")

")

RBA lifts interest rates for eighth month in a row

The official cash rate has crashed through the three per cent barrier, with the Reserve Bank of Australia announcing another 0.25 per cent interest rate hike.

The Reserve Bank of Australia (RBA) has used its final policy meeting of the year to deliver an interest rate hike of 0.25 per cent.

Australian mortgage holders have been dealt an eighth consecutive rate increase, taking the official cash rate to 3.10 per cent and adding hundreds of dollars a month to millions of household mortgages.

The decision was widely anticipated but that will offer little solace to hard-hit homeowners.

Aussies with a $500,000 mortgage will be paying almost $900 more per month compared to what they were paying in April and finding an extra $80 above November's monthly repayments.

The rate hike cycle will take a forced break in January, when the RBA Board doesn't meet.

The reprieve may extend into February, with Finder’s RBA Cash Rate Survey showing that less than half (43 per cent) of experts and economists expect another rate rise at the RBA’s first meeting of 2023.

The justification for the latest interest rate increase was simple, according to RBA Governor Philip Lowe.

“Inflation in Australia is too high, at 6.9 per cent,” he said.

He added that global factors explain much of this high inflation, but strong domestic demand relative to the ability of the economy to meet that demand was also playing a role.

“Returning inflation to target requires a more sustainable balance between demand and supply.”

If rates were to steady for a month or two, there was no hint of it happening from Mr Lowe.

“A further increase in inflation is expected over the months ahead, with inflation forecast to peak at around 8 per cent over the year to the December quarter,” he said.

“The Board expects to increase interest rates further over the period ahead but it is not on a pre-set course.

“It is closely monitoring the global economy, household spending and wage and price-setting behaviour.”

Signs point to more rate hikes

The RBA Governor acknowledged that there was a lag from when interest rate increases were implemented to when they took effect in the economy.

There are mixed signals coming from the populace.

On the one hand, new dwelling approvals are trending lower, there’s lower volumes of new mortgage finance being secured, annual sales volumes have trended 13.3 per cent lower compared to this time last year and consumer sentiment through November also dropped a notable 6.9 per cent.

As a result, property prices are still falling.

But counter to all that, markedly higher interest rates are only making a small dent in inflation, which eased slightly below seven per cent, and the Australian Bureau of Statistics (ABS) on Tuesday announced that household spending is still increasing.

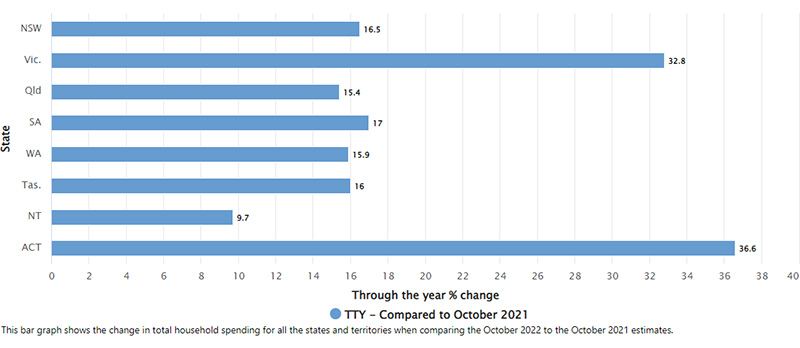

Household Spending By State

Jacqui Vitas, ABS head of macroeconomic statistics, said October 2022 saw the 20th consecutive month of increased through-the-year total household spending, with increases seen in all spending categories.

“The rise was more moderated than previous months, which coincides with less COVID-19 Delta lockdown impacts this time last year,” she said.

Spending in transport (up 42.3 per cent), and hotels, cafes and restaurants (up 39.9 per cent), and clothing and footwear (up 32.2 per cent) all saw strong increases.

Interest rates are (mostly) working

Mortgage distress, softening commodity prices and underperforming wages are likely to prompt the RBA to slow its path towards the 3.2 to 3.85 per cent range many have tipped as the cash rate peak, according to Konark Saxena, Associate Professor in the School of Banking and Finance at UNSW Business School.

Speaking to API Magazine, Mr Konark said the current scenario is much more desirable than what would have happened if interest rates had not been increased.

“In that case, we would have seen much higher household debt, inflation, and more distress down the road.”

He said property price falls were of no concern to the RBA.

“The drop in house prices is one of the intended effects of an increase in interest rates,” Mr Konark said.

“If interest rates were not increasing and house prices were stable, households who are not constrained in terms of borrowing would be taking on more debt, so inflation would be much higher and this would lead to bigger problems later on.

“Increasing interest rates is necessary to curb excessive risk taking when real rates are negative.”

He added that the continually higher levels of spending, which add to inflationary and interest rate pressures, were not necessarily a sign that the RBA’s hikes were ineffective.

I do not think it is a prudent economic policy to artificially keep wages low.

- Konark Saxena, Associate Professor in the School of Banking and Finance, UNSW Business School

“Of course if the increase in interest rates are working, then we should see a drop in consumption and this is not yet evident in the data so it does it seems surprising that consumption is significantly higher than last year, despite the decreases in household housing wealth,” he said.

One explanation may be the low base of last year’s Covid-affected spending habits.

“It is natural that expenditure on travel and entertainment are higher now, compared to artificially low levels last year, and nor does it factor in inflation between the years, so I would not necessarily use this data to suggest interest rate increases are not having the desired effect.”

Households prepared for higher rates

The good news for most households is that they appear to be building their financial buffer in preparation for almost inevitably higher rates in 2023.

Over the past year, households have increased their savings by an estimated 9.87 per cent.

Canstar’s analysis of RBA credit card statistics also showed credit card balances accruing interest in September this year were down 4.96 per cent annually, reaching the lowest level since March 2003.

Canstar’s finance expert, Steve Mickenbecker, said borrowers may have hoped for a little Christmas cheer from the RBA, but have been well-conditioned to expect the inevitability of an increase.

“Australians are not quite battening down the hatches, as retail spending is yet to register a major downturn. But they certainly look to be banking their personal buffer.”

API Magazine's recently released Property Sentiment Report Q3 2022 found that 42 per cent said interest rates would affect their decision to buy in the next 12 months. The exact same proportion said a 1.1 to 2.0 per cent rise would be enough to alter their buying intentions. Another third were more accommodating, with a lift of 2.1 to 3.0 per cent being their tipping point.

A sign that variable rate mortgage holders are feeling the heat is the record numbers resorting to refinancing.

PEXA Chief Economist, Julie Toth, said the largest and fastest rate rise cycle ever implemented by the RBA will continue to take ever larger chunks of disposable income away from mortgage-bearing households into 2023.

““Looking ahead, the RBA continues to flag the possibility of further rate rises in the new year in order to tame excessive domestic demand in our resource-constrained economy.

“We note further rises are not yet a fait accompli, as globally the latest monthly indicators of inflation in the US showed some very welcome hints of levelling out.

“Locally, we are not seeing evidence of a prices-and-wages inflation spiral, which would necessitate further tightening.”

Mr Konark said limited wage growth could still be encouraged without necessarily driving further inflation.

“While stagnant wages make the job of the RBA easier by reducing inflation pressures, I do not think it is a prudent economic policy to artificially keep wages low.

“This will prioritise financial risk taking over building human capital and the efforts of hard-working Australians.

“It will also increase inequalities and distort incentives and is not a good long-term strategy for the Australian economy.

“I think it’s better to allow some wage growth so that young workers, and those that don’t own homes and didn’t share the house price upside of the past decade, don’t have to sacrifice their wages for the sake of the wealthier households of Australia,” he said.

")