")

")

Where does Australian property stand on the world stage?

Depending who you listen to Australians are drowning in debt and real estate prices will tumble, or it offers the strongest growth prospects among a raft of major global economies.

Australians love to compete on the world stage and compare themselves to their overseas peers and when it comes to our property market there’s much to like about our prospects but still a fair bit to instil some fear.

While the forecasters often get it wrong, most international observers – with the notable exception of the International Monetary Fund (IMF) – see plenty of upside in Australian property markets compared to other global cities.

A sign of how quickly perceptions can turn around is evident in the massive reversal published this week by international credit rating agency Fitch Ratings.

“Australian home prices are recovering and are expected to grow 2 to 5 per cent, a turnaround from our original 2023 forecast of minus 10 to minus 7 per cent.”

That’s quite a turnaround.

The agency’s 2023 Global Housing and Mortgage Outlook Mid-Year Update made similar revisions over the past six months for Japan (home prices are forecast to increase at 5 to 7 per cent, instead of 2 to 4 per cent), Spain (down to 0 to 2 per cent from 2 to4 per cent in 2023), and Canada (to decline by 5 per cent to parity in 2023, a less severe drop than our previous forecast of minus 7 to minus 5 per cent).

Among some of the larger global markets and others with similar scale to Australia’s, the land Down Under offers the strongest growth prospects, while China, the United Kingdom and United States are essentially expected to flatline or deliver very modest growth.

But it’s not all plain sailing for Australia, or indeed other national property markets.

The pandemic propelled housing prices to record levels in many countries, especially advanced economies, amid low interest rates and tight property supplies. Then prices started falling late last year in many countries, while others saw the pace of gains slow.

As the IMF’s Nina Biljanovska, Economist at the Macro-Financial Division of the Research Department, pointed out, the deterioration was more pronounced in advanced economies with signs of stretched valuations before and during the pandemic.

“With central banks raising interest rates to contain inflation, the average mortgage rate reached 6.8 percent in advanced economies in late 2022, more than doubling from the start of last year.

“Now, if borrowing costs keep rising or remain elevated for longer, demand and prices are likely to weaken further,” Ms Biljanovska said.

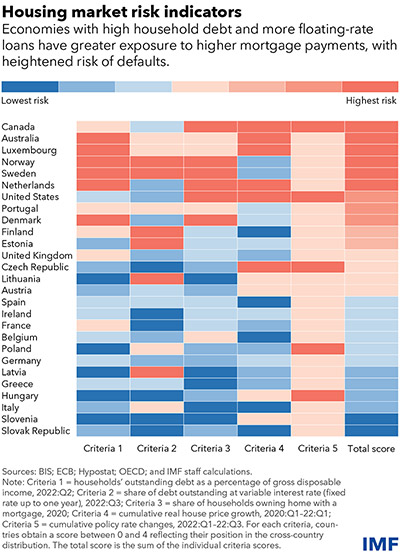

She pointed to data from the Organisation for Economic Co-operation and Development, a group of 38 mostly advanced economies, to single out Australia, Canada, Norway, and Sweden as being at the greatest risk.

But any global property downturn is unlikely to be on a global financial crisis (GFC) scale at least.

“There are important differences between current conditions and the GFC a decade and a half ago,” Ms Biljanovska said.

“In most cases, while it is unlikely that falling home prices will spark a financial crisis, a sharp drop in house prices could dim the economic outlook and the build-up of vulnerabilities warrants close monitoring in coming years – and possibly even intervention by policymakers.

“Banks are better capitalised than before the GFC and underwriting standards in many advanced economies are tighter today than before the crisis.”

But there were still some parallels in the risk assessment between today and that global economic upheaval of 2007-08.

“The average household debt-to-income ratio across countries is about the same as in 2007, driven mainly by households in economies that managed to escape the brunt of the GFC and have since run up substantial borrowing.”

Household debt Australia’s big issue

If the healthy Fitch Ratings projections are to reign over the IMF’s more downcast outlook, Australian property demand is going to need to overcome a couple of significant financial hurdles.

While a lack of housing supply and a steadily growing migrant population are adding pressure to prices, Australians are also financially stretched, with a home price to after-tax income ratio of more than 12 times.

