")

")

One in three mortgage holders under financial stress

Households across the country are reviewing budgets yet again, with more and more slipping into home loan arrears as the continual cycle of interest rate hikes takes its toll.

Around half of all Australian mortgage holders are under financial strain after the latest hike to the official cash rate that dictates the interest banks charge borrowers.

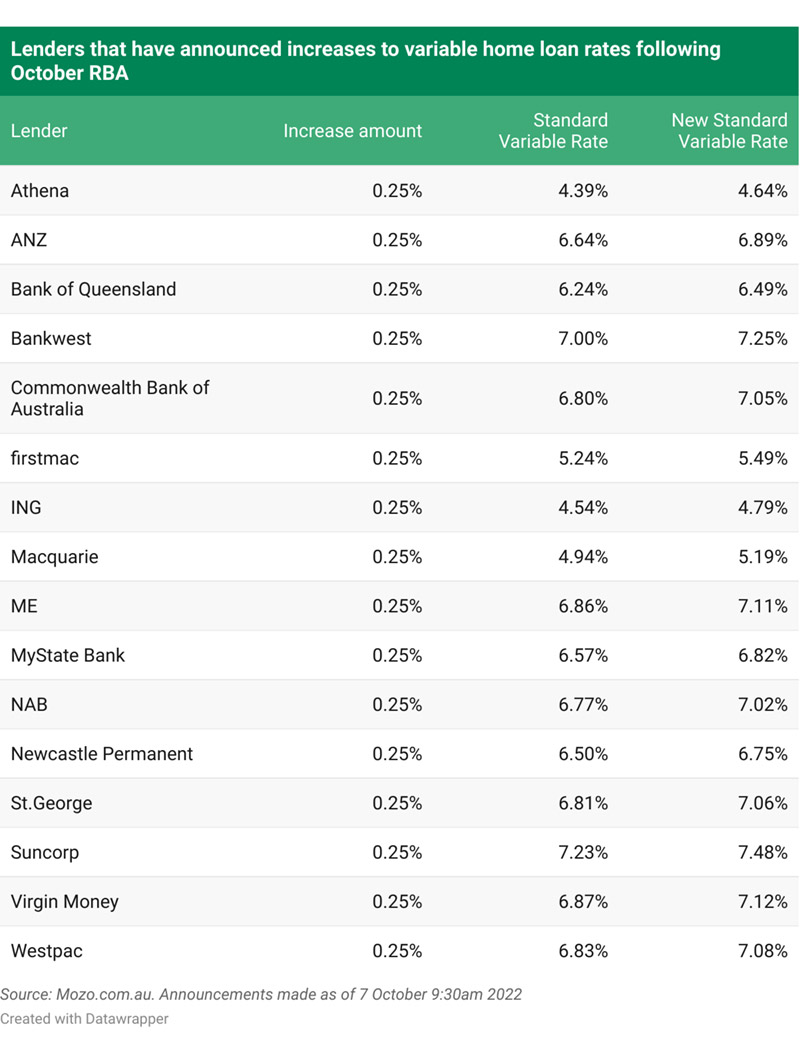

Research released Friday (7 October) by comparison website Mozo showed that almost a third (31 per cent) of borrowers are under financial stress but still able to pay their mortgage.

More disconcertingly, 14 per cent are now in extreme financial stress and unable to meet their repayments.

When another cohort were factored in – the 18 per cent who were in shock when interest rates rose but still able to adjust to the higher repayments by the end of the year – around three in five Australian households were living in a state of financial duress.

Claire Frawley, Mozo’s personal finance expert, said the last six months have hit households hard.

“More than three quarters (78 per cent) of mortgage holders are concerned about rising interest rates,” she said.

“No matter your financial situation, rising interest rates are worrying for most households.”

A third (32 per cent) of homeowners expressed that they would be under serious financial stress if their home loan interest rate was between 5 per cent and 7 per cent.

The average variable interest rate is currently sitting at 5.01 per cent, this is not considering all the lenders that will pass on the 25 basis point increase following the October RBA meeting.

“Those with a variable interest rate of 5.26 per cent will be paying $2,996 a month in repayments for a $500,000 loan.”

How many to go?

Mortgage borrowers should brace for more interest rate hikes, but just how many RBA increases are coming has economists divided.

Three of the big four banks have revised their forecasts, after the lower than expected 0.25 percentage point RBA rate hike on Tuesday.

ANZ now predicts the cash rate will peak at 3.60 per cent in May next year, instead of 3.35 per cent by the end of this year. ANZ noted the RBA’s decision to reduce the pace of the hikes increases the risk that more hikes will be needed in total.

