")

")

Big spending Aussies dent hopes of interest rate reprieve

Just as the Reserve Bank Governor Philip Lowe suggested a pause in interest rate rises was on the cards, big spending Aussie households may have given him cause for a rethink.

The Reserve Bank of Australia (RBA) has made it clear more interest rates rises are in the pipeline but a rethink may have been precipitated by data showing household spending skyrocketing.

Household spending rose 17.8 per cent in January compared to the same time last year, according to figures released Tuesday (14 March) by the Australian Bureau of Statistics (ABS).

Robert Ewing, ABS Head of Business Indicators, said: “Household spending remained high to start the new year, with increases across eight of the nine spending categories compared to January 2022.

“These increases were led by spending on transport (up 41.5 per cent), hotels, cafes and restaurants (38.5 per cent) and clothing and footwear (20.9 per cent),” Mr Ewing said.

“Spending on services recorded a 28.2 per cent through-the-year increase in January 2023, which was stronger than the 8.6 per cent rise in goods spending,” Mr Ewing said.

“This can be credited to the post-Covid recovery in spending categories such as transport, hotels, cafes and restaurants and recreation and culture.

“Spending on these services was more affected by Covid restrictions, and 2022 has seen a recovery to a more normal share of total spending. From the low point in April 2020, spending on services has risen 145.5 per cent compared to 35.8 per cent for goods,” Mr Ewing said.

While the RBA continues to turn the screws on borrowers in a bid to dampen high inflation, Australian households were spending their cash on holidays and hospitality at the start of the year.

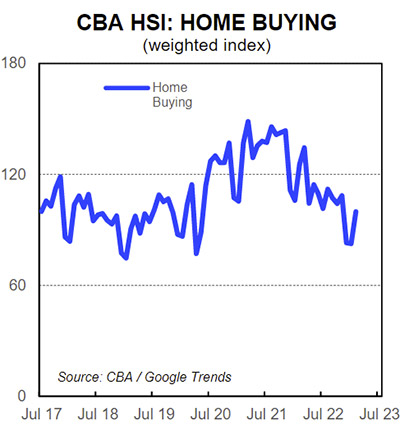

A glimmer of hope was offered by the Commonwealth Bank’s look at spending intentions, as opposed to spending already made, which pointed to a very small fall led by declines in entertainment, retail and travel.

The CommBank Household Spending Intentions (HSI) index for February showed The Entertainment index was down by 11.3 %/month, the retail index was down 9.8%/mth, and the travel index fell by 8.9%/mth.

The Home Buying Index rose by 21.0%/mth in February but remains 20.5 per cent lower over the past year.

The rebound in February as driven by a lift in home loan applications and Google searches for property inspections and appraisals and real estate listings

Commonwealth Bank of Australia Senior Economist Belinda Allen said the CommBank HSI Index showed a further brake on discretionary spending, but that Australians were willing to make sacrifices to prioritise holiday spending.

“We are seeing the growing impact of higher interest rates, with consumers taking stock and prioritising what they are spending their money on. Despite this, there is still demand for travel which indicates Australians are willing to sacrifice spending on other discretionary categories to enjoy a well-earned holiday following the pandemic.

“Recent RBA commentary suggests it is close to pausing the hiking cycle and interest rates are now restrictive. We expect a continued slowdown in consumer spending over coming months, with the large volume of fixed rate mortgages expiring this year adding pressure on household budgets from higher mortgage payments,” Ms Allen said.

Pressure again ramping up on RBA

The RBA last week said it was considering putting a pause on interest rate rises after its 10th consecutive increase earlier this month but ABS data pointing to high levels of spending may sway them to continue their current upwards trajectory.

The bank’s governor, Phillip Lowe, said it's aware of the growing pressures on households.

“The effects of the large cumulative increase in interest rates since May and the difficulties that higher interest rates are causing for many households,” Mr Lowe said on 8 March.

“We are closer to the point where it will be appropriate to pause interest rate increases to allow more time to assess the state of the economy.”

