")

")

Regional property markets miss out on population boom

Australia's record population growth has been centred on the most populous cities, leaving regional property markets out in the cold.

Australia has experienced record population growth that has helped prop up capital city real estate markets but regional areas are being overlooked and property values underperforming as a result.

Even the impact on capital city prices is being diluted by the fact 20 per cent of new arrivals into the country are taking up existing stock in non-private dwellings, such as student accommodation and worker housing, but prices gains are still outpacing the regions.

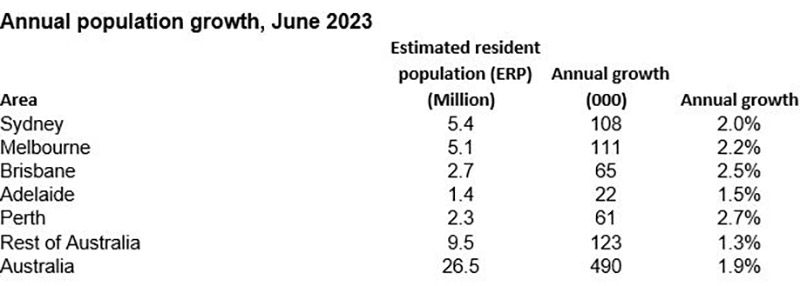

Nearly half a million people were added to Australia’s population in 2022-23, largely from net international migration, but it was the four most populous cities that attracted the newcomers.

Population growth in Perth, Brisbane, Melbourne and Sydney comfortably exceeded that in regional Australia, which recorded its highest level since 2017-18 but still lagged the major cities.

Source: KPMG

Combined with higher interest rates, the impact of this population trend on regional property markets has been pronounced.

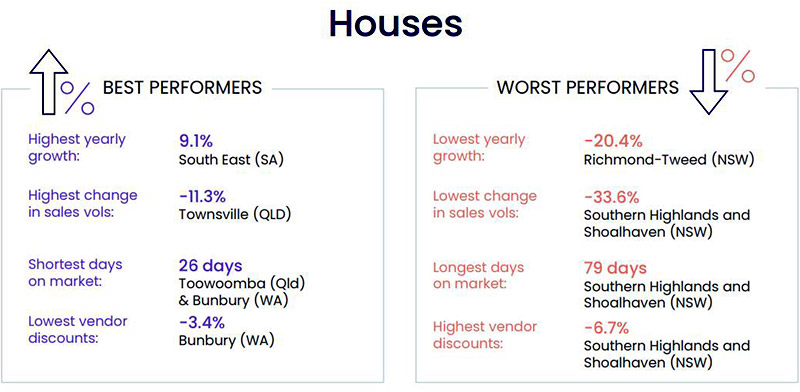

CoreLogic’s quarterly Regional Market Update, which examines Australia’s 25 largest non-capital city regions, shows 18 areas recorded an annual decline in house values over the year to July 2023.

Of the seven markets where values rose, houses in the South East region of South Australia, which includes tourism hotspots Kangaroo Island, the Fleurieu Peninsula and the Limestone Coast, had the largest annual growth for the fourth consecutive report. Values lifted 9.1 per cent in the year to July, a small dip from 10.8 per cent three months ago.

Queensland was a big winner when it came to regional market capital growth, including Central Queensland (2.7 per cent), neighbouring Mackay–Isaac–Whitsunday (1.2 per cent), Toowoomba (0.7 per cent), and Cairns (0.5 per cent), with Bunbury, WA (3.7 per cent) and New England and North West, NSW (1.6 per cent) rounding out the top seven.

