")

")

Are interest rates the only way to control inflation?

Reserve Bank Governor Philip Lowe is painted by many as public enemy number one because of interest rate hikes but is that the only tool at the RBA's and federal government's disposal in the fight against inflation?

Tackling inflation is one of the most persistent and challenging tasks facing any economy.

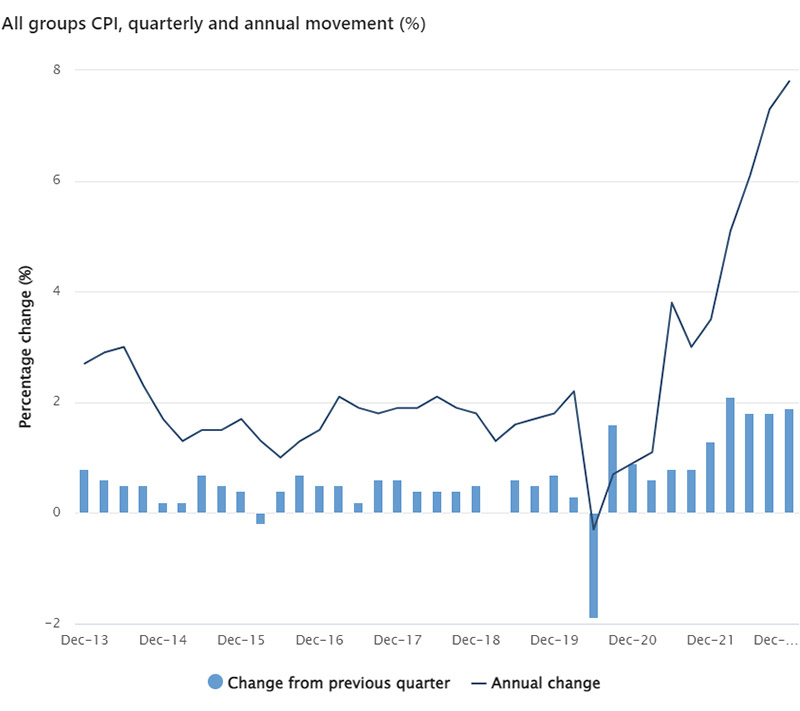

Australia, like most advanced economies around the world, is again wrestling with high inflation, which recently rose to a new 32-year high of 7.8 per cent.

While that is high – the Reserve Bank of Australia (RBA) aims to keep it within the 2 to 3 per cent range – spare a thought for the wage earners of 1951 who were contending with Australia’s highest ever level of inflation, a staggering 23.9 per cent.

Decades later, in the aftermath of the 1982 wage push, inflation peaked around 11 per cent.

In a hopeful indicator for today’s economy, the inflation rate in both those extreme circumstances was quickly brought under control. Within 18 months, the inflation rate of 1982 was back below 4 per cent, while by 1953 it had fallen to 4.92 per cent.

So with the RBA ramping up interest rates, is this the only way to battle inflation?

The main tool in the RBA’s monetary policy arsenal is indeed interest rates. But the government can also introduce fiscal policies to reduce inflation by increasing taxes or cutting spending.

Maria Yanotti, Senior Lecturer in Economics at the Tasmanian School of Business and Economics, said that while the RBA could intervene in the economy through exchange rates, quantitative easing (or printing money), and bank lending requirements, interest rates remain its most effective tool.

“The RBA will do a bit of a combination of those things but it’s the interest rates that have the biggest impact, albeit with an accepted lag time, and it's been that way for 30 or 50 years.

“We’ve seen how damaging and pervasive inflation can be in other countries around the world and the RBA is right to be tackling it head-on with higher interest rates.”

Source: Australian Bureau of Statistics - Consumer Price Index - December Quarter 2022.

Ms Yanotti said the federal government could assist by raising taxes, reducing spending and decreasing consumption but that was rarely politically viable.

“The federal government to some degree is cutting spending to rein in the national deficit but the states certainly are not.

“Even if the government does try to intervene to suppress rising fuel or energy costs, that’s probably not going to be enough to really impact wider inflationary pressure.”

One thing that the academics who spoke to API Magazine agreed on was that demonisation of the RBA Governor, Philip Lowe, was unjustified.

University of Melbourne’s Professor of Property, Dr Piyush Tiwari, said that when lowering rates he was seen as a hero and now that they are going up, he’s painted as the bad guy.

“Historically, interest rates are still actually quite low and I fully expect that the RBA will be justified in raising them further over coming months.

Ms Yanotti said it was politically expedient to have a scapegoat to target and pin the blame on but argued the RBA had only responded to the economic climate of the time when it lowered rates to near zero, and has subsequently done what is necessary to curb inflation that has since followed.

