")

")

Property monthly price falls biggest since 1983

The biggest property price drop in almost 40 years is the fourth successive monthly market decline and there’s no sign of an immediate turnaround.

Australia’s property price declines are accelerating and spreading, with August delivering the sharpest monthly retreat since 1983.

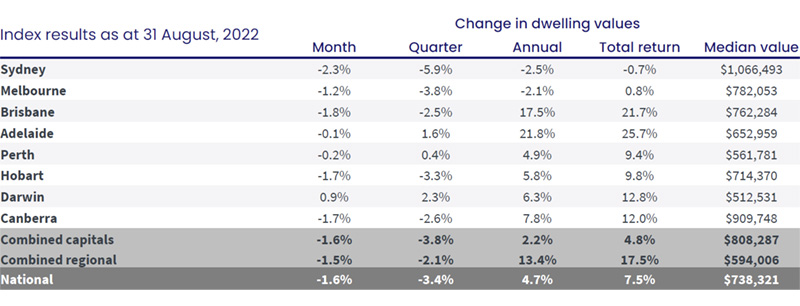

Down 1.6 per cent over the month, CoreLogic’s national Home Value Index (HVI) has clocked up its fourth consecutive month of price falls.

Unless you were a homeowner in Darwin or regional South Australia, there was nowhere to hide.

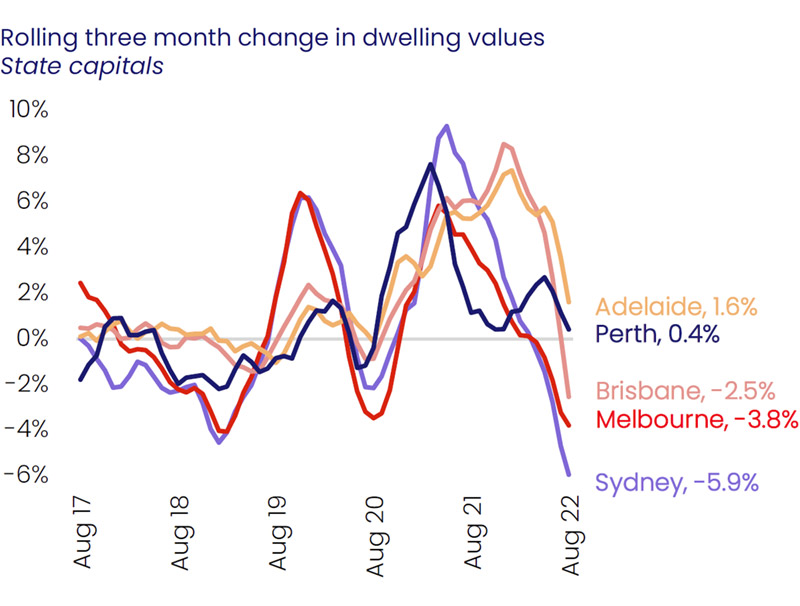

Sydney continued to the lead the downswing, with values falling 2.3 per cent over the month, however weaker conditions in Brisbane accelerated sharply through August, with values falling 1.8 per cent.

CoreLogic’s research director, Tim Lawless, said Brisbane’s shift into decline had been acute after almost two years of sustained growth due to record high internal migration and relative affordability.

“It was only two months ago that the Brisbane housing market peaked after recording a 42.7 per cent boom in values.

“Over the past two months, the market has reversed sharply with values down 1.8 per cent in August after a 0.8 per cent drop in July,” Mr Lawless said.

REIQ CEO Antonia Mercorella said the Real Estate Institute of Queensland’s recently released quarterly results showed Queensland’s soaring property market growth has started to show signs of calming after a period of unsustainable growth.

Across the 41 regional sub-regions analysed nationally, only seven areas recorded a rise in housing values in August, including the northern suburbs of Adelaide (0.9 per cent), Perth’s North East and Mandurah to the south (0.6 per cent/0.5 per cent) and the Coffs Harbour-Grafton region (0.6 per cent).

Regional retreat

Regional Australia’s spell as the price growth alternative driven by a flight to pandemic lifestyle relief has also come to a shuddering halt.

After recording significantly stronger appreciation through the upswing, the fall in regional dwelling values is catching up with the capital cities. Regional home values were down 1.5 per cent in August compared with a 1.6 per cent fall in values across the combined capitals.

Between March 2020 and January 2022 regional dwelling values surged more than 40 per cent, compared with a 25.5 per cent rise for the combined capitals.

“The largest falls in regional home values are emanating from the commutable lifestyle hubs where housing values had surged prior to the recent rate hikes,” Mr Lawless said.

“Over the past three months, values are down 8.0 per cent across the Richmond-Tweed, 4.8 per cent across the Southern Highlands-Shoalhaven market and 4.5 per cent across Queensland’s Sunshine Coast.”

No relief in sight

The prospects of the national property market dodging a fifth successive drop appear slim.

Financial markets are expecting the Reserve Bank of Australia (RBA) to increase official interest rates again next week by 0.5 percentage points.

A fifth straight month of rate rises, most of them double sized, would only serve as more negative sentiment for the real estate market.

As the spring selling season begins, more properties are expected to come onto the market at a time of relatively weak demand, which is likely to ensure prices keep falling.

Selling conditions across Australia’s unit markets have continued to weaken after a period of outperforming house markets.

Builders are feeling as much pain as property owners, with the total number of dwelling approvals falling a whopping 17 per cent in July.

Prices well above pre-Covid

Despite the recent weakness, housing values across most regions remain well above pre-COVID levels.

Housing affordability has barely improved despite the property market downturn, new research revealed.

The time it takes to save for a home deposit across the combined capital cities fell by a negligible 11 days to 11.11 years in the three months to June 2022, the latest ANZ/CoreLogic Housing Affordability Report found.

It’s barely different in regional areas.

It takes 10.7 years to save for a deposit in the regions as of the June quarter, up from 10.4 years three months earlier.

Households now spend 44 per cent of their income on repaying a new home loan, the report estimates. Anything above 30 per cent is regarded as entering into the domain of experiencing mortgage stress.

That is the highest level since June 2011 and up from 40.4 per cent in the previous quarter.

Renters are in just as much pain, with the typical tenant paying 30.9 per cent of income on rent, up a 0.6 per cent on the previous quarter.

Home values in all capital cities and rest-of-state regions, bar Melbourne, still remain 15 per cent or more above the levels recorded in March 2020, implying most homeowners have a significant equity buffer before their home is likely to be worth less than what they paid.

“A 15 per cent peak to trough decline would roughly take CoreLogic’s combined capitals index back to March 2021 levels,” Mr Lawless said.

“Additionally, many homeowners would have had at least a 10 per cent deposit and paid down a portion of their principal, the risk of widespread negative equity remains low.”

As to whether this downturn was different to others or ending abruptly, Mr Lawless said he expects it will continue to play out through the remainder of the year and possibly into 2023.

“It’s hard to see housing prices stabilising until interest rates find a ceiling and consumer sentiment starts to improve,” he said.

“From current levels, interest rates are likely to increase by at least another 75 basis points and there is a good chance advertised stock levels will accumulate through the spring selling season, providing more choice for buyers and adding further downwards pressure on housing values.”

")