")

")

Interest rates hammering home values, loans and budgets

Property prices have been tipped by one major bank to fall by another 11 per cent this year, as interest rate hikes deter prospective buyers and sink home loan lending.

While inflation continues to laugh in the face of higher interest rates, its impact on the housing sector is now undeniable.

New home loan commitments have continued to slide, property prices are falling and expected to drop by another 11 per cent this year, refinancing levels continue to break records and rents are skyrocketing due to a lack of investors and landlords trying to cover higher interest rates.

And, of course, mortgagees are being slammed.

The impact of rising interest rates and higher loan repayments have severely impacted all borrowers, with Canstar’s analysis showing borrowers faced a 42 per cent per cent increase in home loan repayments from May to December, adding $888 to repayments on a $500,000 loan over 30 years, or $1,778 on a $1 million loan.

But not even higher rents and cheaper homes can lure first home buyers, with 4.2 per cent fewer entering the market over the past month and a massive 35.9 per cent less over the year.

The impact of the eight straight Reserve Bank of Australia (RBA) cash rate rises has deterred buyers from jumping into the property market.

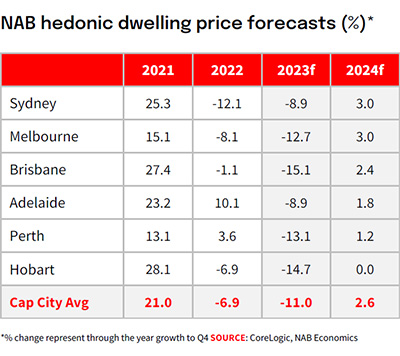

As a result, property prices are falling at their fastest pace on record, albeit from record highs, and the National Australia Bank predicts they’ll tumble another 11 per cent in the next 12 months after falling 7 per cent in the past year.

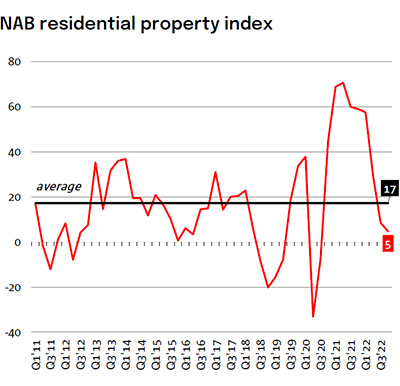

“Overall, this equates to a peak to trough decline of 19 per cent following the peak in prices mid last year,” the NAB residential property survey Q4-2022 noted.

Source: NAB residential property survey Q4-2022

Alan Oster, NAB Group Chief Economist, said they still see the declines as orderly, primarily reflecting reduced borrowing power and affordability constraints rather than an oversupply of housing.

“Indeed, the rebound in population growth alongside a healthy labour market and very tight rental markets are all offsetting factors at present,” he said.

“More broadly, we see the impact of interest rate rises on the rest of the economy becoming more evident in the next six months.

“While spending growth has certainly slowed, the consumer has remained resilient to both higher inflation and interest rates.

“We continue to see the RBA lifting rates at each of the next two meetings, before pausing at 3.6 per cent through the rest of 2023 with some easing in rates likely in 2024.”

Tale of east and west’s property markets

Sydney, Melbourne and Hobart have led the property price declines, likely reflecting greater affordability constraints in these capitals.

Outcomes across the other cities have been mixed, with Brisbane also declining solidly over the past year (with a recent acceleration in falls), but Perth and Adelaide still positive after peaking later and seeing more modest declines. Nonetheless, the impact of higher interest rates is flowing through across all areas, with the recent run of monthly outcomes showing declines across all states.

The NAB Residential Property Index fell for the third straight quarter to end of December.

But tellingly, pessimism about property price performance was largely limited to the eastern states capitals.

Source: NAB residential property survey Q4-2022

Sentiment was negative in Victoria (-6 pts) and New South Wales (-6 pts), where house prices in Melbourne and Sydney fell most steeply over the course of 2022. South Australia (+21 pts) led the way, with positive outcomes also recorded in the Northern Territory (+10 pts), Queensland (+6 pts) and Tasmania (+6 pts). The Western Australia state index was neutral (0).

Confidence levels among surveyed property professionals still point to a relatively slow housing recovery in the next few years, with NAB’s 1-year (+11 pts) and 2-year (+25 pts) confidence measures basically unchanged at well below survey average levels.

Confidence levels in the next 1-2 years are highest in WA and lowest in the Australian Capital Territory.

Property professionals see modest growth in WA (1.3 per cent), the NT (0.4 per cent), Tasmania (0.2 per cent) and SA (0.1 per cent) in the next 12 months, with further falls tipped for Victoria (-4.0 per cent), NSW (-3.3 per cent), Queensland (-2.7 per cent) and the ACT (-2.2 per cent).

