")

")

Soaring inflation offers no reprieve to mortgage holders

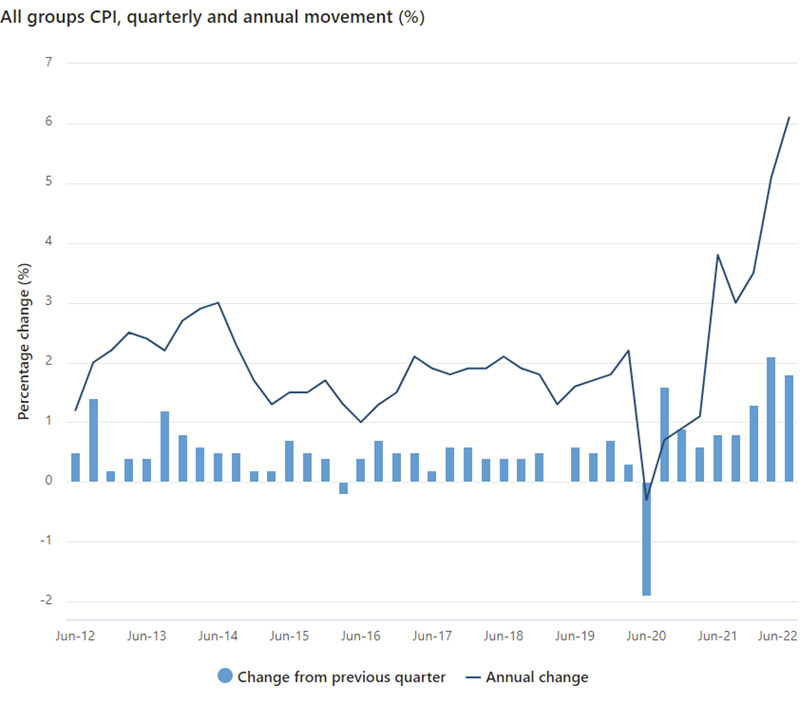

Inflation has hit 6.1 per cent according to consumer price index data released by the Australian Bureau of Statistics, offering further incentive for the Reserve Bank to lift interest rates next Tuesday.

Any doubts around the assumption that the Reserve Bank of Australia would ease the throttle on interest rates hikes have all but dissipated with the latest inflation figures released this morning (27 July).

The Consumer Price Index (CPI) rose 1.8 per cent this quarter, taking the annual figure over the 12 months to the June 2022 quarter to 6.1 per cent.

As the multitude of building company failures attests, the most significant price rises were due to higher dwelling construction costs, and the additional burden of higher automotive fuel prices.

It’s the highest inflation rate since December 1990, when Bob Hawke was prime minister.

The most significant price rises, according to Australian Bureau of Statistics (ABS) data, were new dwelling purchases by owner-occupiers (+5.6 per cent), automotive fuel (+4.2 per cent) and furniture (+7.0 per cent).

While annual CPI inflation increased to 6.1 per cent, annual trimmed mean inflation, which excludes large price rises and falls, increased to 4.9 per cent, the highest since the ABS first published the series in 2003.

The biggest contributor to the CPI rise this quarter was goods, as opposed to services, reflecting high freight costs, supply constraints and prolonged strong demand.

New dwelling prices recorded their largest annual rise since the series commenced in the June 1999 quarter. Price rises continue to be driven by high levels of building construction activity, combined with ongoing shortages of materials and labour.

Fewer payments of government construction grants compared to the previous quarter also contributed to the rise this quarter. These grants have the effect of reducing out of pocket expenses for new dwelling purchases.

Perth endured the most painful price rises, leading the nation with an inflation rate of 7.4 per cent over the year.

Unwanted records

Michelle Marquardt, Head of Prices Statistics at the ABS, said the quarterly increase of 1.8 per cent was the second-highest since the introduction of the GST, following on from a 2.1 per cent increase last quarter.

“Shortages of building supplies and labour, high freight costs and ongoing high levels of construction activity continued to contribute to price rises for newly built dwellings.

“The CPI’s automotive fuel series reached a record level for the fourth consecutive quarter, with fuel prices rising strongly over May and June, following a fall in April due to the fuel excise cut.”

Annual price inflation for new dwellings is currently the highest recorded “since the series commenced in 1999”, Ms Marquardt added.

Rents on the rise

Residential rents had been in decline on an annual basis in Sydney and Melbourne but the latest CPI data points to a turnaround that may help placate landlords seeking refuge from rising mortgage rates but offers no respite to renters already struggling to even find somewhere to live in the face of record low vacancy rates.

Melbourne and Sydney were up 0.2 and 0.4 per cent respectively, but both were down a similar amount over the year.

The other capitals continued to record strong price rises in the June 2022 quarter, with increases in rents seen for both houses and other dwellings, reflecting those historically low vacancy rates.

Perth and Darwin rents have taken off 9.1 and 11.4 per cent respectively over the year, well ahead of the next biggest increase (Hobart, 6.2 per cent). Over the past quarter, it was again Perth and Darwin leading the charge, with rent hikes of 2.1 and 1.9 per cent, followed by Hobart (1.8 per cent), Canberra (1.5 per cent), Adelaide (1.2 per cent) and Brisbane (1.1 per cent).

Housing as an overall expense was the second largest sector in terms of price rises, with a quarterly movement of 2.5 per cent, behind clothing and footwear at 3.5 per cent and equal to the furnishings and household items and services category.

RBA looking on eagerly

The RBA’s inflation target of 2-3 per cent is so far from current reality that it will inevitably raise interest again on Tuesday (2 August), with another double whammy 0.5 per cent hike looking unavoidable as it tries to suppress consumer spending and demand, and therefore inflation.

If the RBA increases the cash rate by 0.50 percentage points, the average owner-occupier with $500,000 debt and 25 years remaining will see their monthly repayments rise by $140.

If the RBA hikes by 0.50 percentage points next Tuesday, and it’s passed on in full by lenders, the average variable customer will see their rate rise by a total of 1.75 percentage points in four months.

If this happens, someone with $500,000, 25-year loan before the hikes began, would see their monthly repayments rise by a total of $472.

The rate hikes are not likely to end next month with inflation expected to continue to climb until the end of the year.

ANZ is now forecasting the cash rate could hit 3.35 per cent by November, while Westpac is forecasting the cash rate will hit this mark in February 2023.

RateCity.com.au research director, Sally Tindall, said more pain is on the way for the one-in-three households with a home loan.

“Australia isn’t the only country with an inflation problem; central banks around the world are moving quickly to try to contain the inflation beast, with hefty hikes to official rates.

“The US Federal Reserve, which is currently grappling with an even bigger inflation problem, is widely tipped to hike official rates by another 0.75 percentage points this week, taking the range to 2.25 per cent – 2.50 per cent.

“Every other week families are finding their grocery bills are growing, the car is more expensive to fill up and the cost of their takeaway coffee keeps hitting record highs.

“In the face of rising costs on all fronts, many families will need to start making significant cutbacks.

“People should really start putting pen to paper to come up with a financial strategy to get them through the next 12 months.

For some households it’ll be a few nips and tucks to their budgets, but for others it’ll involve making tough decisions,” she said.

")