")

")

Is this property downturn different to others?

Australian property booms historically last more than three times longer than downswings and when prices fall they only lose a fraction of the gains made, but is it different this time?

New research has shown that periods of national property price booms last around three times longer than the downturns that only eat away at a fraction of the gains.

But the question of whether this pattern will endure during the current period of price falls is less clear.

Economists say the current downturn could be the steepest and longest since the 1990s.

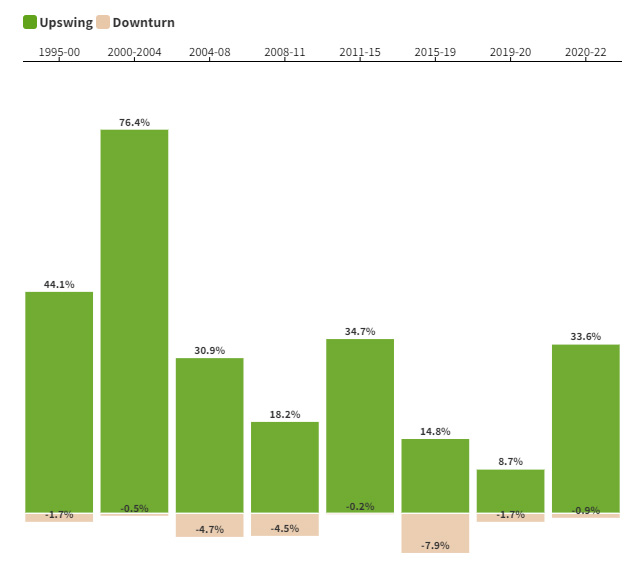

In previous property booms, house prices on average rose 32.7 per cent and the upswing on average lasted on average 33 months.

Meanwhile, in previous downswings, house prices on average declined three per cent and the period of falls on average lasted nine months.

Dr Nicola Powell, Domain Chief of Research and Economics said it was unlikely the current falls, while sustained, would see prices reach pre-pandemic levels.

“A difference between the current downturn and its predecessor, is that interest rates are rising, increasing the cost of a home loan and reducing borrowing capacity at a time when living costs are soaring,” she said.

“While this might mean a bigger decrease in prices than we have historically seen, this analysis suggests it is unlikely we will see a return to a pre-pandemic price.

“With the current combined capitals’ median house price at $1.065 million, it would need to drop a further 25 per cent to reach pre-pandemic pricing.

| Decline | Median house price | House price similar to |

| -5% | $1,012,175 | Sep-21 |

| -10% | $958,902 | Jun-21 |

| -15% | $905,630 | Mar-21 |

| -20% | $852,358 | Dec-20 |

| -25% | $799,085 | pre-pandemic |

There have only been four periods where house prices across the combined capitals declined annually since the early 1990s – during 1995-96, 2008-09, 2011-12 and 2018-19.

“All downturns over the past three decades had an annual decline that peaked at less than 10 per cent,” Dr Powell said.

“The decline was minor relative to the higher rate of incline that had preceded it.

“In comparison, all upswings had an annual increase that peaked above 10 per cent, apart from the pandemic-interrupted upswing of 2019-20.”

“Australians have this view that property prices go through these wild upswings and downturns when actually when you put it into perspective of historical performance … capital cities go through periods of strong growth and quite often prices surge but when we get to the downturn, it’s minor in comparison,” she said.

A historical comparison of upswing and downturn house price steepness, combined capitals

Dr Powell conceded the current downswing could still be steeper than the last one in 2017-19, when prices fell by 7.9 per cent.

“The depth of the downturn could be the biggest we’ve seen … and we’re likely to see a bigger decline in Sydney and Melbourne.

“It is realistic to expect a 10 to 15 per cent drop in house prices in Sydney but it is very unlikely for prices to return to pre-pandemic,” Dr Powell said.

Inflated prospects

Interest rate increases were unlikely to be ending in the short term and there was very little chance of a return to record breaking house price growth any time soon, according to Nerida Conisbee, Ray White Chief Economist, however, the chances of a sustained downturn and giant declines in prices looked to be steadily dissipating.

Ms Conisbee cited the example of the United States, where a mild easing of inflation to 8.5 per cent from above 9 per cent has been enough to drive investors back into the stock market, pushing it back up 15 per cent on mid-June lows.

And American tech real-estate marketplace company Zillow now predicts that US house prices will still climb 2.4 per cent over the next 12 months.

“Although Australia’s consumer price increases are not moving as quickly as the US, over the past seven weeks there has been a noticeable decrease in petrol prices and supply chains seem to be moving a bit quicker, Ms Conisbee said.

With inflation drivers improving and markets feeling more confident about the outlook, it does look like the housing downturn may be over sooner than expected.

- Nerida Conisbee, Ray White Chief Economist

“With inflation starting to pull back, so to does the need to raise interest rates.

“In Australia, the ASX 30-day interbank cash rate futures are currently implying an interest rate peak of around 3.6 per cent mid-next year, with rates then coming back from around October.

“Importantly, the expectation of how high the peak will be continues to pare back - a few months ago, it was expected to be well over four per cent.”

“With inflation drivers improving and markets feeling more confident about the outlook, it does look like the housing downturn may be over sooner than expected.

“Clearance rates are already starting to look more positive, hitting a 12-week high over the weekend,” Ms Conisbee said.

The Baltic Dry Index, which measures the cost of shipping worldwide, has dropped almost 80 per cent. Given how significant fuel and supply chains were to high inflation, there is the prospect that high inflation may be over sooner than later and with it the rate hike cycle.

Investors and renters

Further eroding confidence in the property market is inflation’s outstripping of rents over the past decade, leading to many investors evacuating the property market.

New industry research has shown that rents have grown at only half the rate of inflation over the past decade, in spite of the significant inflationary and rent increases during the past year.

Data from the Australian Bureau of Statistics Consumer Price Index from June 2012 to June 2022 showed rents increased by 11 per cent during the decade, however, inflation rose 25.6 per cent during the same period, a 15 per cent shortfall.

On an annual basis, rents saw a 1 per cent increase, while inflation increased at over 2 per cent each year over the decade.

Peter Koulizos, Program Director - Master of Property at University of Adelaide, said investors were becoming overburdened.

“As well as their cash flow taking a hit because of this income versus inflation imbalance, investors have also had to finance a huge variety of additional costs levied by all levels of government over the past decade.

“Governments deserted the supply of affordable rental properties years ago, expecting private investors to simply take over this responsibility, however more and more investors are deciding that it’s just not worth it.”

")