")

")

Where property prices are likely heading in 2024, and why

While politicians bicker and grandstand, the residential market remains primed for significant rent increases and capital growth in select capital city and regional areas.

A recent holiday and time spent with friends reinforced one thing – the fixation on where property prices are heading is as strong as ever.

Market sentiment now can best be described as indecisive.

Over the last three months price trends has been inconsistent around the country as people’s expectations of a long term growth contend with the ramifications of rising interest rates.

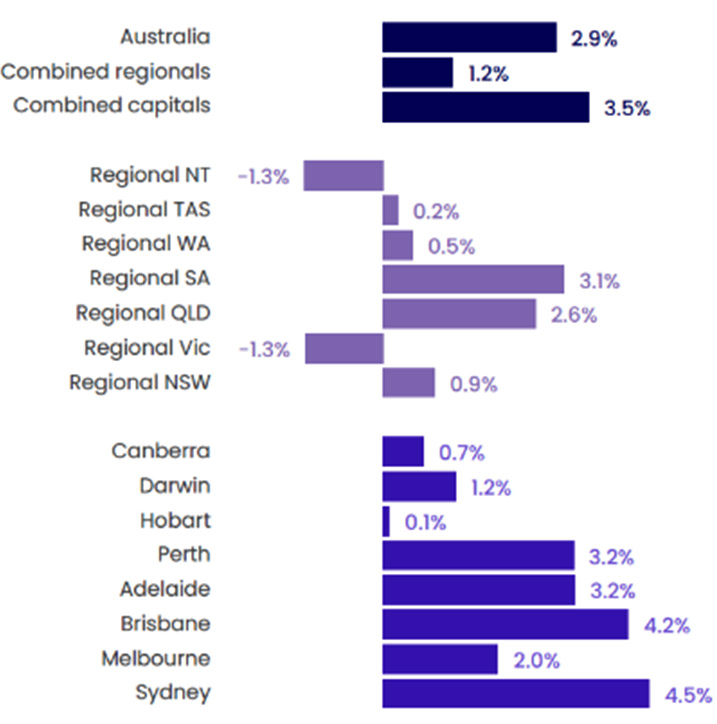

The bigger capital cities are recording solid growth, led by Sydney and Brisbane, while Perth and Adelaide have delivered gains over the past year. Melbourne is emerging from the doldrums and the smaller capitals, Hobart, Darwin and Canberra are floundering somewhat.

In regional centres, only South Australia and Queensland have performed strongly of late but there signs of life elsewhere, as we discuss in this article.

Home price index – three months to July 2023

Source: CoreLogic

Where are property prices heading in 2024?

At the start of 2023, commentators gloomy about property were caught off guard by a burst of price growth that started around March.

That optimism spread from Sydney to other centres until the RBA’s last two rate rises tempered the momentum.

So, how can we forecast what we’re likely to see in 2024?

The best place to start is a review of the factors we know will play a role and make some judgements about how they will play out.

Variable number one is the so-called mortgage cliff, where borrowers have or will be shunted from low fixed rates of around 2 per cent onto variable rates of between 5.6 and 6.2 per cent.

This has been underway for some time and to date, we haven’t seen any major property market impact.

I expect rental growth to hit double digits in 2024.

- Miriam Sandkuhler, CEO, Property Mavens

The average increase in payments for these households is around $900 per month yet interestingly enough, the level of arrears being reported by banks is still below that prevailing in 2019.

The areas most prone to the mortgage cliff are predominantly on the outer fringes of our capital cities as well as in some larger regional centres, like Ipswich Queensland.

To be clear, I don’t expect a tidal wave of defaults. What’s more likely is the combination of higher rates and lower economic growth will see a ratcheting up of pressure in areas with higher debt loads and among owners with lower equity in their properties.

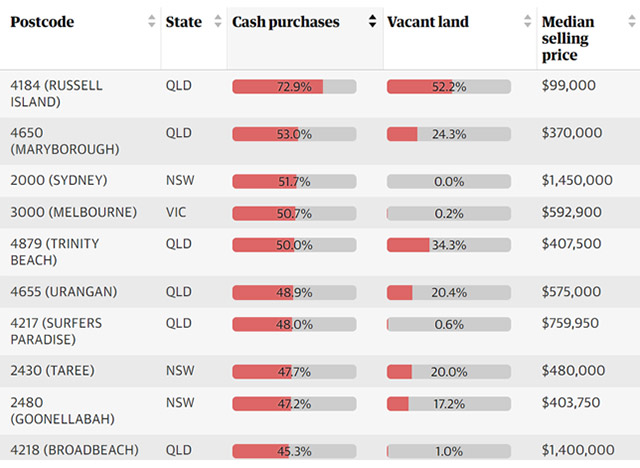

The rise (and fall) of cashed up buyers

One of the more interesting factors this year has been the surge in people buying homes for cash (i.e. without a mortgage).

