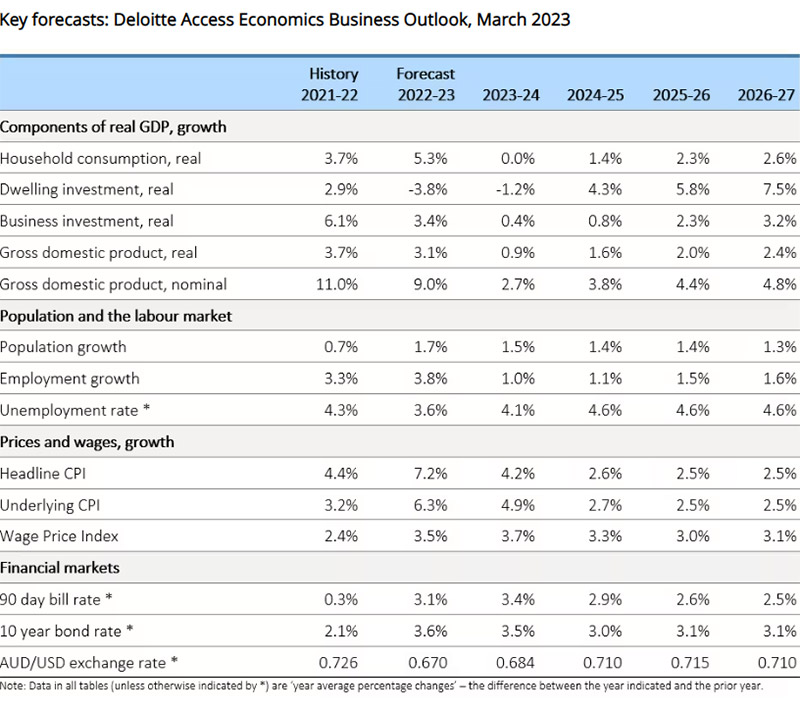

Deloitte Access Economics has revised down expectations for Australian economic growth in calendar year 2023 and 2024 to just 1.5 per cent and 1.2 per cent respectively.

If realised, Australia’s growth will be the slowest, outside the pandemic, since the recession of the early 1990s.

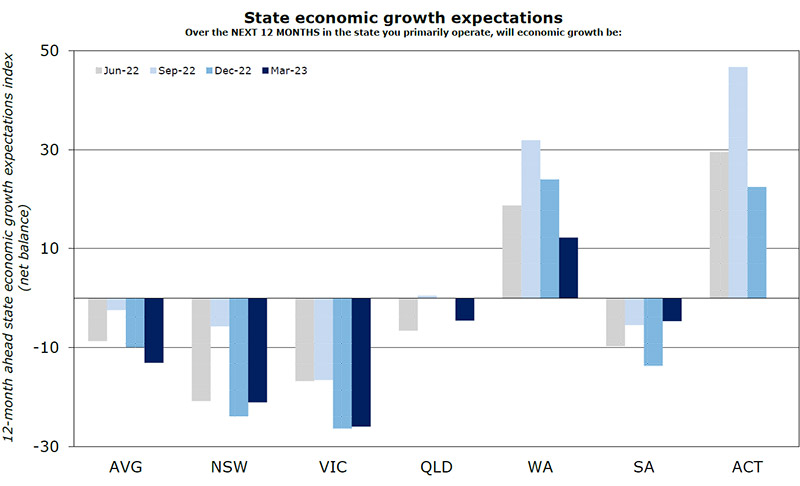

According to the ANZ/Property Council Survey 2023, only Western Australia and the ACT expect economic activity to grow rather than decline in their state. In a worrying sign for the economy, the two most populous states, new South Wales and Victoria, were the most pessimistic.

Source: ANZ/Property Council.

Consumers, carrying the weight of inflationary, mortgage, rent and cost of living pressures, are seemingly even less impressed with how the economy is tracking.

According to Tuesday’s (18 April) ANZ-Roy Morgan poll, consumer confidence is down another 2.1 points to 77.2 this week.

Interest rates are clearly a major influence, with the latest figures wiping out the increase of 1.1pts last week after the RBA decided not to raise interest rates in early April.

This is the now the seventh straight week the index has been below the mark of 80 – the longest stretch below 80 since the index began being conducted on a weekly basis in October 2008.

Drawing further comparisons to the 1990s’ economic hardships, the last time Consumer Confidence spent at least seven weeks under 80 was during the 1990-91 recession.

Looking forward, under a third of Australians, 30 per cent (down 2 pts), expect their family to be ‘better off’ financially this time next year while over a third, 36 per cent (up 3 pts), expect to be ‘worse off’.

The RBA makes its case

Amidst accusations it is pushing Australia into recession, the RBA Board on Tuesday (18 April) released its Minutes of the Monetary Policy Meeting relating to its 4 April rate pause.

While the RBA held off on an 11th consecutive rate hike this month, the policy meeting minutes make it clear there are a range of variables of concern in its quest to return inflation to its 2-3 per cent target range.

One was the upgrade to near-term projections for population growth, which members noted could put significant pressure on Australia’s existing capital stock, especially housing, which would in turn manifest in higher consumer prices.

“There are already signs that the recent fall in housing prices might be smaller and more short-lived than expected,” the minutes noted.

“Although higher immigration might reduce wage pressures in industries that had been experiencing significant labour shortages, members noted that the net effect of a sudden surge in population growth could be somewhat inflationary for a period.”

The second economic component of RBA concern was the increased “risk” of larger wage increases in parts of the economy, including in the public sector, later in the year.

It’s a risk that will be of little concern to wage earners whose incomes have been eroded so harshly over the past 18 months.

“Board members observed that the flowthrough to inflation from wages in social and public sector industries is somewhat diffuse … but judged that it was nonetheless likely to have some impact,” the Board noted.

“Overall, wages growth remained consistent with the inflation target, provided there was some pick-up in productivity growth.”

Deloitte’s Mr Smith remained unconvinced that the balance of arguments landed in favour of continued rate hikes.

The latest Financial Stability Review from the RBA suggests, he said, that under typical assumptions for income growth, inflation and unemployment, 15 per cent of variable-rate, owner-occupier mortgage holders will be in negative cash flow by the end of 2023, with many of these borrowers already projected to be in this position.

“On these numbers, at least 300,000 Australian households may currently be experiencing negative cash flow, with mortgage repayments and essential living expenses together exceeding household disposable income.

“That should shock all of us,” Mr Smith said.

Source: Deloitte.

")