")

")

Rising interest rates presenting opportunity for investors

There is no one-size-fits-all answer when it comes to how interest rate increases will impact investors but property market experts argue it could be an opportunistic time for savvy investors to capitalise.

There is no one-size-fits-all answer when it comes to how interest rate increases will impact investors but property market experts argue it could be an opportunistic time for savvy investors to capitalise.

With Australia’s cash rate having risen to 0.35 per cent earlier this month - the biggest and only increase Australia has seen since 2010 - investors and homeowners alike are pondering what this means for their repayment burden.

The rise is a blow for many Australians already struggling to break into the hot property market, and with the Reserve Bank of Australia announcing more increases are to come, the dream of home ownership is diminishing for many.

Investors are potentially presented with a different trajectory, with industry experts believing the increase presents opportunities for investors.

There is no black and white answer as to how interest rate increases will affect investors according to Bobby Haeri, Co-Director of The Investors Agency.

“There are many different factors which come into play, such as loan to value ratio (LVR), debt to income ratio, cash returns on the portfolio and most importantly the quality of the properties in your portfolio,” he said.

“The rental industry is seeing strong returns and record low vacancy rates, which should mean these increases won’t have a large impact on investors, especially if their properties are positively geared.

“Negatively geared property owners may be out of pocket, but if their circumstances haven’t changed, the buffer the bank has set should mean they can still meet their repayments.

“Investors most likely to be impacted are those who purchased high rise apartments or high-density living and are facing issues finding tenants.”

Mr Haeri said rents will continue to rise, which is good news for investors.

“With an increase in expatriates returning home, a drop in construction approvals along with builders going into liquidation, and the government ramping up migration to assist the economy post-covid, rents will continue increasing significantly in many locations over the next few years, helping to reduce the impact of the rate rises.”

Stressing out

Homeowners experiencing mortgage stress and those looking to purchase their first home will draw the short end of the stick when the rate rises eventuate.

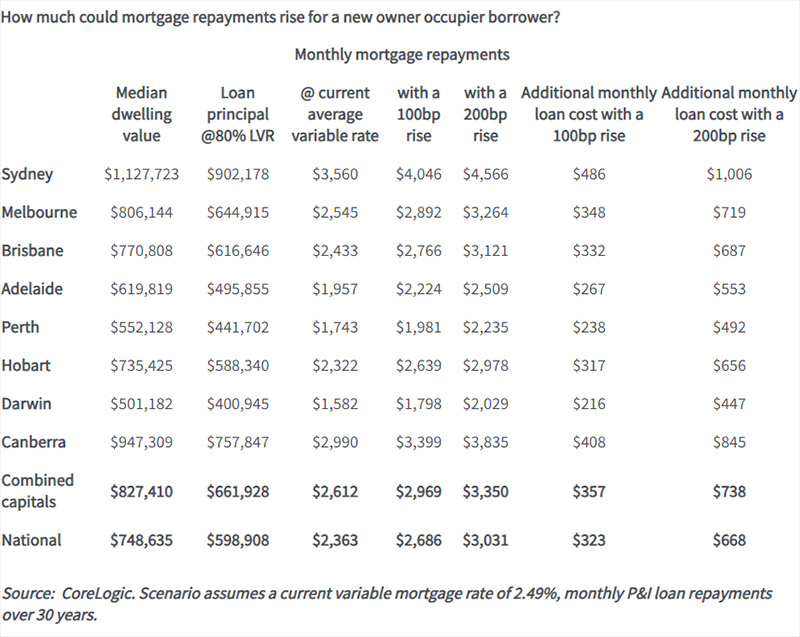

According to Domain’s Home Loans Repayment Calculator, the recent 0.25 per cent increase in interest rates will increase monthly home loan repayments for a mortgage of $750,000 by $99 a month.

By Christmas, if the cash rate hits 1.75 per cent, the same borrower could be paying a total of $443 a month more on their repayments than they were before the cash rate hikes began.

If the cash rate gets to 2.50 per cent by the end of 2023, the same borrower will be paying a total of $651 more on their monthly repayments since the hikes began, according to data released by RateCity.com.au.

