")

")

Report paints bleak picture for housing, affordability and rental market

The National Housing Finance and Investment Corporation’s (NHFIC) third State of the Nation’s Housing 2022–23 report points to a decades-long struggle ahead to provide Australians with enough homes in which to live.

The outlook is bleak for renters and those aspiring to live in an affordable property, with a major new report predicting a housing supply shortfall of more than 106,000 homes over the next five years.

Net additions of apartments and medium-density dwellings, such as townhouses, are projected to be around 57,000 a year over the five years to 2026-27, which is around 40 per cent less than the levels seen in the late 2010s.

The National Housing Finance and Investment Corporation’s (NHFIC) third State of the Nation’s Housing 2022–23 research report said it continues to expect a shortage of apartments and multi-density dwellings for rent over the medium-term.

Critically, NHFIC has also identified that the supply of affordable and social housing is currently short 331,000 houses, with the homelessness housing shortfall sitting at 46,500.

Diminishing supply is coinciding with an increasing rate of new household formation, which is only exacerbating an already chronic rental and housing crisis.

Nathan Dal Bon, CEO, NHFIC, said the rapid return of overseas migration together with a supply pipeline constrained by decade-high construction costs and significant increases in interest rates is worsening an already tight rental market.

“The rapid return of population growth is coinciding with the fastest increases in interest rates for several decades, undermining residential construction feasibilities and weakening the pipeline of new housing,” he said.

Mr Dal Bon added that the opening of Australia’s borders in early 2022 led to a much stronger than anticipated recovery in population growth. The Centre for Population expects net overseas migration to increase by 268,000 between 2022 and 2024, with recent data suggesting this could be considerably higher.

If you’re serious about improving affordability, take GST off new constructed dwellings.

- Steve Douglas, Executive Chairman, SMATS Group

Australians are moving towards a more solitary existence.

The report said that within five years, it is expected lone person households will be the fastest growing household type across the country.

From 2023 to 2032, household formation is expected to be dominated by lone person households (563,600 additional households), followed by couples with children households (533,300 additional households).

More than 1.8 million new households are expected to form across Australia from 2023 to 2033, taking total households to 12.6 million (up from 10.7 million in 2022).

These households are expected to comprise around 1.7 million new occupied households and 116,000 vacant properties (e.g. holiday homes).

“The much earlier than expected increase in interest rates is adversely impacting supply,” Mr Dal Bon said.

“NHFIC expects around 148,500 new dwellings to be delivered in 2022-23, before net new construction falls to 127,500 in 2024-25.

“A recovery in supply is expected after 2025-26 on the back of changing macroeconomic conditions and stronger underlying demand.”

Strong demand for housing coupled with tight supply of both labour and materials, and bad weather has put significant pressure on the construction industry, he said.

Approximately 28,000 dwellings were delayed in 2022. NHFIC’s industry consultation suggests builders are making cost allowances of up to 40 per cent for unexpected delays, up from a more normal 20 per cent.

“In addition to higher interest rates, supply of new housing continues to be impeded by a range of factors including, the availability of serviced land, higher construction costs, ongoing community opposition to development and long lead times for delivering new supply,” the report noted.

Steve Douglas, Executive Chairman, SMATS Group, pointed out that governments on both sides of politics are not addressing supply issues.

“If you’re serious about improving affordability, take GST off new constructed dwellings.

“There’s no need for it to be there because the government makes the money on stamp duty already and with prices now far, far higher than they ever were, they’re making a small fortune – 6 per cent stamp duty, 6 per cent GST, 12 per cent on every transaction is going to the state government.

“Stop it! Take one or the other, increase supply, reduce pressure and allow the population to be housed,” Mr Douglas said.

