")

")

Opinions divided on who fares worst in property market with few winners

There are few winners as dwelling and rental affordability worsens, and just as few agreements on the extent to which interest rates and inflation will impact different market segments nationally.

From senior Reserve Bank (RBA) officials to real estate and finance CEOs, opinions vary on what medium-term impact inflation and interest rates are going to have on the nation’s property prices and rental market.

From the luxury prime property market to first-home buyers, residential investors and commercial real estate, and the varied regional and capital city markets around the country, diverging outlooks are highlighting the uncertainty around the national property market.

Jonathan Kearns, the RBA’s Head of Domestic Markets, said he expected the luxury property market to sustain the biggest hit, while commercial property was also more highly susceptible to interest rate hikes.

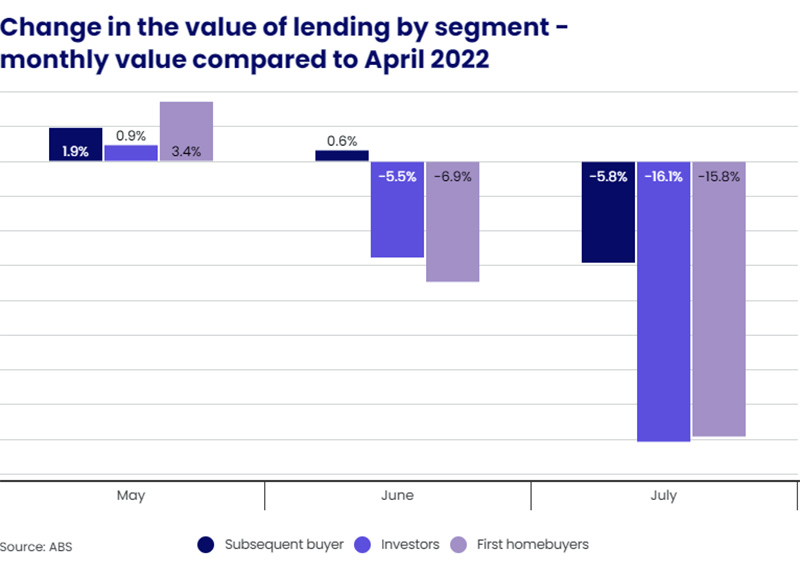

But Australian Bureau of Statistics data released this week has also shown that it was demand from first-home buyers and investors that was falling off over a cliff.

CoreLogic’s Head of Residential Research, Eliza Owen, said demand for housing finance across owner-occupiers that are not first homebuyers (i.e. upgraders, movers and downsizers, whom she refers to as subsequent buyers) appears to be fairly resilient in the rising rate environment.

“Since the rate tightening cycle started in May, investors and first-home buyers have seen much faster declines in housing finance secured than subsequent buyers,” she said.

“This may be because subsequent buyers are less sensitive to lifts in interest rates.

“Using the sale of an existing home to fund their next home purchase, subsequent home buyers would likely need to take out less debt than first-home buyers, thus being less affected by rate rises.

“Meanwhile, investors are likely to be more sensitive to a lift in rate rises.

“Although investors can offset the expense of higher interest rate payments as a tax deduction, they are typically more leveraged than owner occupiers, and have inherently higher mortgage rates,” Ms Owen said.

With Australia’s property market falling at the fastest pace since the 1980s, Mr Kearns said it was the pricier suburbs that tended to be more cyclical, and subject to bigger price variations.

“We know higher interest rates will tend to depress residential and commercial property prices but there is considerable uncertainty about the magnitude and even the timing.”

Inflation peak

RBA Governor Philip Lowe last week said it would be no surprise to see a 10 per cent national property price fall, while in April an RBA model estimated that a 2 per cent increase in interest rates would lower real housing prices by around 15 per cent over a two-year period.

“While this 15 per cent decline was commonly reported as being a forecast for housing prices, it was not actually a prediction of how much housing prices would change.

“Rather it was an estimate of how sensitive housing prices are to interest rates, assuming that all the other costs and benefits to housing don’t change with interest rates.

But he stressed that many factors other than interest rates also influence housing prices.

“For example, the demand for housing would be greater with stronger household income growth, increased population through immigration, or a preference for fewer people living in each household.”

Inflation is the driving force behind interest rates and commentators are unsure when it will peak and provide some respite to interest rate pressure.

