")

")

ANZ predicts epic national property price crash

A major lender has revealed property prices are set to plummet by almost 20 per cent, wiping more than $200,000 off the median value of a Sydney home and causing large falls around the country over the next two years.

No state capital escapes unscathed in ANZ’s newly released property price forecast for the next couple of years.

In a report whose title says it all, Australia’s Housing: Downhill until 2024, the bank predicts the national property market will suffer a massive 18 per cent fall from peak to trough before recovering slightly in 2024.

The epic correction is expected to be driven by the steep increase in mortgage rates that started in May and are likely to continue until the end of this year.

“The biggest factor driving prices lower is reduced borrowing capacity, not a rise in forced sales,” the report authored by Senior Economists Felicity Emmett and Adelaide Timbrell noted.

Amid the doom and gloom for homeowners, and ray of hope for first-home buyers, there was some respite from the shock of such big price drops.

“Arrears rates are coming from a very low base, households have built up large liquidity buffers, and the rise in the share of loans in negative equity is expected to be modest,” the report noted, suggesting mass sell-offs and loan defaults were likely to be minimal.

A tight rental market, rising immigration and low unemployment were tipped to mitigate the weakness in housing demand and even lead to a 2024-2025 return to price growth.

If ANZ’s predictions were to materialise, the national median house price could drop by $150,518 by the end of next year.

Sydney’s median house price is set to fall even further, with an estimated drop of $204,543 between July 2022 and the end of 2023, taking it to $1,141,650.

In Melbourne, the median house price could fall by $128,141 from July 2022 to the end of 2023 to $836,809, while prices could drop by more than $160,000 in Brisbane and Adelaide by the end of next year.

Median house prices - how far could they fall by the end of 2023?

| ANZ 2022 forecast | ANZ 2023 forecast | Dec 2023 forecasted median house price | Estimated drop July 22 – end 2023 | |

|---|---|---|---|---|

| Australia | -8% | -9% | $666,141 | -$150,518 |

| Sydney | -14% | -6% | $1,141,650 | -$204,543 |

| Melbourne | -11% | -6% | $836,809 | -$128,141 |

| Brisbane | 1% | -12% | $719,669 | -$164,667 |

| Adelaide | 4% | -17% | $539,452 | -$166,182 |

| Perth | 1% | -12% | $498,468 | -$88,556 |

| Hobart | -9% | -8% | $648,310 | -$134,438 |

| Darwin | 0 | -12% | $493,506 | -$96,242 |

| Canberra | -7% | -9% | $871,949 | -$175,963 |

Source: RateCity.com.au. ANZ property price forecasts, CoreLogic index-adjusted median values, 31 December 2021 and 31 July 2022.

ANZ’s forecast is in line with other major financial institutions, with Commonwealth Bank’s economists expecting a decline of at least 15 per cent peak to trough.

While steep price drops are expected between now and the end of 2023, ANZ is forecasting property price rises in all capital cities in 2024.

Median house prices – prices to rebound in 2024

| ANZ 2024 forecast | Dec 2024 forecasted median house price | |

|---|---|---|

| Australia | 5% | $699,448 |

| Sydney | 6% | $1,210,149 |

| Melbourne | 6% | $887,018 |

| Brisbane | 5% | $755,652 |

| Adelaide | 2% | $550,241 |

| Perth | 3% | $513,422 |

| Hobart | 4% | $674,243 |

| Darwin | 3% | $508,311 |

| Canberra | 4% | $906,827 |

Source: RateCity.com.au. ANZ property price forecasts, CoreLogic index-adjusted median values, 31 December 2021 and 31 July 2022.

As with the smaller capital cities, ANZ expects the increase in interest rates and reduction in borrowing capacity to eventually hit previously buoyant regional housing markets.

New data from CoreLogic suggest this is already occurring in some of the more expensive regional areas.

A low starting point for the share of loans in negative equity suggests that any rise in arrears may not be accompanied by forced sales.

The RBA estimates that even if housing prices fall 20 per cent, the share of loans with negative equity would rise to only 2.5 per cent, well below the 3.25 per cent peak in 2019.

Only 0.1 per cent of borrowers’ loan balances are currently in negative equity, whereby they owe more than the property is worth.

Instead, the main catalyst for the lower prices will be reduced borrowing capacity.

“Reduced borrowing capacity is set to be the key driver of lower prices,” the report forecast.

