")

")

Do government incentives skew the market?

Grants and incentives are welcomed by first home buyers and others given the chance to dip into taxpayer coffers, but their consequences are not always as the government intended.

Over the years we’ve all heard about government incentives.

Whether they have been state or federal, tax relief or handouts, they’ve been numerous and not all of them have been as effective as intended. Some have had unintended consequences.

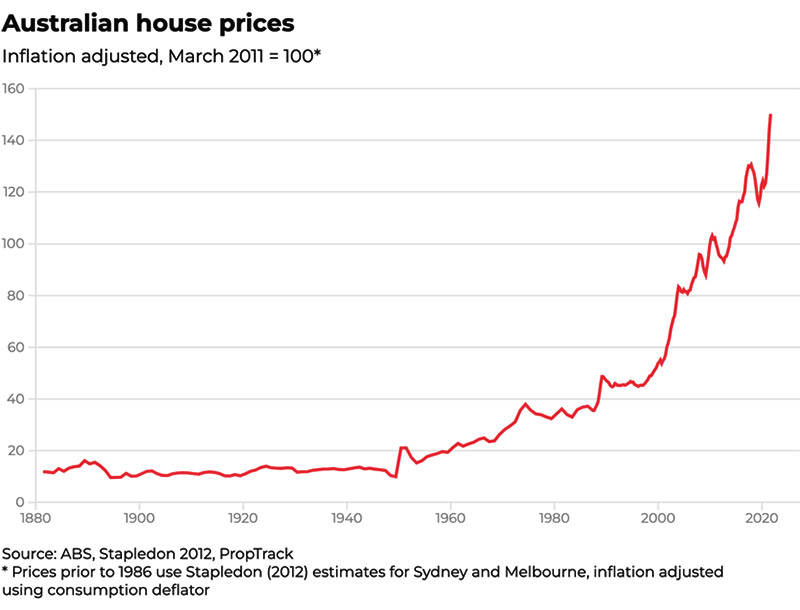

The very first incentive dates back to post-World War II, when returning servicemen and women were offered 45-year loan terms to enable these first home owners to re-establish themselves. It’s hard to tell if it skewed the market, given population growth kicked in heavily during this time. But property prices certainly moved very fast, in fact 1950 remains the headiest growth year during our last 140 years of recorded Australian property price history, when prices grew a whopping 111 per cent.

Additional source: realestate.com.au

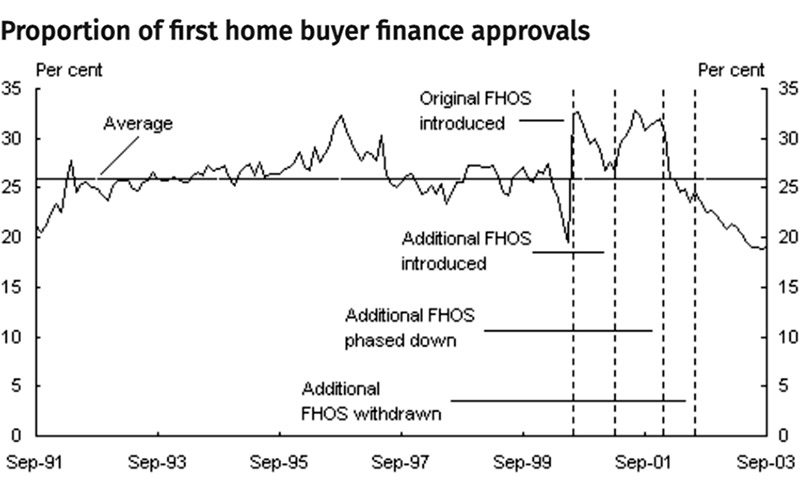

Australia’s first homeowners’ grant was announced in 2000 to offset the effects of the GST.

Variable interest rates were around 7 per cent at the time (with 5 per cent cash rate), and quickly jumped around 125 basis points. The banks enjoyed the solid increase in first home buyer activity for a short period, but the most intense burst of this cohort was yet to come, some nine years later.

Source: theadviser.com.au

Let’s cast our minds back to ‘Kevin-07’ Rudd Government and the nationwide grants (and boosts) that were passed out to first home buyers.

In the wake of the Global Financial Crisis (GFC), the government announced that the grant was to be doubled to $14,000 and a boost of an additional $7,000 for all first home buyer brand new purchases was to be added to the grant, amounting to a massive $21,000 government gift.