According to reports by property transaction agency PEXA, a quarter of all buyers on the eastern seaboard settled with cash. While a lot these were in country areas, several suburbs in Sydney, Melbourne, Brisbane and the Gold Coast and Sunshine Coast were also prominent.

The strong cash purchase rates in central Sydney and Melbourne, along with heavy cash buying of vacant land in outer suburbs suggests a return of overseas investors.

Post codes where cash is king

Source: PEXA

But it’s the cashed up Baby Boomers who have been driving most of the growth, especially in provincial areas like Maryborough (Qld) and Taree (NSW) and suburbs like Broadbeach(Qld), Frankston (Vic), and Kellyville (NSW).

While these buyers have been a strong influence this winter, I expect that to wane somewhat over the next year.

Nonetheless, it serves as a reminder that today’s market is less likely to be shaped by couples purchasing with a 10 per cent deposit. If you want to understand where the market goes next, start by tracking buyers with significant resources.

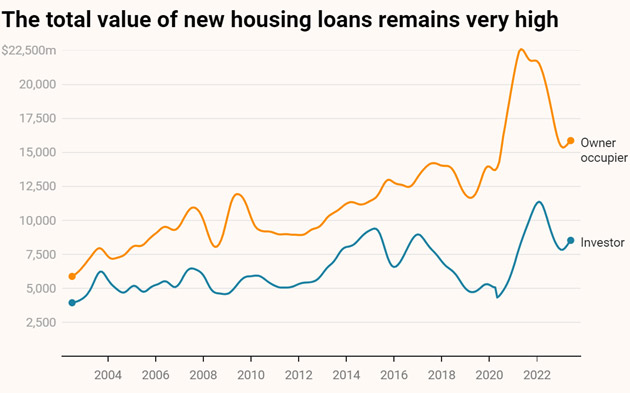

Home loans bouncing back?

Interest rates were a game changer in 2023, checking the market’s growth mid-year.

But have rates peaked? After a year of rises every month, the RBA has now lifted rates in only three of the last five months, meaning we are likely near a peak.

These rises have had a big impact on the number of home loans approved, typically a reliable sign of how prices are likely to travel over the next six to 12 months.

Source: ABS, G Jericho

But it’s interesting to note the value of mortgages has only retreated to its level of 2019. And while the speed of that decline has been rapid, it has now stopped and could be starting to trend upwards.

Rent juggernaut continues unabated

While politicians bicker and grandstand, the residential market remains primed for significant rental growth.

Some investors asked me recently whether the Albanese government’s plan to build 30,000 social housing units would have any impact on market rents.

While undoubtedly great for the people who will be housed, this plan is unlikely to have any discernible impact on rents.

The Rudd Government pursued a similar housing initiative in 2009. It delivered 20,000 units yet did little to alter rents or housing affordability.

As I wrote recently, the factors driving the rental market are structural and to date, nothing has been done to change the dynamic.

Over the last year, rents surged from their 15 year average growth of 3.5 to 6.7 per cent, according to the Australian Bureau of Statistics.

I expect rental growth to hit double digits in 2024.

For landlords, the key period to watch is February and March. In most centres, something like 30 per cent of lease agreements roll over in these two months and that’s when we will see how big the rises will be.

Property market rollercoaster

We expect the rollercoaster ride with Australia’s property prices to continue.

While the overall number mightn’t look that great, below the surface the dynamics will be fascinating.

This year’s growth spurt kicked off with family homes in Sydney’s middle ring and was driven through winter by areas like Melbourne’s prestigious Bayside.

That growth ended with a thud in the outer ring mortgage belt and many of the small regional centres that were the unlikely stars of 2021 and 2022.

In 2024, I expect most of the high performing areas to be inner and middle ring suburbs of capital cities and in larger regional centres like Newcastle, Geelong and Ballarat.

Rent rises will play a much bigger role in 2024 than we’ve become used to, attracting investors and encouraging some renters to try and buy into the more affordable sectors of the market.

The overall market will produce lukewarm results but rewarding returns for shrewd investors.

")