Mortgage stress kept at bay by savings buffers - for some

Mortgage stress is creeping upwards as repayments soar but savings and offset loan buffers mean property panic selling is still some way off yet.

While each Reserve Bank of Australia (RBA) board meeting keeps the country’s six million mortgagees on the edge of their seats dreading new interest rate rises, experts suggest monthly repayment increases haven’t caused as much pain as predicted.

Undeniably, some suburbs are faring better than others.

Adam Boyton, Head of Australian Economics, ANZ, describes household incomes as resilient in the face of the interest rate hiking cycle.

“The level of household income at the end of the first quarter of this year was only a little below a pre-Covid trend and that’s even after taking inflation and interest rate increases into account, then add to this picture the savings buffers accumulated during the Covid years that remain untouched and that’s still the case, even allowing for the decline in the household saving rate recently.”

It’s view long espoused by under fire RBA Governor Philip Lowe in his claims that households can handle the rate rises.

“We’re not suggesting there aren’t households under serious financial strain in Australia because of inflation and rate rises but what the research shows is if we step back and ask ourselves where the economy might go over the next 18 months, it is not as negative a picture as some might suggest,” Mr Boyton said.

The 6 June Reserve Bank Board Monetary Policy Meeting Minutes note acknowledged the cash rate additional mortgage payments equating to around 9 per cent of household disposable income in April, but based on increases in the cash rate to date, payments were projected to rise to the equivalent of around 10 per cent of household disposable income by the end of 2024.

“Net flows into borrowers’ offset and redraw accounts remained positive to April, although extra mortgage payments were well below the highs seen during the pandemic and increases in scheduled mortgage payments would reduce some borrowers’ ability to make these extra payments, but higher rates were also creating an incentive to hold savings in these accounts,” the Minutes stated.

Panic selling averted for now

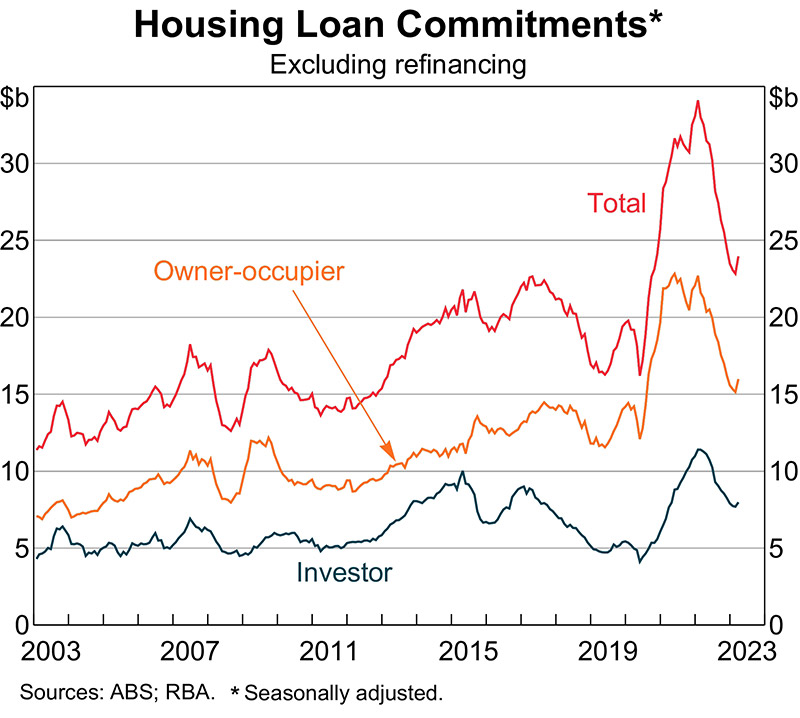

The value of non-performing housing loans was noted as rising a little but from a very low level and measures of personal insolvencies also remained at low levels, while new housing loan commitments had stabilised following declines of around 30 per cent from the peak in early 2022.

Commitments had steadied among both owner-occupiers and investors, and across states, which was consistent with housing prices having steadied after prior declines.

And panic selling is still not the norm.

Dawn Thomas, Senior Financial Advisor, The Wealth Designers

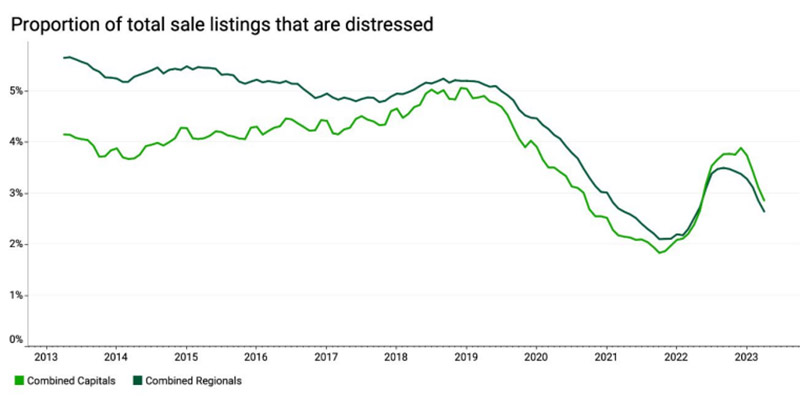

Online marketing platform Domain found the incidence of distressed sale listings that use phrases like ‘urgent sale’, ‘desperate seller’, ‘mortgagee in possession’ and ‘repossession’, has been falling for four consecutive months for the combined capitals, and seven consecutive months for the combined regionals, with levels still well below the historical proportions seen over 2013-2019.