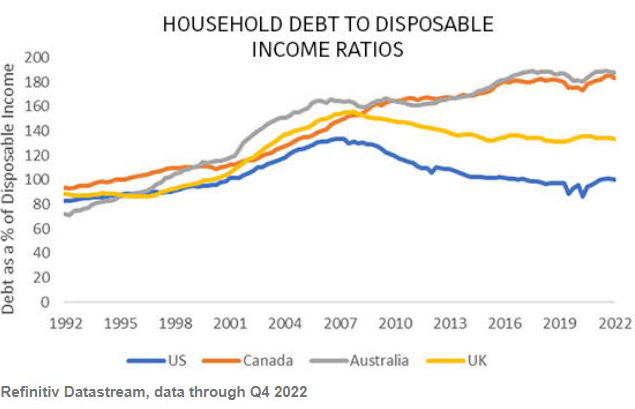

Russell Investments, an investment firm based in Seattle, this week issued The Global Housing Inspection Report 2023 Edition, in which it pointed out household debt to disposable income ratios continue to remain elevated in Australia and Canada, putting further pressure on the housing markets in these regions.

“Gone are the days of financing a home for 3 per cent interest,” the report noted.

“With central banks in all four regions (in graph above) aggressively hiking interest rates, new homeowners will feel the sting as they try to obtain financing for their purchase and in countries with a high proportion of homeowners who have variable rate mortgages, even existing homeowners won’t be spared.”

Global forces at work on real estate

While governments, policymakers and industry like to think they are the masters of their own domain, the reality is global factors play as big, if not a greater, role in shaping the trajectory of property markets than local factors.

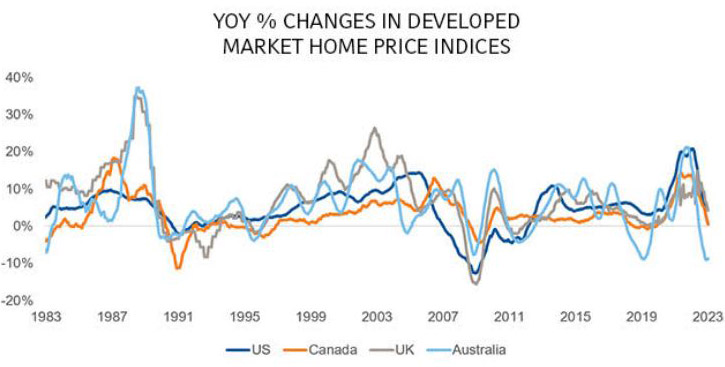

War in Europe, post-Covid economic recovery, and subsequent global inflation have led to property markets in the US, UK, Canada and Australia marching in lockstep for the past few years. But this general pattern of these property markets trending along a similar path dates back as far as 1983.

Source: Russell Investments, using Refinitiv Datastream data.

The effect of central bank monetary policy tightening has taken a noticeable toll on developed country housing markets.

“In more recent months, promising signs of a potential rebound greeted investors – in Canada, the Home Price Index saw four straight months of month-over-month percentage increases, meanwhile, a similar trend occurred in Australia, with home prices increasing from May to June,” the Russell Investments global report noted.

But there was a but.

“However … we believe it may still be too early to officially call the bottom of the housing market.

“With interest rates continuing to remain at elevated levels, the residential housing market will likely face continued headwinds in the near term.

“In fact, in places like Canada and Australia, the rebound in house prices was actually one of the catalysts for the central banks resuming rate hikes after an initial pause.”

Australian property outperforming most

While Australia property price are on the incline, the same can’t said of other major markets.

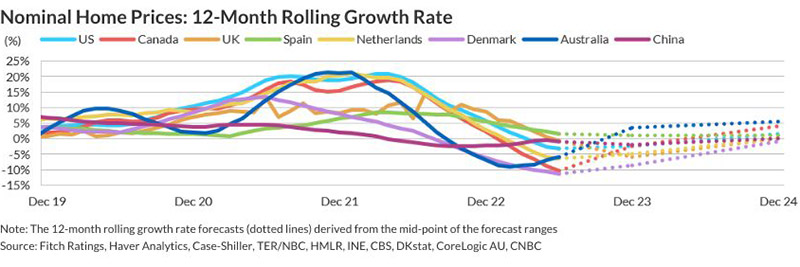

According to Fitch Ratings US home prices will experience modest growth for a year, attributed to a short-term dip in interest rates earlier this year and record low inventory. However, rates have since gone back up, and a mild recession later this year could lead to housing market softening.

Source: Fitch Ratings.

UK home prices are expected to continue to fall this year and into the first half of 2024 as a result of increased mortgage rates and falling real wages. The Netherlands’ home price index peaked in 2022, and further declines will be limited due to a tight labour market, low housing supply, and government support for homebuyers.

China’s home prices are at or near the bottom, with overall home buying sentiment still weak.

An interesting six months looms for the global market and Australia’s position within it, with observers set to learn whether the bulls or bears prevail.

")