Property’s turnaround point looming

Amid the turbulence of the past few years, repeated interest rate rises and cost of living increases, economic confidence is at an all-time low but most commentators expect property prices to stabilise and return to modest growth in 2024, on the condition inflation is finally tamed.

Maree Kilroy, Senior Economist for BIS Oxford Economics, said the pace of price declines is expected to soften further through the first half of 2023, with lower than average new listings playing a key role in stabilising the market.

“Our forecast is for September quarter to represent the bottom for national property prices, with turnover beginning to improve soon after.

“Some cities will recover earlier than others.”

Speaking at a Melbourne event hosted by real estate debt investment platform AltX, social commentator Bernard Salt explained why Australian property owners and investors should feel optimistic about the future of property in Australia.

“The resumption of immigration to pre-pandemic levels will inject a high level of demand into the property market over the next five years, in both owner-occupier and investment sectors,” he said.

“The tight rental market is likely to be bolstered by an anticipated influx of students, especially from China.”

With newly arrived migrants often looking to showcase their success and wealth by buying a home, Mr Salt expects there will be increased demand in the owner-occupier market.

While immigration is one of the main factors to power the rental and owner-occupier markets in the near future, it’s not the only one, according to Mr Salt.

“Middle-aged millennials and retiring baby boomers are also likely to encourage growth in lifestyle properties outside the major cities.

“In the 1950s, the average lifespan was 69 years, and the average retirement age was 65,” he said.

“So, you’d expect to have four years in retirement before you dropped dead, whereas now the average life expectancy is 84, which is almost 20 years in retirement.

Our lifecycle has been reinvented to introduce a lifestyle stage.”

And with a lifestyle stage, he pointed out, comes a demand for lifestyle property.

“We’re about to see five and a half million people pass from the single apartment stage of life into needing a lifestyle house.”

Everybody’s refinancing

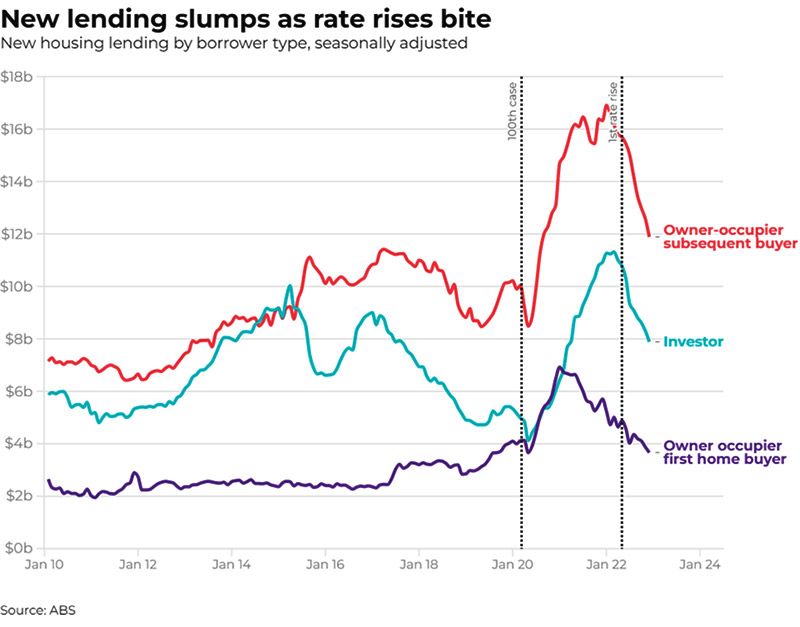

In the interim, huge numbers of borrowers are ditching their bank and refinancing elsewhere.

The value of total housing loan refinancing between lenders fell 1.5 per cent but remained high at $19.1 billion in December 2022, according to data released Friday (3 February) by the Australian Bureau of Statistics (ABS).

“Recent months saw record high refinancing activity for both owner-occupiers and investors. Borrowers continued to switch lenders for lower interest rates as the RBA’s cash rate target rose,” Sean Crick, ABS head of Finance and Wealth, said.

While there is elevated refinancing activity, the value of new lending continues to fall with the housing market downturn ongoing. This is in part driven by fewer home purchases as well as the reduction in borrowing capacities that has accompanied the sharp rise in interest rates.

The total value of new loan commitments for housing fell 4.3 per cent month-on-month in December, to sit 29.3 per cent lower year-on-year, the largest annual decline on record. Though the fall comes off the close to record high levels seen in December 2021.

The value of new lending to owner occupiers was down 4.1 per cent, and to investors it fell 4.4 per cent month-on-month in December.

")