In the RBA’s monthly Monetary Policy Decision, Mr Lowe specifically identified household spending a key factor in its decision-making process.

“The Board will be paying close attention to developments in the global economy, trends in household spending and the outlook for inflation and the labour market.”

New data from the Australian Prudential Regulation Authority (APRA) that reports on the volume of housing loans that are non-performing (or 90 plus days past due), as well as loans where payments are late by 30-89 days, suggests Australian borrowers are generally coping well.

In the December quarter of 2022, the total portion of loans with late repayments sat near record lows of 1.01 per cent. This increased from 0.98 per cent in the previous quarter, led by a slight uptick in the volume of loans that were 30-89 days past due (from 0.3 per cent to 0.4 per cent).

While loans are not necessarily turning delinquent just yet, households are certainly showing signs of nervousness.

ANZ-Roy Morgan Consumer Confidence data, also released Tuesday, showed a drop of 2.9pts to 77.0 this week – the lowest rating since early April 2020 in the early days of the pandemic.

Consumer Confidence was down around the country this week and below 80 in all five mainland states after the RBA raised interest rates for a record tenth straight meeting, up 0.25 per cent to 3.6 per cent.

International factors in rates debate

David Whitting, Property Director at equity crowdfunding platform VentureCrowd, said the interest rate cycle was nearing an end.

“To be fair, the RBA has not hiked as far or fast as many of our contemporaries, including the US Federal Reserve and the RBNZ, and while some have criticised their slowness, consumers may very well be happy if other central banks and economies do more of the heavy lifting to bring down global inflation.”

Mr Whitting said another two 25bps increases would take the official rate 4.1 per cent, which most think will be the high point.

“It would seem sensible that those last two happen only if inflation numbers persist higher than forecast, and to measure that there may be a pause to allow those figures to flow through, so we may see a pause in April.

“External shocks may also mean a halt as has occurred in the US over the last few days, with the failure of Silicon Valley Bank changing most forecasts for another Fed raise into broad agreement that there will be no hike this month.

“Luckily, more stringent bank deposit ratios after the GFC in Australia mitigates that here, although other large company failures, such as the many builders going under, may provide a similar warning.”

Taking a different tack in inflation fight

Kevin Young, President of Property Club, said the huge jump in household spending will only encourage the RBA to increase interest rates even further but argued it was not the right approach to tackling inflation.

“The reality is that only 35 percent of private dwellings in Australia have a mortgage and the owners of these properties are now carrying the full financial burden of rising interest rates,” he said.

“The worst hit financially are first home buyers and property investors – the very people we need to solve the current housing crisis.”

Mr Young said the burden of fighting the scourge of high inflation should be shared more equitably through broader government fiscal measures to avoid pushing the country into recession.

“Australia should emulate the approach in the United States, which recently passed an Inflation Reduction Act designed to reduce inflation through a variety of fiscal measures.

“Australia does not need to replicate these precise measures but we can introduce policy settings that are most suited to our own circumstances.

“For example, Australia could increase the rate of GST by 1 per cent, which would be a fairer way of sharing the burden of reducing inflation.

“The billions of dollars collected by this additional tax could be used to reduce the budget deficit and as investment in the future of Australia.

“By slowing the economy through a broader tax, interest rates could be slashed to encourage property investors back into the housing market.

“In addition, we could restore negative gearing to second hand properties and immediately provide thousands of additional more affordable rental properties for renters throughout Australia.

“Rather than making the big banks richer through higher interest rates, these measures would help solve the housing crisis in Australia and deliver a positive social outcome for millions of Australians.”

Mr Whitting agreed that interest rates do disproportionately burden one sector of the economy, namely mortgage holders, and perhaps the time had come to advance the debate about a fairer distribution of the burden.

“At a time where yet another superannuation rule change is being argued over, perhaps a broad based temporary increase in the compulsory percentage of salary to superannuation might be a broader way to depress current spending, but still allowing those who have earned that money to retain it as savings, rather than effectively transferring it to the bank.”

")