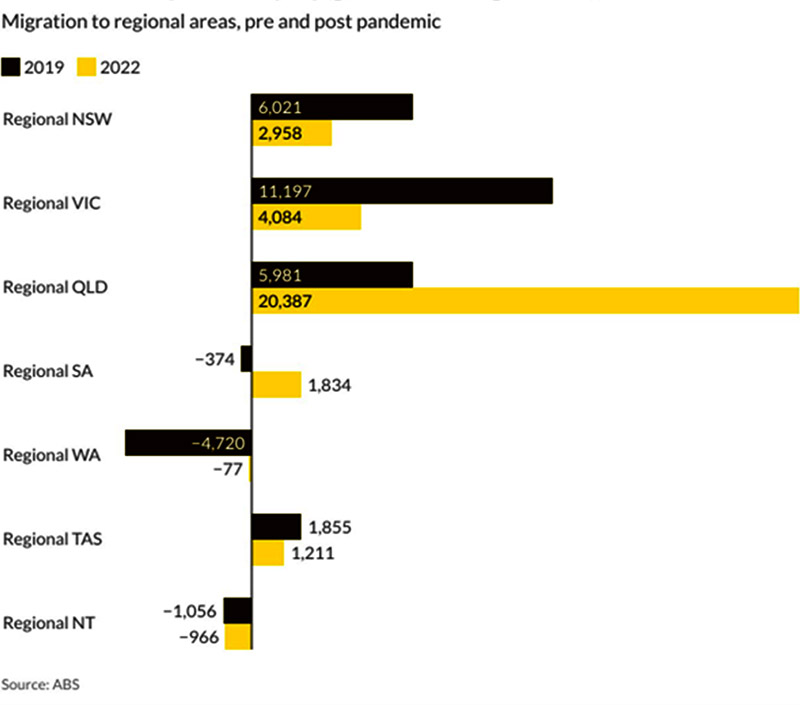

As the following table emphatically highlights, regional Queensland accounts for the vast majority of regional migration nationally.

The weakest conditions over the past year persisted in NSW lifestyle markets Richmond-Tweed (-20.4 per cent) and Southern Highlands and Shoalhaven (-15.0 per cent), although the annual pace of declines is easing. Victoria’s Ballarat (-11.2 per cent) and Geelong (-10.4 per cent) were the only other regions included in the report to record a double-digit decline in house values over the past year.

CoreLogic Australia Head of Research, Eliza Owen, said despite regional Australian dwelling values rising for the past five months, values remain 5.6 per cent below this time last year, and sales volumes are down 21.3 per cent.

“While the market is starting to recover, value growth is largely being led by capital city markets, reflecting milder housing demand across regional Australia as demographic patterns normalise,” Ms Owen said.

Source: CoreLogic

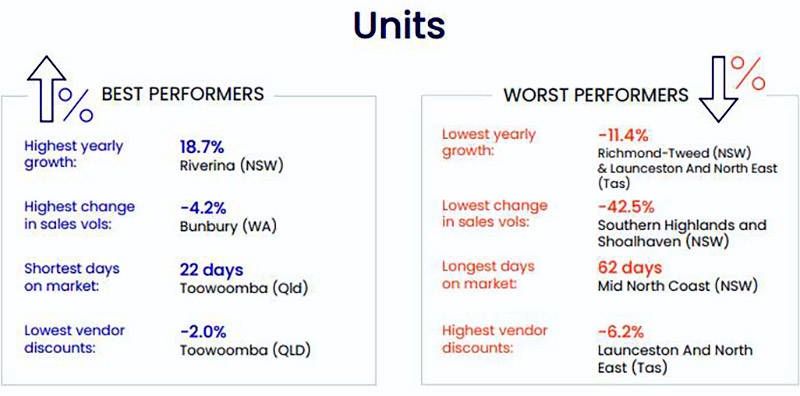

Unit sales volumes declined in all regions over the year to May, with only five of Australia’s regional unit markets recorded positive annual growth in the 12 months to July 2023.

NSW’s Riverina region led the way for the second consecutive quarter. Unit values rose 18.7 per cent, more than double the second and third strongest markets Cairns (9.2 per cent) and Hume, Victoria (9.1 per cent).

At the other end of the scale, Launceston-North East Tasmania, and Richmond-Tweed recorded the equal largest decline in unit values over the past year of 11.4 per cent.

House prices in Richmond-Tweed have fallen by almost 25 per cent in a year but actually edged upwards in two of the past three months, suggesting the worst may be over for this hard-hit market.

Source: CoreLogic

Where are the migrants living?

Overall population growth was driven by Australia’s net international migration, which reached 375,000 thanks to the return of international students and working holidaymakers.

This is more than 50 per cent higher than the year before the pandemic. While the natural population increase (births less deaths) decreased to the lowest level in 20 years.

High international migration was largely possible due to spare capacity in ‘non-private dwellings’, such as student accommodation, and worker housing, which saw a record population increase of 100,000 in 2022-23. The number of people living in ‘non-private dwellings’ has returned to 2018-19 levels of around 864,000 people.

KPMG’s urban economist Terry Rawnsley explains that the spare capacity in ‘non-private dwellings’, particularly empty student accommodation, was pivotal to achieving this record level of population growth.

“While we have seen strong net international migration, the notion that it is all being accommodated in the private housing market is a bit of a misconception.

“It is true that student accommodation has played a major role in the growth of 'non-private dwellings', but we have also observed a rebound in the trend of people shifting into aged care homes which was disrupted during the COVID pandemic.”

“The increases in international student and aged care populations are largely a release of bottle necks caused by Covid, and we are seeing many people moving into existing ‘non-private dwellings’ that had been underutilised during the pandemic.

“Population growth in regional Australia’s ‘non-private dwellings’ was influenced by workers accommodation across the tourism, mining and horticultural sectors,” Mr Rawnsley said.

More broadly, population growth primarily has been focused on major capital cities with 45 per cent occurring in Sydney and Melbourne, while Brisbane and Perth accounted for a further 25 per cent.

")