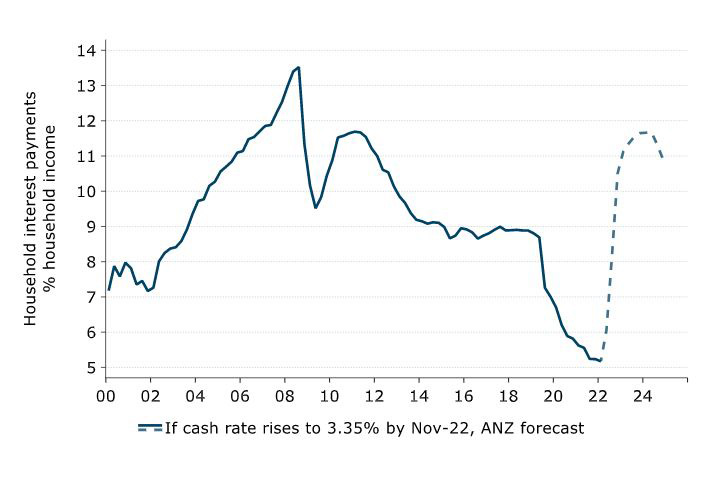

“Our forecast for the cash rate to reach 3.35 per cent equates to a reduction in borrowing capacity of nearly 30 per cent.

“This reduced ability to pay up will drive prices lower over coming months - already housing finance data show that average new mortgage sizes are beginning to fall.”

The bank’s outlook for construction was similarly dire.

“The very large backlog of work in the pipeline will support construction in 2022, but we expect a cumulative fall of around 16 per cent through 2023 and 2024, as higher mortgage rates and lower house prices flow through to weaker approvals and then falling construction work,” the report noted.

“Housing is an important driver of GDP in Australia, so the decline in activity will act as a significant drag on the economy.”

Options and pitfalls

With banks offering little interest on savings, inflation eating away at savings and salaries, and stocks still volatile and high-priced, many are questioning the merits of property as an attractive investment option.

Jim Malamatinas, Director of A Game Property Advisory based in Melbourne, said many first-home or less experienced buyers were tentative due to market uncertainty but others were more active.

“A lot of any potential buyers are watching and waiting to see what will happen in the property market given the uncertainty but investors are entering the market at the moment given the great opportunity to strategically find property in high growth areas at below market value,” Mr Malamatinas told API Magazine.

“Compared to this time last year I am currently serving double the amount of investors every month.”

Rents were identified by ANZ as one element that would lessen the impact of national price declines, with vacancy rates around the country below 1 per cent in many key markets (with rates around 3 per cent regarded as healthy).

“I am still purchasing investment properties with positive/neutral cashflow of 3.5-4.5 per cent yield and good capital growth indicators,” Mr Malamatinas said.

“Given the decrease in vacancy rates in the last month and future forecasts predicting a further decrease, investing in property will remain attractive.”

Inflation lurking

A direct impact of inflation is that it erodes the real value of housing.

For the June quarter of 2022, Australian home values fell 0.2 per cent, but when the soaring rate of inflation is factored in, actual value has fallen by 1.9 per cent.

Given that core inflation is unusually high, and the unique ‘emergency low’ cash rate settings through the pandemic, the RBA is now lifting the cash rate at the fastest pace since the 1990s.

CoreLogic’s Head of Residential Research, Eliza Owen, said that because of the strong relationship between home values and interest rates, inflation becomes a key indicator to watch when considering the outlook for the housing market.

So, how long will it take to curb inflation?

“Inflation is expected to remain high in 2022, with a mix of domestic and international factors putting upward pressure on prices,” Ms Owen said.

“Internationally, these include Russia’s invasion of Ukraine, the resurgence of Covid and lockdowns in China, and capacity constraints in some segments of the economy.

“Domestically, extreme weather events have contributed to increases in some food items, and resilience in household spending remains an uncertainty.”

However, there are early signs of relief in supply and demand pressures in the economy.

“Money markets are indicating a lower peak in the cash rate than originally anticipated a few months ago, and CBA has suggested RBA cash rate cuts could be in store as early as next year.

“If these trends in easing inflation begin to manifest more widely, it could signal a floor for the housing market decline as early as 2023,” Ms Owen said.

The major banks are split on cash rate forecasts, with Westpac and ANZ tipping a peak of 3.35 per cent and CBA 2.6 per cent.

")