")

")

Will property prices keep rising in 2023?

Soaring interest rates, mortgage cliffs, more households in financial stress; it seems whatever is thrown at the real estate market at the moment is brushed aside as property prices keep rising.

You kind of have to wonder what effect all these interest rate rises are having on very much at all?

There is no doubt they’re affecting low and middle income earners, with the average mortgage holder and renter now deemed to be in financial stress.

But property prices have continued to rise for five consecutive months, rents continue to skyrocket, retail spending goes on unabated and inflation refuses to budge.

Interest rates are rising in response to inflation, as we know, but among the basket of goods included in that inflation figure are rent and energy costs.

In a perverse catch-22 scenario, rents are being forced upwards by higher interest rates that are driving landlords out of the market and reducing the supply of rental properties, while energy price pressures have nothing to do with interest rates and all the rate rises in the world won’t bring power prices, and therefore inflation, down.

First home buyers and renters may have thought there might be a silver lining in it for them as relentless interest rate hikes delivered lower property prices but that’s not happening either.

So, as this cycle of seemingly ineffectual rate rises goes on and on, with Reserve Bank of Australia (RBA) Governor Philip Lowe making it pretty clear the escalation will continue, how long can property prices continue to grow and how much pain can borrowers and renters withstand.

Property prices marching upwards – for now

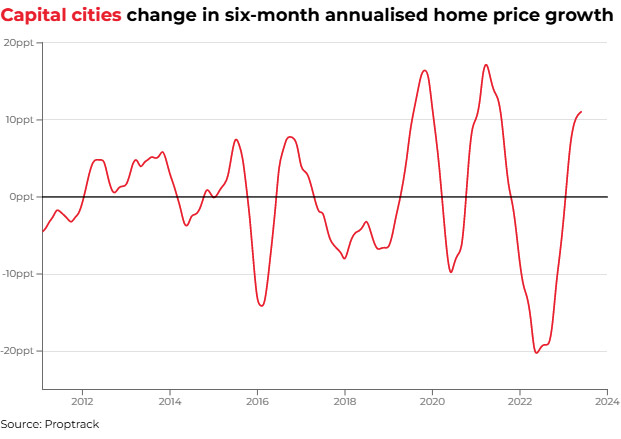

The housing market has started this year on a stronger footing, and after five consecutive months of national home price growth, stronger market conditions are becoming more pervasive and price rises becoming more widespread.

In May prices rose in every capital city except Darwin. Every rest of state area also saw prices rise, except regional NSW and regional Victoria.

The PropTrack Home Price Index released this week showed the current price rebound continued in May with price rises becoming more widespread and broadening across markets.

National home prices have now increased for the fifth consecutive month, rising 0.33 per cent in May, and are up 1.55 per cent year-to-date.

This continued lift in May brings national home prices up 1.03 per cent over the past quarter, the strongest pace of quarterly growth since the March quarter of 2022 when prices peaked.

So, what’s offsetting the pressure of interest rates?

Migration is a big factor.

The arrival of around 235,000 people per year from overseas means around 100,000 homes or more need to be found. This comes at time when the government is trying to address a shortfall of a million homes by building 200,000 a year. So it’s going to be at least a decade for that shortfall to be overcome and with new home approvals and builds plummeting, the betting money suggests that’s optimistic.

Migration is putting property price pressure on all capital cities. As more international migrants land in populous Sydney and Melbourne, interstate migration from there feeds the Western Australian, South Australian, Queensland and regional property markets.

A lack of land and housing supply is also bringing a sense of FOMO to the marketplace.

Although supply constraints eased slightly with respect to the total stock on market in some regions, the flow of new listings remains soft, keeping a floor under prices with sellers benefitting from lower competition with other vendors.

Property price pressure remains upward

An estimated 880,000 Australian households with fixed-rate mortgages expiring this year will need to find thousands of dollars more each month to meet repayments, as an era of cheap rates is replaced by higher variable rate loans.

