")

")

Is threatened property investor species returning from brink of extinction?

Faced with many predators, buyers of investment properties looked to be on the brink of extinction but studies emerging from the wilds of the real estate market suggest they may be bouncing back.

The herds of property investors that had once swept majestically across the suburban plains and contributed to the supply of now endangered rental properties have been under pressure from myriad predators.

But signs are emerging that buyers of investment properties may be tentatively stepping out from the safety of their caves and no longer afraid of tumbling over the mortgage cliff in lemming-like self-destruction.

The doyens of studying the movements of these threatened investor species, the Australian Bureau of Statistics (ABS), revealed Monday (3 July) that while still 21 per cent below last year’s numbers, investment property borrowers are returning to wild.

Value of new home loans approved in May 2023

| Value | Monthly change | Year-on-year change | |

|---|---|---|---|

| Total | $24.86 billion | $1.13 billion +4.8% |

-$6.3 billion -20.5% |

| Owner-occupier | $16.37 billion | $634 million +3.9% |

- $4.1 billion -20.2% |

| Investor | $8.5 billion | $497 million +6.2% |

-$2.2 billion -20.9% |

Source: ABS lending indicators for May 2023, released 3 July 2023, seasonally adjusted data.

In May 2023 in seasonally adjusted terms, the value of new loan commitments for total housing rose 4.8 per cent to $24.9 billion, after a fall of 1.0 per cent in April. It was still 20.5 per cent lower compared to a year ago.

The major driver of the turnaround was investor housing loans, which rose 6.2 per cent to $8.5 billion, while owner-occupier housing rose 4.0 per cent to $16.4 billion (still 20.2 per cent down on a year ago).

New South Wales (+8.5 per cent) and Victoria (+9.0 per cent) did most to drive this solid result.

In another sign of a healthier supply environment, the volatile ABS stats for the total number of dwellings approved rose 20.6 per cent in May following a 6.8 per cent decrease in April.

Daniel Rossi, ABS head of construction statistics, said the rise in total dwellings was driven by the dwellings excluding houses series, which rose 59.4 per cent.

“This increase reflected a large number of apartment developments approved in New South Wales in May,” he said.

Refinancing a means of survival

Stalked by the Reserve Bank of Australia’s interest rate rises, cost of living pressures, regulatory changes to rental regulations, and an imminent switch for many to higher variable rate loans, investors had been either devoured or were cowering on the fringes of the pack.

Real Estate Institute of Australia (REIA) President, Hayden Groves, said the latest ABS Lending figures for May 2023 demonstrate that interest rate rises are hurting owner occupiers, investors, and first home buyers, with many seeking to refinance.

Refinancing bounced back in the month of May, increasing by $1.58 billion to a total of $20.97 billion – the second highest monthly value for external refinancing on record.

The ABS lending indicators released today showed the total value of mortgages refinanced since the start of the rate hikes is now $247 billion, in seasonally adjusted terms.

Total value of refinancing – May 2023

| May-23 | Monthly change | Year-on-year change | Total since start of hikes (May 22 – May 23) |

|---|---|---|---|

| $20.97 billion | +$1.58 billion +8.1% |

+$3.8 billion +22.4% |

$247 billion |

Source: ABS Lending Indicators May 2023, released 3 July 2023, seasonally adjusted data.

According to Mr Groves, the latest ABS lending figures show that for owner occupiers and investors alike, external refinancing has grown considerably.

“Owner occupier refinancing reached a new high, 21 per cent higher than a year ago.

“Refinancing for investor housing rose 7.2 per cent and was 25.6 per cent higher than a year ago.

“Clearly, home buyers and investors are being heavily affected by interest rate hikes and inflation and are seeking new conditions,” he said.

“Twelve cash rate rises have been instrumental in the slowdown in first home buyer and investor activity, which is increasingly impacting housing affordability.”

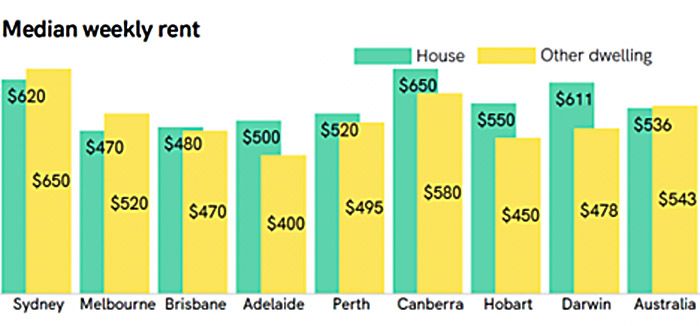

Steve Douglas, Executive Chairman, Australasian Taxation Services, said soaring rents and low vacancy rates meant the time was right for investors to return to the market.

“Vacancy rates dropped 0.8 per cent in Melbourne in one quarter alone, while cities like Adelaide (0.5 per cent), Perth (0.6 per cent) and Brisbane (around 1 per cent) offer investors guaranteed returns – those numbers are just nuts!

“The end result is that there has been a 17 per cent average annual increase on rentals for a two-bedroom apartment, 11 per cent on a two-bedroom house – that’s major money, this is an investor’s delight,” he said.

Shane Garrett, Master Builders Australia’s Chief Economist, said May’s sharp increase in unit/apartment building approvals is welcome given the severity of shortages in the rental market.

“The difficult conditions in the rental market are the result of prolonged underbuilding in the medium/high-density part of the market, dating from before the pandemic.

“The 12 interest rate increases we have endured so far have made it much more expensive to build new homes.

“Higher mortgage rates have also forced up the cost of providing homes to the rental market.

“Lending figures provide a good indication of what’s likely to develop on the ground over the coming months.

“The number of loans for the construction of a new home eased slightly during May and a 5.1 per cent uplift in the number of loans for the purchase of newly built dwelling, however, loans are still over 40 per cent lower than a year ago,” Mr Garrett said.

Government grants 'not the answer'

Recent reports have revealed government schemes like HomeBuilder are detrimental to housing affordability.

Dr Peyman Khezr, Senior Lecturer, Economics, Finance and Marketing at RMIT said such schemes have had unintended consequences that have worsened housing affordability in Australia.

“Subsidies of this nature typically do not cause long-term positive impacts on the market and often result in market disruptions.

“The solution lies in identifying and addressing the source of the problem, which is twofold: supply and demand.

“Grants, like HomeBuilder, shift the demand by enhancing affordability for potential homeowners, however, the supply cannot respond rapidly enough in the short term to cater to this surge in demand.

“Consequently, the price mechanism reacts to the excess demand by inflating the cost of home construction. This increase eventually diminishes affordability to a level where supply can meet demand.

“Put simply, grants rapidly stimulate demand while supply struggles to keep pace, ultimately leading to a rise in prices.

“Cash injections in the form of grants only inflate prices and deteriorate housing affordability in the long run.

“Instead of pumping cash into the housing market, the government should identify sources of market inefficiencies and regulate the market to address these issues,” Dr Khezr said.

")