")

")

Imperfect 10: RBA lifts interest rates for tenth time in a row

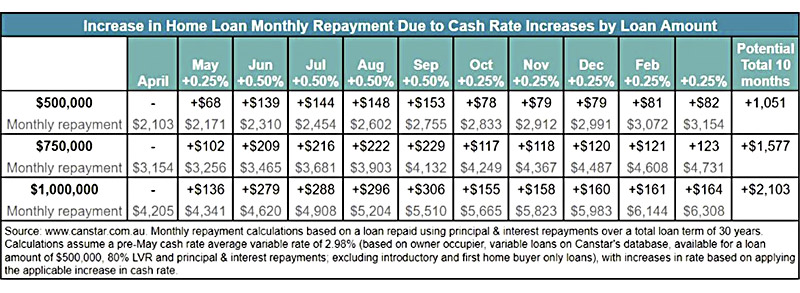

Borrowers have been hit with a tenth consecutive interest rate rise, adding more than $1,000 to the average monthly mortgage since the first rise back in April.

The Reserve Bank of Australia (RBA) has raised the cash rate 25 basis points to 3.60 per cent, hitting mortgage holders with a tenth consecutive interest rate increase.

Borrowers coming to terms with a 50 per cent increase in repayments since April 2022 will need to work the equivalent of an extra 29 hours per month to keep pace with repayments, according to analysis from Canstar.

The pain inflicted on working households by continued interest rate hikes was underscored by data released Tuesday (7 March) showing that for the December quarter 2022, company gross operating profits rose 10.6% compared to just 2.6 per cent for wages and salaries.

Interest rates are now at their highest level since May 2012 and with an inflation rate of 7.8 per cent still eroding earnings, more interest rate increases in the immediate months ahead cannot be ruled out.

Today’s hike adds roughly $160/month to repayments on a $500,000 variable rate owner occupier mortgage. Since the rate hiking cycle commenced in May, mortgage repayments on a $500,000 home loan have increased by just over $1,000/month for owner-occupiers.

The hawkish tone of RBA Governor Philip Lowe made it clear more interest rate increases were around the corner.

“The Board expects that further tightening of monetary policy will be needed to ensure inflation returns to target and that this period of high inflation is only temporary,” Mr Lowe noted in his monthly Monetary Policy Decision.

“In assessing when and how much further interest rates need to increase, the Board will be paying close attention to developments in the global economy, trends in household spending and the outlook for inflation and the labour market.

“The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that.”

Those words closely mirror the ones used to justify previous interest rate rises and should elicit nervousness in Australian borrowers.

Mr Lowe said the Board recognised that monetary policy operates with a lag and that the full effect of the cumulative increase in interest rates is yet to be felt in mortgage payments.

He also offered a rare admission that the unbroken run of ten interest rate rises was a source of anguish for many.

“There is uncertainty around the timing and extent of the slowdown in household spending.

“Some households have substantial savings buffers, but others are experiencing a painful squeeze on their budgets due to higher interest rates and the increase in the cost of living.

“Household balance sheets are also being affected by the decline in housing prices (and) another source of uncertainty is how the global economy responds to the large and rapid increase in interest rates around the world.

“These uncertainties mean that there are a range of potential scenarios for the Australian economy,” he said.

Mortgage and renter pain

The number of new housing loans for owner-occupiers and investors fell 30 per cent and 27 per cent respectively in December 2022 versus December 2021, according to ABS data.

This will likely put even more pressure on rental prices, as more people continue renting rather than opt to buy a home.

