")

")

Growth over for apartments as national real estate demand falls away

Selling conditions across Australia’s property markets have continued to weaken, with Perth and Adelaide proving an exception, while units are no longer delivering price growth in most areas.

As property prices continue to decline in most Australian real estate markets, units are still outperforming houses but their period of growth has ground to a halt.

Buyer demand across the board has been shown to have peaked in 2021 in almost every national housing and unit market. The notable exceptions were units and houses in Perth, which peaked in February-March 2022 and units in Adelaide, which peaked later in 2022.

With national dwelling values falling for the third consecutive month, selling conditions across Australia’s unit markets have continued to weaken.

Falling a further 0.9 per cent over the month, and down 1.4 per cent over the three months to July, national unit values are now 0.2 per cent lower over the year to date.

While national houses have recorded deeper monthly (-1.4 per cent) and quarterly (-2.2 per cent) declines, stronger growth over the first four months of the year means house values are still 1.2 per cent higher than they were at the beginning of this year.

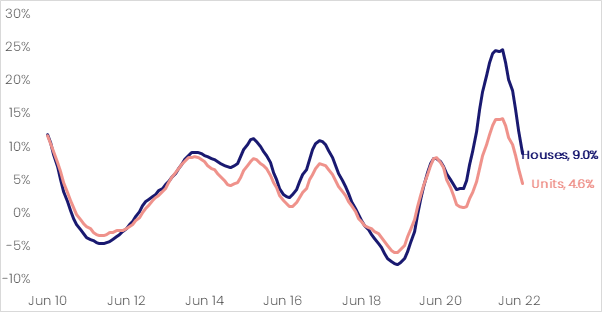

In May, the annual performance gap between national houses and units had fallen to its lowest level since April 2021 at just 7.0 percentage points.

The annual performance gap between national houses (9.0 per cent) and units (4.6 per cent) has continued to narrow, to just 4.4 percentage points. Annual house growth has fallen below double digits for the first time since April 2021 (9.3 per cent).

CoreLogic Economist Kaytlin Ezzy said the impacts of consecutive rate hikes are now becoming more widespread, with the pace of growth easing or falling into negative territory across most market segments.

“Units are relatively more affordable and attract strong investor activity, meaning value changes across the medium to high density sector are proving to be less volatile than the house segment,” Ms Ezzy said.

“However, market factors including increased interest rates, lower consumer sentiment and higher cost of living, mean selling conditions for units have also shifted in favour of buyers.”

Demand markedly lower

It may appear the Australian housing market changed gear overnight but market dynamics have been slowly cooling since 2021.

Initially, the intensity of buyer demand was evident back in March 2021 as the Domain Buyer Demand Indicator (BDI) built during the 2020 lockdowns but did eventually ease.

Lockdowns struck again in winter 2021 across certain locations, further constraining sales activity. Eased restrictions that collided with spring 2021 resulted in bumper activity, escalating Domain’s BDI to a record peak in October 2021 for houses and units across the combined capitals and houses in regional Australia.

Month when buyer demand peaked

| Area | Houses | Units |

|---|---|---|

| Combined capitals | Oct-21 | Oct-21 |

| Regional Australia | Oct-21 | Jan-21 |

| Sydney | Mar-21 | Mar-21 |

| Melbourne | Oct-21 | Mar-21 |

| Brisbane | Oct-21 | Oct-21 |

| Adelaide | Oct-21 | Feb-22 |

| Canberra | Jul-21 | Jul-21 |

| Perth | Mar-22 | Feb-22 |

| Hobart | Feb-21 | Sep-21 |

| Darwin | Jun-21 | Jul-21 |

Source: Domain. Domain Buyer Demand Indicator is a rolling 30-day time series, beginning the week ending October 1, 2017, and used to index the time series. The average index over winter 2022 (ending at the most recent period August 20, 2022) is compared to the immediately preceding three winters (2021, 2020 and 2019).

Looking at buyer interest by property type in each city reveals some interesting skews, according to Domain’s latest data.

The BDI is higher for units in Brisbane, Canberra, Darwin, Hobart and Perth. While this is the opposite in Sydney, Melbourne and Adelaide, the gap between houses and units is narrowing as affordability has become a key restraint for buyers, shifting the demand dial.

This steer towards units is also playing out in pricing as they outperformed house prices for the first time in almost three years across the combined capitals.

The stronger performance follows a period of substantial outperformance of house prices, which rose 34 per cent from trough to peak during the pandemic, while unit prices rose only 10 per cent.

Higher interest rates and living costs, as well as affordability, could play a larger role in the decreasing demand for houses. The relative underperformance of units during the pandemic boom and value proposition could place a floor under demand.

Since the October 2021 peak in the Domain BDI, it has moderated as wages struggle to keep pace with rising inflation and tightening affordability.

Across the combined capitals, current demand is 32.6 per cent lower for houses and 27.7 per cent lower for units compared to the peak. This aligns to the reduction in home loans financed and housing activity.

With the exceptions of South Australia and the Northern Territory, each unit market saw the average selling time increase, as vendors take longer to negotiate a sale. Compared to the three months to April, units across Hobart and regional Tasmania are now taking approximately three times as long to sell, while nationally, the median time on market has increased by six days.

Sydney units falling hardest

Following the national trend, unit values across the combined capitals decreased for the third consecutive month, down 1.0 per cent, taking capital city unit values 1.8 per cent lower over the three months to July.

Coupled with the weaker monthly increases recorded over the first quarter of the year, these declines have seen the annual change in values weaken from 12.7 per cent over the year to January, to just 2.5 per cent over the 12 months to July. Over the same period, annual growth in regional unit values has decreased from 23.7 per cent to 16.1 per cent.

“Across the individual capital city and rest of state unit markets, Hobart and regional Tasmania recorded the largest decline in values over July, down 2.5 per cent and 2.1 per cent respectively,” Ms Ezzy said.

Unit values across Sydney (-1.5 per cent) fell for the sixth consecutive month, taking values approximately $35,000 lower over the year to date, while unit values across Melbourne fell 1.2 per cent in July and were 2.1 per cent down over the quarter.

“With consecutive rate hikes and high total listing supply, unit values across Sydney and Melbourne are now just 0.3 per cent and 0.5 per cent above the levels recorded this time last year.

“Looking at CoreLogic’s daily index, it’s likely Sydney and Melbourne’s annual trend will fall into negative when the August results are reported,” Ms Ezzy said.

Regional NSW units declined by 0.4 per cent over the month, taking values back to the levels seen in April, while regional Queensland (-0.3 per cent) and Canberra (-0.2 per cent) recorded the first monthly fall in unit values since August 2020 and April 2020 respectively.

Tim McKibbin, Chief Executive Officer, REINSW, daily reports of excessive price discounting and threats of a prolonged downturn gave observers of the Sydney market the impression the market is in turmoil but claimed the reality is much less dramatic.

“Actually, transactions have been quietly increasing in recent weeks and we expect this gentle upswing to continue as the spring selling season gets underway this week.

“Clearance rates are steady and unremarkable, which belies the fact that many properties offered for auction don’t necessarily sell under the hammer on the day.

“It’s about strategy, it can differ by suburban market, and agents with local expertise know this better than anybody.

“In some cases, it’s a matter of semantics - vendors who set realistic price expectations in touch with the current market are not necessarily ‘discounting’.

“Obviously, prices on the whole are trending down, albeit slightly.

“Even prices in some regional prestige lifestyle areas, which enjoyed substantial uplifts during the first two years of the pandemic, have started to come back,” Mr McKibbin said.

")