Domain lists suburbs with the highest number of distressed listings in NSW as Marsden Park, Quakers Hill, Acacia Gardens, Austral and Schofields, in Queensland, Surfers Paradise, Pacific Pines, Biggera Waters and Southport, and Dandenong in Victoria.

Dawn Thomas, Senior Financial Adviser, The Wealth Designers, told API Magazine there are people who have paid down their loans rapidly by making use of the low interest rate environment when they were around, and her clients are encouraged to make allowance in their cash flow for further rates increases.

“We see clients who have their cashflow under control to an extent but where it has changed is how much cashflow they have available for other wealth building strategies, such as building up their investment portfolio or contributing into superannuation.

“People are becoming more acutely aware of the need of an emergency account because with a tighter cashflow, covering unexpected capital expenses becomes more difficult, so it is a fair assumption that many homeowners are struggling.”

Source: Domain.

Suburbs with the highest number of distressed listings

| Rank | Suburb | State |

|---|---|---|

| 1 | Marsden Park | NSW |

| 2 | Surfers Paradise | QLD |

| 3 | Quakers Hill | NSW |

| 4 | Pacific Pines | QLD |

| 5 | Acacia Gardens | NSW |

| 6 | Biggera Waters | QLD |

| 7 | Austral | NSW |

| 8 | Schofields | NSW |

| 9 | Southport | QLD |

| 10 | Dandenong | VIC |

Source: Domain

Benjamin Budge, Senior Advisor, My Wealth Solutions, suggests 50 per cent of homeowners are struggling with their property repayments or cashflow restrictions.

“The benefit of being able to plan ahead for interest rate changes is that many of our clients have cash tucked away or have prepared their offset account for these changes and it is harder to obtain credit now than it was prior to interest rate rises, primarily due to the drop in the borrowing capacity of a lot of investors who are no longer able to borrow the amount they would like to, in order to buy what they want to buy,” Mr Budget told API Magazine.

This in part may explain investor listings surging according to CoreLogic, which in Sydney, Melbourne and Perth are higher than the previous decade average.

“The City and Inner South market in Sydney has an historic 10-year average of 38 per cent of new listings coming from market investors but in May it topped the list of regions with the highest proportion of investment listings, surging to 57 per cent,” Eliza Owen, Head of Residential Research Australia, CoreLogic said.

Benjamin Budge, Senior Advisor, My Wealth Solutions

“Historically, purchasing data shows the majority of buyers are owner-occupiers, and it’s entirely possible the increase in investment listings may lead to owner-occupiers purchasing homes that were previously investment properties.”

“People might feel that mortgage stress was avoidable, however, there are people who entered their loans in an environment where there were historical interest rate lows and the rate increases have now put an immense strain on their cash flow, so for people who did not account for these increases, the pain of interest rate rises is real,” Ms Thomas said.

“Not only is debt more expensive, but inflation has also made everything more expensive so there must be many people feeling that they can’t catch a break in terms of the outgoings they have to cover and that is legitimately a stressful experience.”

Mortgage stress is most commonly defined as a household spending more than 30 per cent of their pre-tax income on their home loan repayments, with the same rule of thumb applying to rental stress.

Homelessness on the rise

Homelessness is at the extreme end of an inability to afford repayments, which are increasingly more affordable than rents, and the UNSW City Futures Research Centre expects the current 640,000 Australians experiencing homelessness to rise.

Deborah Di Natale, CEO, Council to Homeless Persons (CHP), says the organisation is currently witnessing an alarming escalation in homelessness in Victoria, highlighting inequality across metropolitan and regional areas.

A CHP report released last week indicates homelessness in the Geelong and Surf Coast electorate of South Barwon rose 435 per cent over five years, with equally disturbing trends unfolding in Melton (134 per cent increase), Eureka (113 per cent), Pakenham (113 per cent), Cranbourne (111 per cent), Bendigo East (107 per cent), Oakleigh (101 per cent), Mildura (96 per cent), Box Hill (88 per cent) and Morwell (85 per cent).

Debroah Di Natale, CEO, Council to Homeless Persons

The National Shelter Rental Affordability Index shows a 14 per cent decline in rental affordability in the last year, and rents on a typical home are up 23 per cent in Sydney, 21 per cent in Melbourne, 16 per cent in Brisbane, 12 per cent in Adelaide and 19 per cent in Perth.

“I don’t think mortgage stress is an overstatement because there are people hurting out there and many people are struggling to pay their mortgage and it’s a serious issue, which means some individuals are digging into their cash or savings to keep up repayments, which may work for a time but not forever,” Mr Budge said.

The ANZ’s Mr Boyton points to the easing of inflation and likelihood of interest rates peaking this year as signs of improvement.

“The key thing to supporting household incomes in Australia this year is getting inflation down and it’s also important the business sector stays healthy and continues to employ, because with the unemployment rate at just 3.7 per cent, it is still close to a 50-year low and business conditions remain at above average levels,” he said.