Sam Tsiaplias, Principal Research Fellow in the Macroeconomics Research Program at University of Melbourne, said interest rates are not the only way to combat inflation, “although they are the primary means by which the RBA attempts to control inflation.”

“Government policies are also relevant, particularly in terms of policies that can ease cost of living pressures, for example, policies aimed at reducing the size of energy bills can help ease inflationary pressures associated with rising energy prices.”

Was printing money to blame for high inflation?

Initiating an emergency stimulus package, the RBA in late 2020 began buying hundreds of billions of dollars worth of government bonds, in what effectively amounted to printing money. The program ran from November 2020 to February 2022, and saw the RBA buy $281 billion of federal, state and territory government bonds.

Was this increase in the pool of money necessary and did it contribute to higher inflation?

The RBA defends itself against the claim that its money printing was responsible for the inflation we're experiencing now because, to simplify its complex argument, the money it printed did not, strictly speaking, enter the economy.

“While inflation has increased following the bond-purchase program, it is not clear that this can be explained by the Quantity Theory,” an RBA review into its bond purchase program noted.

“Different components of the money supply can move independently over time.

“While the bond purchase program led to a sharp increase in exchange settlement balances and thus ’base’ money, the increase in the broader money supply, which is relevant for nominal expenditure in the economy, was not as large,” it said.

Which is RBA-speak for, the money wasn’t really a contributor because it didn’t land in people’s pockets to be spent.

University of Tasmania’s Ms Yanotti said, however, said that governments around the world resorted to so-called quantitative easing and are subsequently all experiencing an inflation hangover.

“It was necessary at the time to stimulate stagnant economies, through job keeper schemes, expansionary monetary policy and the like but it did fuel inflation and it’s now necessary to decelerate the economy.”

Professor Tiwari said the RBA acted wisely at the time but appeasing the public was always going to be a difficult process.

“The stimulus generated by quantitative easing and the lowering of interest rates and their subsequent return to a more normalised range was always going to be a difficult juggling act.

“Precise timing is difficult,” he said.

For those who prefer to demonise the RBA Governor, it appears likely there will be ample fuel for that fire in coming months.

“There’s definitely room for a couple more rate rises in the coming months,” Professor Tiwari said.

Builders bracing for more rate pain

According to the Housing Industry Association’s economic and industry Outlook Report released Tuesday (21 February), the number of detached houses commencing construction is set to decline this year and next to its lowest level since 2012.

HIA Chief Economist, Tim Reardon, said interest rates had ended the building boom.

“The 2022 cash rate increases were sufficient to bring this building boom to an end and further increases in 2023 will accelerate this downturn,” added Mr Reardon.

“There was a large volume of work in the pipeline when rates started to rise in May 2022, and there remains a record number of homes under construction, but this will shrink quickly as market confidence continues to fade.

“Lending for the purchase or construction of a new home had already fallen to its lowest level since 2012 by the end of 2022, and the full impact of last year’s rate increases is still to flow through to households.

“This will see the number of detached housing starts fall below 100,000 starts per year for the first time in a decade to just 96,300 in 2024. This is a very rapid slowdown from the 149,000 starts in 2021.

“Multi-unit starts were impaired last year by the acute shortage of labour and materials that has seen many projects postponed until 2023.”

Unlike detached home construction, he said the number of multi-units commencing construction should increase as the acute shortage of housing, returning migrants and students, and affordability constraints continue to drive demand for housing.

“It is unfortunate that the RBA appears set to repeat the cycle the building industry experienced after the GFC.

“Following an initial cut to rates, the RBA then increased rates quickly, bringing the building industry to a stall, before being forced to cut rates again to avoid adverse impacts on the wider economy.

“It is also unfortunate that higher rates will further impair the ability of the market to respond to the acute shortage of housing stock.

“One policy tool at the disposal of government is to ease the barriers put in place in recent years that restrict first home buyer access to a mortgage.

“Over a decade of macro prudential restrictions have seen borrowing for those with less than a 20 per cent deposit become increasingly expensive and this inevitably leads to banks increasingly lending to those that already own a home.

“Easing the barriers to home ownership need not undermine the efforts of the RBA or the government to reduce inflationary pressures,” Mr Reardon said.

RBA unrepentant

Mr Reardon may be in for more disappointment, if Mr Lowe’s recent appearances before two parliamentary committees: the Senate Economics Legislation Committee and the House of Representatives Standing Committee on Economics, is any indication.

Mr Lowe was unrepentant about the prospect of further interest rate increases and doubled down by saying the bank may not be going hard enough.

While acknowledging interest rates were a blunt instrument to control inflation, he said people had forgotten how corrosive high inflation could be.

He also acknowledged that there was a risk that companies and consumers might cut back on borrowing and spending so much that the economy is pushed into recession but he insisted the scourge of inflation was so damaging that it had to be the RBA’s primary focus.

")