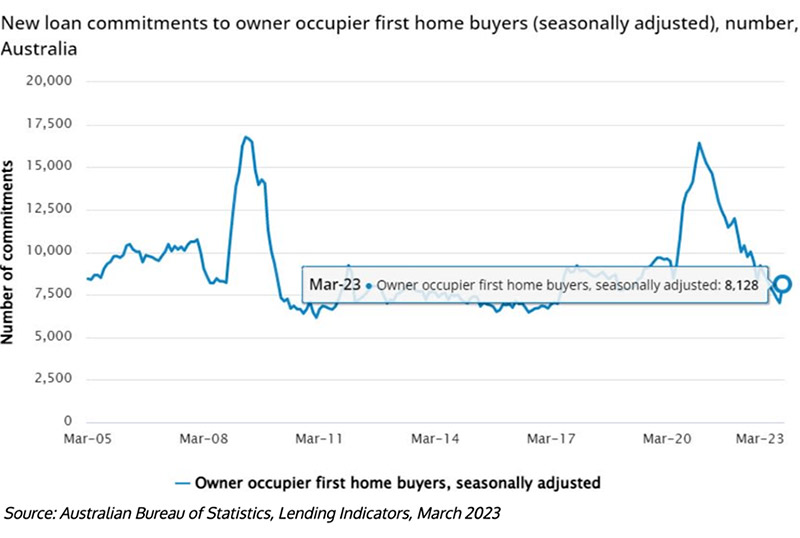

At the time, some lenders only required a 5 per cent deposit, of which the grant could be included in the ‘funds to complete’. Purchasing activity went crazy, and not just among first home buyers, although this chart is quite compelling.

Additional source: treasury.gov.au

What is even more compelling is the impact of low interest rates.

Back in 2009, our cash rate tumbled very quickly from 7 to 3 per cent in response to the GFC.

Not only did first home buyers with their grants and boosts take advantage of the cheap money, but owner occupiers and investors alike did so. Our national house prices surged during this time.

But around a decade later, political cries about housing affordability and investor activity adversely impacting the plight of the first home buyer grew in strength.

In various states and territories, governments introduced all kinds of discounts for first home buyer stamp duty.

Grant recipients battle each other

I recall bidding in Victoria at an auction that attracted predominantly first home buyers.

It was a classic two-bedroom Kensington townhouse, built in circa 1990. The market value at the time was around $600,000, however the discounted duty was capped at a $600,000 purchase.

The bidding opened at $520,000 and bids flew in quick succession to $580,000. Before other bidders had a chance to calculate their bids, I threw out a $600,000 bid. Shoulders slumped, the bidding abruptly stopped, and the property was knocked down to my client. Investor activity was strong, but first home buyers came to the fore once the concessions and grants became available.

Conveyancers and solicitors still laugh about the vast numbers of sales contracts with $600,000 price tags that they processed.

The challenge in the market during this time was that of a two-speed market.

Sub-$600,000 purchase activity was strong, and property sales values in this price segment were overstretched.

The contingent that the government were trying to help were strangling each other with competing bids and offers and driving prices up in the unit market.

Fast-forwarding to the Victorian stamp duty incentive to 2020 following the pandemic, we saw similar problems in the property market when the state government introduced a stamp duty concession for all buyers, (not just first home buyers up to a value of $1,000,000).

Yet again, the two-speed market kicked into gear, leaving $1 million-plus vendors crestfallen, and sub-$1 million vendors excited by the buyer participation and energy.

Sadly, many properties that held market values of circa $950,000 sold for $1,000,000 during this crazy period. Buyers fought hard in this price segment to take advantage of the discount on offer.

Government incentive raises building costs

The last example to ponder is our national HomeBuilder incentive. Nobody could have anticipated Russia invading Ukraine, nor could have we forecast inflation and the impact of rising construction materials, but our lead-times and builder costs went through the roof following this government initiative.

Did it stimulate spending and jobs when we most needed it? Certainly. But the unintended consequences have been significant and distorted the market.

These days, buyer appetite for renovation projects is exceptionally low.

Despite the popularity of reality television shows and stories of sharp profits, consumers know only all-too-well that a renovation or rebuild project will spell delays, hefty costs and overcapitalisation risk.

Land banking has lost its appeal with builders and developers, too. Not only are they facing higher holding costs with tougher interest bills, but onerous rental reforms in some states and territories have made the prospect of renting out a dump to share-house students a costly proposition.

Until our trade shortage levels out and materials costs come back down, our two-speed market conditions will remain.

Could a medium-term outlook spell opportunity for those who can tolerate a run-down or weathered house around them for a few years? Absolutely!

")