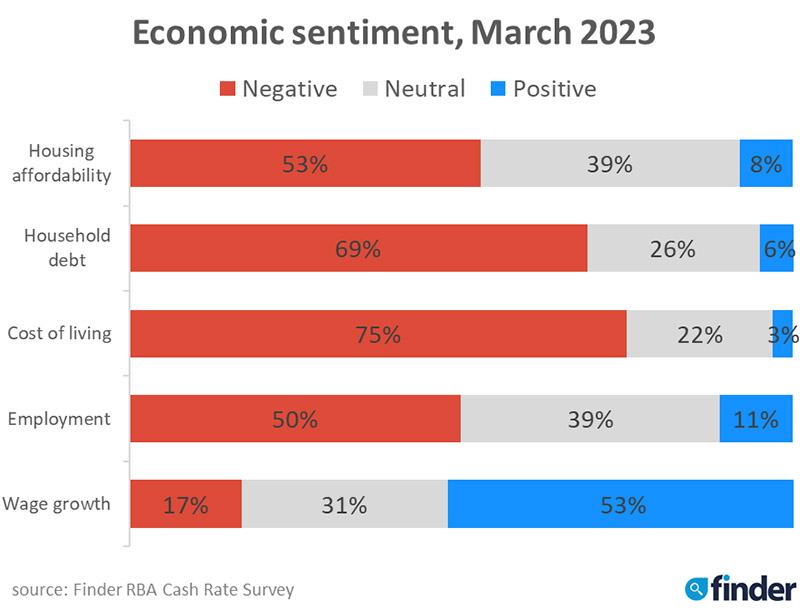

A whopping 36 per cent of Aussie homeowners said they struggled to pay their mortgage in February, according to Finder’s Consumer Sentiment Tracker. Almost half of Aussie renters (43 per cent) said they struggled to pay their rent last month.

Mala Raghavan, Head of Discipline (Economics), University of Tasmania, said there is currently a limited supply of rental properties with a low vacancy rate in the market.

“With fewer Australians buying homes, coupled with the inflow of international students and foreign workers, the demand for rental properties will increase, putting significant pressure on landlords to increase rental prices,” Raghavan said.

Relief still seems some way off, with more rate increases tipped for the coming months.

Households, meanwhile, continue to stress about a range of financial variables, including cost of living, debt and housing affordability.

Economist Harry Murphy Cruise of Moody’s Analytics said inflation remains bitingly high, forcing the RBA to keep hiking interest rates.

“While the worst of the inflation pressures are likely in the rear-view mirror, a meaningful price reprieve is still some time away, and as such, we expect consecutive rate hikes at the next two meetings, taking the cash rate to 3.85 per cent.

“In better news, earlier rate hikes are starting to have an effect: unemployment is lifting, retail sales volumes went backwards in the December quarter and wage rises have been lower than feared, so this should keep interest rates under 4 per cent.”

Online property exchange network PEXA’s latest Property Insights Report confirms the ‘affordable housing’ segment of prospective buyers is feeling the pinch the most.

“The largest drop in settlement volumes in 2022 was for properties priced below $500,000,” PEXA Chief Economist, Julie Toth said.

In New South Wales, the number of property settlements priced under $500,000 dropped by 34.8 per cent in 2022 compared to 2021, according to the report. In Victoria, it fell by 7 per cent, while in Queensland it fell by 12.8 per cent.

“This trend confirms that the effects of rising rates are being felt disproportionately by buyers seeking lower-priced homes, further exacerbating Australia’s pressing need for affordable housing,” Ms Toth said.

Building industry hurting too

Given that more than 90 per cent of economists and academics predicted the latest official cash rate increase, few people are doubting the necessity of tackling the scourge of inflation.

Mr Lowe’s nine paragraph Monetary Policy Decision makes 18 references to inflation. While the RBA is watching retail and household spending, unemployment, GDP, wage growth and global developments, inflation is the target and interest rates the tool.

The building industry is another casualty in the interest rate hike cycle.

New home building activity has dropped to its lowest monthly number in over a decade, decreasing by 27.6 per cent in January alone. Separate lending data shows that loans for the purchase of new homes have fallen to their lowest level since November 2008, according to the ABS’s January figures.

Rising inflation and interest rates have already forced building and construction activity to slow sharply making it much harder to deliver the housing and infrastructure needs for Australians, according to Master Builders Australia CEO Denita Wawn.

Today’s RBA statement notes how accelerating rental prices are already contributing to inflationary pressures across the economy. Further interest rate increases will deepen the new home building downturn and magnify these rental market pressures.

“While we recognise the RBA will likely need to continue to lift interest rates over the next few months to reduce the risk of locking in high inflation, there’s more that can be done to avoid locking a generation out of homeownership and exacerbating our housing supply and affordability challenges.”

Ms Wawn said beyond the blunt tool of interest rates, the upcoming federal budget should focus on policies that ensure spending is carefully targeted at boosting productivity for business and allowing for more favourable outcomes when it comes to the cost, quality and quantity of building and construction output.

“Insufficient supply of titled residential land, high developer charges, and inflexible planning laws are also holding back detached house building.”

")