Four easy steps for property investors to manage tax deductions, cash flow

BMT Tax Depreciation outlines how a PAYG withholding variation works, its benefits and how claiming depreciation can further improve cash flow.

Choosing to use a Pay As You Go (PAYG) withholding variation could allow a property investor to routinely increase their cash flow by changing the amount of tax withheld by their employer.

BMT Tax Depreciation outlines how a PAYG withholding variation works, the benefits and how claiming depreciation can further improve cash flow.

What is a PAYG withholding variation and how does it work?

A PAYG withholding variation, previously known as a Section 221YD, enables investors to take advantage of tax deductions regularly by allowing a person to change the amount of tax withheld by their employer.

A downward PAYG withholding variation reduces the amount of PAYG tax withheld as it accounts for additional tax deductions, like tax-deductible expenses and depreciation available from an investment property.

A property investor may do this to get more cash in their pocket regularly, rather than waiting every 12-months for their tax return.

On the other hand, an upward PAYG variation increases the amount of tax paid each pay cycle. This could be an option for property investors who own a positively geared investment property and want to avoid a big tax bill at lodgement time.

The most common PAYG withholding variation is a downward variation.

Four-steps in setting up a PAYG withholding variation

Step 1: Contact an accountant. An accountant will usually organise a PAYG Withholding variation by submitting estimated financial information to the Australian Taxation Office (ATO).

Step 2: Contact a specialist quantity surveyor to order a tax depreciation schedule. This schedule will outline all current and future depreciation deductions for an investment property. The higher the depreciation deductions are, the less tax needs to be taken out from your salary.

Step 3: Once a request has been approved by the ATO, your employer will adjust the amount of tax withheld.

Step 4: Remember, a PAYG withholding variation doesn’t replace your normal tax return. You will still need to visit an accountant at the end of the year to calculate the actual amount of tax.

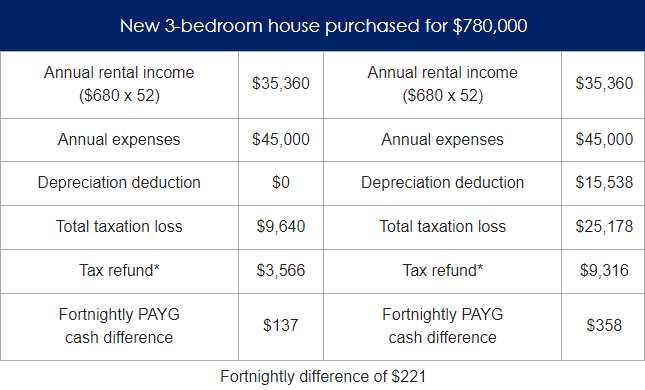

Case study: PAYG withholding variation and depreciation deductions

Joe purchases a brand-new house for $780,000 which is rented out for $680 per week, or $35,360 per annum. Joe has expenses including interest, rates, repairs and maintenance, property management fees and insurance totalling $45,000 per annum.

*Based on a tax rate of 37 per cent.

If Joe doesn’t claim depreciation, he receives an additional $137 per fortnight by applying his PAYG withholding variation. But with a depreciation claim of $15,538, Joe receives $358, an additional $221 in his fortnightly pay.

As we can see, a PAYG withholding variation provides Joe more flexibility by having access to money on a regular basis rather than a lump sum once a year.

Because a PAYG withholding variation provides investors access to money during the year it enables easier management of cash flow, especially in the event of surprise costs such as urgent repairs or maintenance. This additional income also provides the owner the option to invest the extra money or reduce loan liabilities.