James Gerrard, financial planner for FinancialAdvisor.com.au, said owner-occupiers could find themselves in financial distress over the next few years due to the increase.

“Many owner-occupiers have borrowed the maximum from the banks when purchasing the family home with the thought that rates will stay low for a long time so they won't have to worry about rising repayments,” he said.

“However, with interest rates on the rise, some homeowners will no doubt be caught out and fall into financial distress as rates rise.

Through the middle of last year, 45 per cent of housing loans were funded on fixed rate terms, temporarily shielding those borrowers from rate hikes.

The RBA has recently noted in their latest financial stability review the median repayment buffer for owner occupiers with a variable mortgage rate had grown to 21 months of scheduled repayments in February 2022, up from 10 months at the start of the pandemic.

The RBA has also pointed out that non-performing housing loans comprised only 0.9 per cent of the mortgage portfolio at the end of last year, which is below pre-COVID levels.

Even with a two-percentage point rise in mortgage rates, the median repayment buffer would reduce back to 19 months, which is still substantial. With the median household well ahead of their mortgage repayment schedule, the risk of households falling behind on their mortgage is reduced.

Matthew Gatt, General Manager of Home Loans at Compare Club, shared a similar sentiment to Mr Gerrard.

“Similar to investors on a variable rate, first-home buyers will see an increase in the monthly cost of their mortgage, and this will continue to rise into the future if rate rise predictions are accurate for the year ahead,” he said.

“Homeowners who were considering using equity to enter the investment property market will potentially be impacted by lender policy changes in a similar way to investors, where options may be limited and borrowing capacity reduced.”

Heat coming out of market

As the cash rate normalises, there is an expectation housing markets will continue to lose momentum.

A higher cash rate implies higher variable mortgage rates, a reduction in borrowing capacity and tighter serviceability assessments for prospective borrowers.

CoreLogic Research Director Tim Lawless said past research from the RBA has pointed to ‘high end’ housing markets with higher investor concentrations being more sensitive to changes in interest rates in the short term.

“This may be why Sydney and Melbourne markets are already seeing price declines, with more affordable housing markets expected to eventually follow the downward trend.”

Mr Gerrard supported the view that interest rate hikes will reduce Australia’s appetite to purchase the property.

“The impact of rate rises will continue to act as a headwind to the property market but I do not think it will lead to a severe correction,” he said.

“Property markets are heavily driven by sentiment and while we have lingering inflation issues and rising interest rates, this will reduce people’s appetite for property.”

Mr Gatt said government incentives for first-home buyers will help to increase activity in the industry during this period of rates transition.

“In theory, increasing interest rates should see a softening of the property market, and at the moment there are a number of reports indicating that new loan application numbers are down as people reassess the market and the impact of pending interest rate rises,” he said.

“This will be offset to some extent though by the various government incentives for first-home buyers to assist them in purchasing property,”

“Many of these schemes will see increased activity in the property market that may see values more stable than they otherwise would have been.”

Opportunity for investors

Compare Club’s Mr Gatt told Australian Property Investor Magazine now could be a good time for investors to buy.

“With vacancy rates at an all-time low, now could be a good time to offset interest rate rises by buying more investment properties that will yield great cash flow,” he said.

“It really pays off to speak to a professional mortgage broker who can help make an assessment of the options in regards to repayments and future lending.”

Mr Gerrard said investors should use this time to review their property portfolio for dead weight.

“Rising interest rates can act as a catalyst for investment property owners to review their portfolio and clear out the duds, and take profits on the diamonds,” he said.

“Properties with high strata or upcoming special levies are offloaded, as well as properties with large capital gains.”

Mr Haeri highlighted opportunities in New South Wales and Victoria.

“For those investors who have the appetite for lower yields, some good opportunities have and will present themselves across NSW and Victoria,” he said.

“Just be mindful that the yields are extremely low and buyers should not expect much growth in the next 12 months.”

“As interest rates start to rise and some markets start to stagnate or correct, investors should look to value-adding strategies to increase equity through their portfolio.”

")