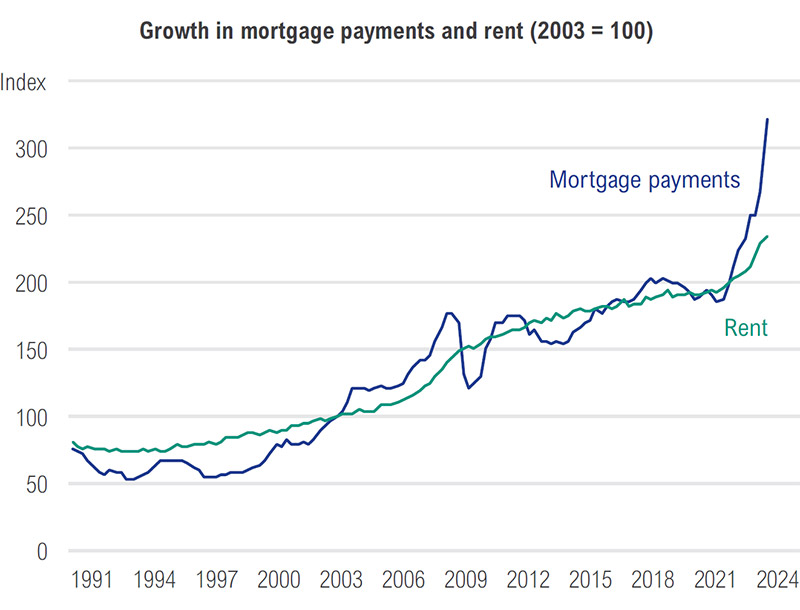

Rental growth and rental affordability varied significantly across and within greater city and regional areas, with rental growth in regional areas now falling after a period of record demand.

Renters have nowhere to turn

Rental growth in major cities such as Sydney and Melbourne are outpacing rental growth in regional New South Wales and Victoria, which suggests the premium of living in large cities close to employment centres may be returning, the report noted.

In Sydney, rents in several outer Local Government Areas (LGAs) increased more than 30 per cent from early-2020 to January 2023 and more than three times that of some inner city LGAs.

Outcomes in Melbourne have been more subdued, with more than half of Melbourne’s LGAs experiencing rental increases of less than 10 per cent since pre-pandemic. Southeast Queensland has had the largest rental rises, with all 12 LGAs experiencing rental increases of 30 per cent or more.

Source: National Housing Finance and Investment Corporation.

For renters try to claw their way onto the property ladder, there’s little respite from the damning statistics.

Analysis shows that since the 1990s in Sydney, deposit hurdle rates (i.e. deposit as a percentage of income) on average increased by around 8 per cent during an interest rate tightening cycle (-10 per cent so far this cycle), compared with 26 per cent during easing cycles. The average deposit required as a percentage of annual income has nearly doubled over this period from 60 per cent to 110 per cent.

More purpose-built accommodation needed

Property Council Chief Executive Mike Zorbas said a like comparison between this year’s NHFIC report and last year’s shows the full projection period gap in the 2022 report (2022 to 2032) was broadly in balance and the full projection period gap in this year’s report (2023 to 2033) is minus 79,300 homes.

“This emerging 79,300 home deficit is a grim warning,” Mr Zorbas said.

“It reminds us that state, territory and local governments simply have to lift their run rates on housing supply across the at-market, key worker and social housing spectrum.

“We also need to urgently move the housing needle by creating the right investment conditions for new build-to-rent housing, purpose-built student accommodation and retirement living communities.

“We need this for our existing population and to continue to attract the skilled migrants and students who support our education sector and bridge the huge gaps in our mining, construction agricultural and retail workforces nationally,” he said.

Mr Zorbas said the analysis also provides more reason to urgently revive and support the passage of the Australian Government's legislative agenda on housing, including the Housing Australian Future Fund and the innovative new National Housing Supply and Affordability Council.

Maxwell Shifman, UDIA’s National President, said the report confirms that the housing market is in steep decline, with the shortfall of 106,300 at-market houses by 2027 as well as the 377,600 shortfall of homeless, affordable and social housing.

“Unfortunately, as NHFIC’s numbers show, we only deliver (net) 2,000 affordable and social houses a year and while the Housing Australia Future Fund will seek to double those numbers over five years, this is a very difficult task that needs the entire housing market, including private sector and Community Housing Providers, working together to solve the issue.

")