")

")

Endure economic wild cards through long-term investment planning

An unpredictable property market is surprising agents with unexpected sales highs and lows, while economic wild cards are a source of uncertainty, but a winning strategy for buyers is long-term planning.

The nation’s economists sat glued to their screens while journalists confidently predicted interest rates would not rise in April. As far as they were concerned, the next move would be towards the end of the year and that move would be down.

Then, the Board of the Reserve Bank of Australia struck, lifting the official cash rate to 3.85 per cent.

While everyone was reading the confident headlines, Philip Lowe, Governor of the RBA noted in his statement, “Inflation in Australia has passed its peak, but at 7 per cent is still too high and it will be some time yet before it is back in the target range.”

If there was any doubt, his statement went on to say: “Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe.

That set up quite a reaction in the real estate market. Many players had assumed the worst was over and were predicting a late property boom for 2023.

Where are we in the property cycle?

The short answer is, just off the back of an extraordinary boom.

In technical terms a post-boom stagnation, but that description quite unhelpful and perhaps a better label would be “foggy bottom”.

In this phase investors, buyers and agents are groping around trying to identify whether the recent drop off is continuing or whether the bottom has been reached and we can set our sails for growth.

Importantly, real estate data throws up contradictory pictures of where the market is at.

Zoe Goh, buyers’ agent, and a colleague with Property Mavens, works across Melbourne’s northern suburbs and describes her patch as unpredictable.

“Houses which promise to be dead as the morgue record a $100,000 over reserve price on auction day yet sure-fire sales with lots of interest beforehand see bidders evaporate without a trace when it comes to the crunch but interestingly, we’re seeing the same sort of volatility in C-grade properties on the market as with the investment grade houses and units we target for our clients,” she said.

Another colleague, Anjay Zazulak, buyers’ agent and vendor advocate, Property Mavens in Sydney has told me that while results for Sydney’s investment grade property are more predictable, volatility in sales outcomes is higher than it’s been for many years.

Market uncertainty is driven by the conflicting signs

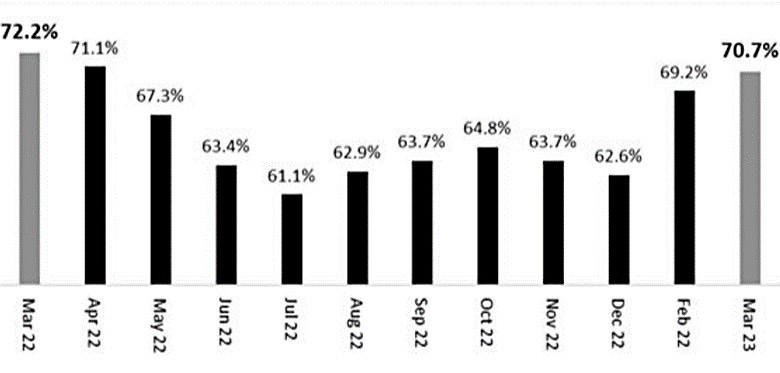

Let’s take the Melbourne auction market as an example. If you were looking at the clearance rate alone, you could be forgiven for thinking we’re in a boom. There was a reported clearance rate of 78.1 per cent for Saturday, May 6, well ahead of the 66.4 per cent clearance rate for the same weekend last year.

That result was for 644 auctions, below the 767 listed over the same weekend last year and 2019 where auction numbers above 1,000 were common.

While there’s been an uptrend in clearances this year, there’s also been quite a bit of movement over the last 12 months suggesting buyers are still making up their minds.

Source: Kay & Burton, A Wilson.

Are we there yet?

Perhaps the most useful way to think of the market now is to picture it as a game of rugby.

On one side, we have positive forces striving to push the market forward - think of players as a surging rate of migration, good employment outcomes, a rebound of overseas interest and a lack of supply of properties for sale.

Now factor in the weight and strength of the opposing side. Start with players like the potential for more interest rate rises, weakening economic conditions and the outbreak of consumer uncertainty, anyone of which could cause another downwards drift in property sentiment.

At present, these competing factors are grinding up against each other but at some point, one side will gain an advantage and race away.

When can we feel sure the worst is behind us?

The outlook for home prices remains mixed, however over the medium to long term, I’m much more confident.

Interest rates remain a wild card, but monetary policy is now confronting inflation which appears to have peaked both here and across the advanced world, including the always important America.

While the RBA will act to keep the inflation bear in its cage (and not move too far from US interest rates) the scope for further rises has fallen.

If rates begin to look like they have peaked, keep your eye on the number of people gaining approval for new mortgages.

At present, finance commitments have decreased markedly from the same time last year with new owner-occupier mortgages down 33 per cent and investors down 35 per cent. If that trend starts to move up, you can be sure house prices will start rising.

Then there’s Australia’s surge in migration, set to hit 190,000 people in 2023-24. This is occurring against a background of a sizeable shift of rental properties to short term accommodation.

That is priming the case for continuing rent increases which is already enticing some investors back to the property market.

There’s the other elephant hiding behind the data – the large unmet demand for housing from younger Australians.

As we’ve seen over the last two decades, it only takes the smallest encouragement (think grants or falls in interest rates) to produce an outsized response from first time buyers.

In summary, nearly all the long-term factors are positive now, it’s mostly shorter-term elements holding the market back.

When we see some signs such as a rise in financial commitments, strong auction clearance rates and consistently good sales outcomes despite an increase in the numbers of properties for sale then you can be sure we’re in the next cyclical upswing.

If you’re an investor it’s the longer term you should be focused on, just ensure you buy a property with all its elements working in your favour.

")