")

")

'Deeply pessimistic' Australians shunning new homes, refinancing in record numbers

Australians have little confidence in their financial plight and are turning to refinancing to ease their budget burdens while shunning new homes in the face of rising interest rates and inflation.

New home sales continue to fall as buyers shy away from rising interest rates, increased building costs and uncertainty in the building industry.

The RBA’s hefty interest rate hikes and inflation that eats into household budgets and savings is also driving record numbers of people to refinance their home loan.

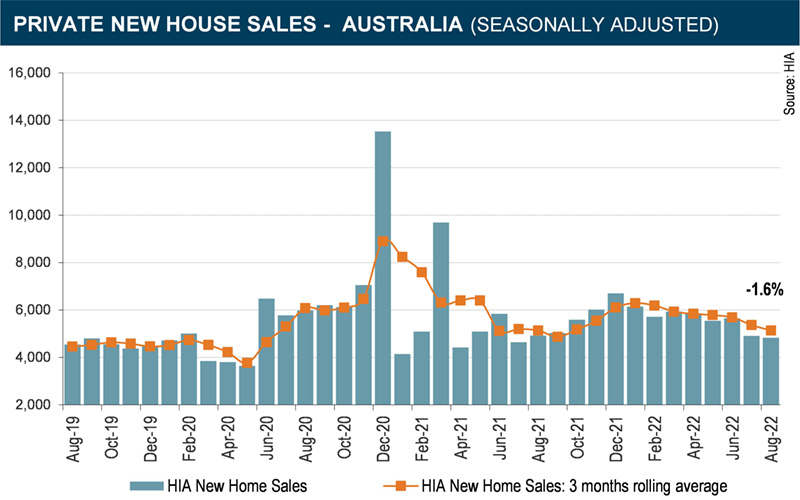

New home sales fell by 1.6 per cent in August after the 13.1 per cent decline seen in July, while more than a million Australians refinanced their home loan in the past 12 months

July and August represent the weakest pair of months for new home sales since the lockdowns in 2021.

Victoria drove the declines in sales in August, down by 15.2 per cent, followed by Queensland (-1.8 per cent). The other states saw increases, including South Australia (+18.2 per cent), New South Wales (+14.2 per cent) and Western Australia (+7.5 per cent).

For those three states that recorded increases, it was a significant turnaround from double-digit falls the previous month.

Lacking confidence

The fall in new home sales mirrors the “deeply pessimistic” mood of the country’s consumers and underpins the rush to refinance and low priority of buying a new home.

The latest Westpac Melbourne Institute Index of Consumer Sentiment report, released Tuesday (13 September), shows consumer confidence remains near historic lows, while record numbers of people are now working multiple jobs. The Australian Bureau of Statistics on Wednesday revealed 900,000 were making ends meet by going from job to job, a 4.3 per cent increase on the previous quarter.

HIA Economist Tom Devitt said sales of new homes over the past two months are reflective of a slowing in the market as the impact of the rise in the cash rate and inflation hit households.

“This rise in borrowing costs compounds the impact of the rise in the cost of construction.

“The full impact of recent and future rate increases will continue to flow through as an adverse impact on the sale of new homes in coming months.

“The concern remains that that the adverse impact of rising rates on the wider economy will be obscured by this volume of ongoing work and that the RBA goes too far, too soon,” Mr Devitt said.

Source: ABS

Westpac chief economist Bill Evans argued that consumers were glum but not at recession levels of misery.

He said home buyer confidence is only likely to see sustained gains once consumers sense that inflation is easing and the cycle of interest rate increases is over. He pointed out that the “time to buy a dwelling” index fell by 2.3 per cent in August, which brings it 41 per cent lower than its peak in November 2020.

“Although this index is likely to have bottomed out, signs of a sustained improvement are unlikely while overall confidence in the housing market continues to deteriorate,” Mr Evans said.

“History suggests confidence may be reaching something of a natural floor — a deeply pessimistic level but stopping short of the despair that can take hold when a deep recession causes widespread upheaval in labour markets,” he said.

Turning to refinancing

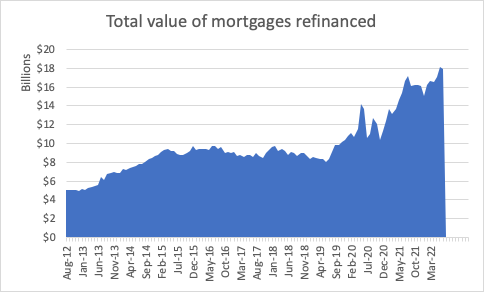

The latest ABS lending indicator figures show $17.93 billion worth of loans were refinanced in July, just below the June record all-time high.

Of the nearly 8 million Australian mortgage holders, an estimated 2.48 million had refinanced their home loan in the past year or intended to in the next two years, according to research by property exchange network PEXA.

The research released Wednesday showed that home owners refinanced their home loan on average 5.6 years after purchasing the property.

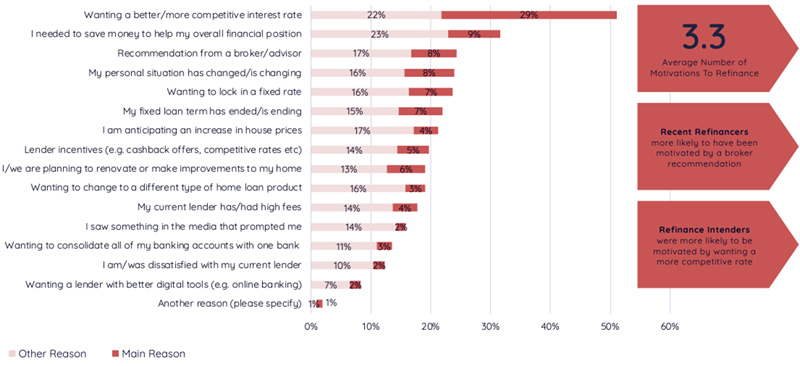

Highlighting the value of negotiating, more than half (55 per cent) of those who had refinanced in the past year stayed with the same lender but with an improved interest rate. Those who had refinanced in the past 12 months were also highly likely to refinance again, with 81 per cent stating they were intending to do so within the next two years.

Home owners who refinanced saved on average $1,524 per year. Refinancers who switched lenders achieved on average an annual saving of $1,908, and it took 4.2 weeks to finalise the refinance. Refinancers who remained with their existing lender achieved an annual average saving of $384, completing the refinance faster, in just three weeks.

Motivations to Refinance

Source: PEXA Refinancer Sentiment Report - September 2022

The banks are responding to this turbulent market by offering record numbers of home loan cashback deals, mostly targeted at refinancers.

Analysis from RateCity.com.au found that 34 lenders offer cashback deals, up from 12 in February 2020.

Deals range from $888 up to $5,000 for average mortgages. Citi also offers $6,000 via a broker for loans of $1 million or more, while Reduce Home Loans offers $10,000 cashback on loans of $2 million or more.

")