That mortgage cliff looms as borrowers with the average mortgage of $576,985 are having to find an extra $15,000 a year compared to when rates were at their nadir in April 2022.

But Eleanor Creagh, Senior Economist, PropTrack, said the decision by the Reserve Bank to lift the cash rate in May did not deter the current home price rebound, in fact it was the opposite, with price rises broadening across markets and remaining resilient to the falls the calculated shift in borrowing capacities would imply.

“Interest rates may still rise further, and the economy is also expected to slow, which may weigh on home prices in the months ahead but with the bulk of interest rate tightening in the rear-view mirror and the peak in sight, much of the uncertainty buyers have experienced with respect to borrowing capacities and mortgage servicing costs is subsiding, meaning a better sense of how far their budgets may go,” Ms Creagh said.

“A home shortage exacerbated by high construction costs will also underpin values as population growth increases.

“We expect home prices to continue to lift in the months ahead, buoyed by population growth, rental market tightness, and an undersupply of new homes, with a return to positive annual price growth expected across most capital city markets in the coming months.”

But there are signs of market fragility

Speaking to API Magazine, Tony Kelly, Managing Director of VicTas, Herron Todd White, said a two-speed property market was emerging.

“The impact of interest rate increases can take up to 18 months to filter through so it may not be until late this year that we can really see the impact they have had and how the property prices react,” he said.

“Although some statistics indicate an increase in property prices across the market, the market is more fragile right now than many realise.

“From a valuer’s perspective, it doesn’t feel as though the market is growing or aggressive, as is evidenced by the increase in expression of interest sales and a reduction in auctions campaigns taking place.

“The upper end of the market is much stronger than the bottom end, those who can afford to buy are continuing to do so which is driving up the average price increases represented in the industry statistics.”

Traditionally, as Spring selling season approaches the number of homes for sale significantly increases, about which Mr Kelly said one city would be a bellwether for the wider market.

“The performance of a robust market like Melbourne’s will be a real indicator of the market’s strength.

“Melbourne is more stable than most capital cities as there is less fluctuation than Gold Coast, Sydney or Perth where the markets move quicker and there are more variables like tourism or a transient workforce.”

Any respite for renters?

Since the onset of Covid, capital city rents have risen 25.7 per cent and regional rental values have increased 29.2 per cent, adding the equivalent of $125/week and $116/week to the respective median rent.

More than 40 per cent of Australian house and unit markets have recorded a double-digit rent increase in the past year.

A surge in overseas migrants and international students coupled with a significant shortfall in rental listings has led to the strongest annual rental increase on record for Australia’s capital cities.

It's now cheaper to buy than rent in many areas.

While rents are falling, there are signs that the pace of price hikes may be easing.

CoreLogic’s national rental index shows the rate of rental growth has softened slightly, with rents up 0.8 per cent in May compared to the 0.9 per cent and 1 per cent increases in April and March respectively.

CoreLogic Economist Kaytlin Ezzy said the slowdown in the monthly growth rate had contributed to a fall in the annual trend, which dipped below double digits for the first time in 10 months, with rents nationally increasing 9.9 per cent over the 12 months to May.

However, she added this was largely being driven by a slowdown in regional markets, where rents increased 0.3 per cent over the month, down from a record monthly growth rate of 1.2 per cent in March 2022.

“Regional rental growth has slowed dramatically from a year ago while capital city rents were up 1.0 per cent in May.

“When you break that figure down further by property type, we can see the unit sector is under the greatest pressure, with rents increasing at a faster rate than houses due to their relative affordability.”

Mr Kelly said job security and population growth were the two biggest impacts on the housing and rental market right now.

“This market cycle has been different to many periods of financial strain in the past, as job security has remained high, which gives confidence to consumers to continue spending and the economy doesn’t cool down, it causes inflation to continue.

“The government is in the difficult position of needing labour to fill key roles and boost the economy, but with the current vacancy levels the more people simply equates to more demand and the more intense the housing crisis.”

")