While Westpac still believes the cash rate will hit 3.60 per cent, it has pushed back the peak until March next year.

NAB has kept its 3.10 per cent peak but has pushed it back from November to February 2023.

CBA’s cash rate outlook remains unchanged, forecasting the peak at 2.85 per cent next month.

Sally Tindall, Research Director, RateCity, said there could still potentially be four more standard RBA hikes ahead.

“Make certain you’re ready for these hikes by checking what your monthly repayments will be if your rate rose by another 1 per cent after this hike,” she said.

Australians, however, are doing nothing to convince the RBA that interest rates are biting hard enough to dampen inflation.

They collectively continue to smash the credit card and yet still manage to pay off the debt.

Credit card spending hit a record high, according to data released Friday, while the cumulative debt dropped to an almost two-decade low.

RBA: ‘arrears mounting’

The Reserve Bank of Australia had admitted that housing loan arrears are likely to increase but stuck to its oft-repeated mantra that most households are equipped to handle the increased repayment load.

“There is a small group of borrowers who could fail to meet debt payments due to low savings and high levels of debt,” the RBA’s Financial Stability Review, released Friday, stated.

“Financial stress could be more widespread if economic activity turns out to be much weaker than expected.

“Higher interest rates will increase borrowers’ debt payments.

“Despite a strong labour market, income growth has not kept up with inflation in Australia, leaving households with less capacity to service their debts,” the RBA noted.

It went on to say that many households will be able to manage this debt burden by reducing their spending and/or rate of saving.

“However, a small share of borrowers with lower savings and high debt are vulnerable to payment difficulties and as a result, housing loan arrears rates are likely to increase in the period ahead from currently very low levels.”

Debt-servicing challenges will become more widespread if economic conditions, particularly the level of unemployment, turn out to be worse than expected and housing prices fall sharply, it said.

Total increase to repayments 1 May 2022 to peak on big four bank forecasts

| Loan size | CBA Cash rate 2.85% |

Westpac Cash rate 3.60% |

NAB Cash rate 3.10% |

ANZ Cash rate 3.60% |

|---|---|---|---|---|

| $500,000 | $760 | $983 | $833 | $982 |

| $750,000 | $1,140 | $1,474 | $1,250 | $1,473 |

| $1 million | $1,520 | $1,966 | $1,667 | $1,964 |

Source: RateCity. Calculations are estimates and repayments are for an owner-occupier paying principal and interest over 25 years. Starting rate is the RBA existing variable customer rate of 2.86 per cent in April 2022 and big four bank cash rate forecasts are applied.

Mortgage prison

Falling property prices have the capacity to force some borrowers into ‘mortgage prison’ where they are unable to refinance.

The value of the median-priced house in Sydney could drop by a further $175,087 by the end of next year, down to $1.10 million, based on new property price forecasts from NAB.

RateCity analysis of these forecasts shows the median Sydney house price could fall to $1,108,415 by December 2023. This would be the largest drop across all capital cities in dollar terms.

In Melbourne, the median house price is estimated to fall by $156,367 from now until the end of next year to $780,764.

Borrowers who bought recently with a small deposit could find their equity (the amount of the home they own) falls below 20 per cent and remains there for a number of years, even if they make their standard principal and interest repayments.

This would make it costly to switch banks as they are likely to have to pay lenders mortgage insurance, a cost that can run into the tens of thousands of dollars and could easily negate savings made from refinancing. In some cases, lenders might decide not to take them on at all due to their equity position.

Median house prices - how far could they fall by the end of 2023?

| City | Median house price (today) | Estimated house price (end 2023) | Difference to today $ | Difference to today % |

|---|---|---|---|---|

| Sydney | $1,283,502 | $1,108,415 | -$175,087 | -14% |

| Melbourne | $937,131 | $780,764 | -$156,367 | -17% |

| Brisbane | $841,923 | $733,484 | -$108,439 | -13% |

| Perth | $584,941 | $493,111 | -$91,830 | -16% |

| Adelaide | $704,692 | $583,864 | -$120,828 | -17% |

| Hobart | $761,368 | $604,600 | -$156,767 | -21% |

Source: RateCity. NAB property price forecasts, CoreLogic index-adjusted median values, 31 December 2021 and 31 September 2022. Assumes house prices fall in line with dwelling forecasts.

People most likely to fall in this category are those who borrowed at the peak of house prices in their area, with small deposits such as first home buyers.

RateCity analysis shows if someone bought a median-priced house in Sydney in June 2021 with a 5 per cent deposit, they could owe the bank 5 per cent more than their home is worth by the end of 2023, if NAB property price forecasts are realised (LVR of 105 per cent).

")