Jo Masters, Chief Economist, Barrenjoey Markets, said it remains very unclear when inflation will peak and that makes valuing assets “incredibly difficult.”

“Household buffers remained one key discussion point, as data showed lending for new home loans slowed faster than estimated.

Australia’s record debt-to-income ratio of 187 per cent amplified the risks of rising interest rates, she told media.

Tony Lombardo, CEO, Lendlease, said there are positive tailwinds emerging as immigration that was shut off during the pandemic returns and boosts demand for real estate.

“The healthy balance sheets of households, a point highlighted by Reserve Bank in recent months, mean borrowers have the capacity to cope with even higher rates,” he said.

First timers not borrowing

The number of new loan commitments for first homebuyers was 8,338 – falling below the decade average of 8,787, and about 48 per cent below its peak in January 2021.

Zippy Financial’s Director and Principal Broker Louisa Sanghera said first-home buyer activity had now returned to a level lower than what was recorded pre-pandemic.

“Back then, first-home buyers had been increasing slowly after many years on the sidelines because of the high property prices at the time – or so they seemed in retrospect,” Ms Sanghera said.

“However, the government’s popular HomeBuilder scheme changed that scenario, with a significant proportion of the 113,000 applications likely to have been first-time buyers, keen to make the most of the financial grants that were available.”

Ms Sanghera said owner-occupier and investor activity was reducing more generally because of the higher interest rate environment, which was creating plenty of opportunities for prospective property owners in a time of rising interest rates.

“Now that might sound counter-intuitive, but would-be property owners are the ones facing the fewest lending troubles at present, because they are borrowing ‘clean-skins’ so to speak.

“Borrowers with existing portfolios are often experiencing lending challenges at present, but not so much for people who are applying for their first-ever home loan,” she said.

Real Estate Institute of Australia (REIA) President, Mr Hayden Groves, also cited dampening loan activity as a canary in the coalmine for the property market and rental supply and affordability.

Mr Groves said new loans have decreased 17.2 per cent to 93,956, with loans to first-home buyers dipping by a significant 32.6 per cent to 29,127. Loan values increased by 11.6 per cent over the year with the average loan size now $612,079.

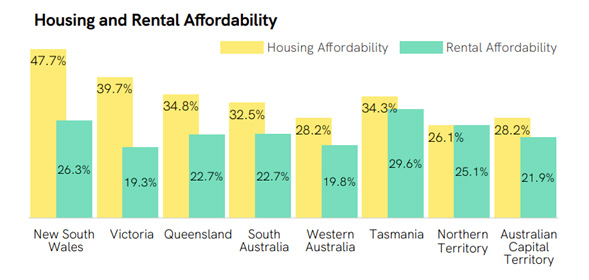

Rental affordability also declined in the June quarter of 2022, with the proportion of income required to meet median rent increasing to 22.9 per cent. This was an increase of 0.4 percentage points over the quarter and an increase of 1.2 percentage points over the past 12 months.

Source: REIA

“Over the quarter, rental affordability improved in Victoria but declined in all other states and territories, with the least affordable being Tasmania.

“The decline in housing affordability over the June quarter (down 2.7 percentage points) outpaced the decline in rental affordability (down 0.4 percentage points).

“Nationally, the proportion of income required to meet average loan repayments increased to 38.4 per cent, an increase of 4.7 percentage points over the past year.

“This is due to a combination of rising interest rates and higher average loans with average loan repayments increasing over the past year by $621 per month.

“Housing affordability has declined in all states and territories over the past year with New South Wales having the largest decline (down 5.7 percentage points),” he said.

Mr Groves said that with rental and home sale listings remaining at historical low levels, it is anticipated supply will continue to be constrained for the foreseeable future.

“While the outlook for housing affordability remains relatively gloomy, the next REIA Affordability Report, to be released in December, should paint a clearer picture of the long-term impacts of inflation control measures,” he concluded.

Ms Owen said subsequent buyers will continue to dominate the mortgage and purchasing market, even if higher interest rates impacted this relatively resilient demographic.

“For investors, we would expect demand to pick up longer term when there is more certainty around the trajectory of mortgage rates and price declines start to flatten out, because rental market conditions remain strong, with more rental demand expected as overseas migration returns.

Ms Owen said the lack of homebuyer grants compared to the past meant this price downswing would see fewer first first-home buyers capitalising on lower prices as they still had to contend with higher repayments as rates took off and inflation ate away at deposit savings.

")