")

")

Another big leap takes interest rates to six-year high

The RBA has created history by raising interest rates by 0.5 per cent for the third month in a row, making it four consecutive months of increases.

Interest rates have continued their historic upward trajectory, with the cash rate lifted by another half a percentage point to a six-year high of 1.85 per cent.

It marks the first time the Reserve Bank of Australia (RBA) has lifted interest rates at four consecutive meetings since the introduction of its 2 to 3 per cent inflation target in 1990.

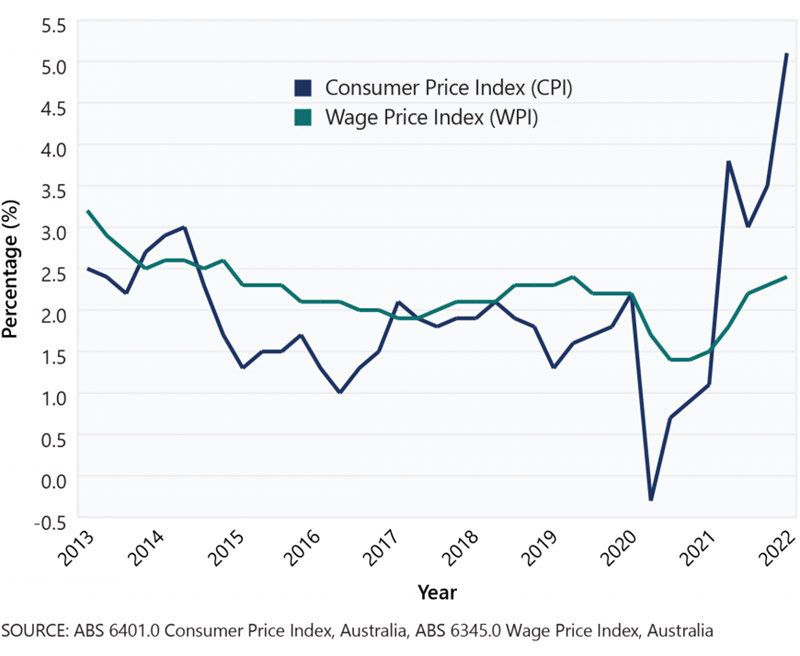

It comes after the latest inflation figures showed Australian prices rose 6.1 per cent in the June quarter - the fastest annual pace in 21 years.

The combined cash rate hikes will cost the average Aussie homeowner an additional $610 per month compared to what they were paying in April. The average home loan in Australia is $611,158.

RBA Governor Philip Lowe made it clear more rate rises were likely but offered no specific clues as to how often or by how much.

“The Board expects to take further steps in the process of normalising monetary conditions over the months ahead, but it is not on a pre-set path.

“The size and timing of future interest rate increases will be guided by the incoming data and the Board's assessment of the outlook for inflation and the labour market.

“The Board is committed to doing what is necessary to ensure that inflation in Australia returns to target over time.”

Pain aplenty

Graham Cooke, head of consumer research at Finder said rising interest rates, soaring inflation, energy prices and the general cost of living are already squeezing household budgets.

“This latest hike could cost the average mortgage holder a whopping $7,300 extra per year compared to what they were paying in April.

“With almost a quarter of Australian homeowners already struggling to pay their mortgage in July, this news will be especially painful,” Cooke said.

Almost 1 in 5 Australian mortgage holders (18%) have refinanced their home loan in the past six months, according to a Finder survey of homeowners in July 2022.

The same proportion (18%) say they plan to do so in the coming six months.

Even as the RBA hikes rates rapidly, inflation soared and wages remained stubbornly flat, household spending in May still increased 7.9 per cent compared to 2021.

Despite this, three out of four experts believe the recent cash rate hikes will be enough to rein in household spending and decrease inflation.

Leanne Pilkington of Laing+Simmons said the measures were already impacting sentiment.

“Rate hikes are dampening the property market, and it’s reasonable to believe increased mortgage repayments for a large number of Australians will affect spending over time, with a reduction in spending already being seen,” Pilkington said.

Malcolm Wood of stockbrokers Ord Minnett noted, “Rate rises will absorb the elevated saving rate, reverse the wealth effect (lower home prices) and cap the amount of excess saving spent.”

The amount the average Australian has stashed in savings is creeping up, according to Finder’s Consumer Sentiment tracker.

In June and July, the average Aussie had $36,446 tucked away. That’s compared to $25,381 in January and February this year.

Economy responding

Property prices are continuing to fall, with CoreLogic’s measure of values showing a 1.3 per cent decline in July. It was the third successive monthly fall, coinciding with the RBA’s increase in interest rates.

There are also indications the lift in rates is starting to have an impact outside the housing market.

Measures for production, employment and supplier deliveries all edged down last month. There are also signs of softness in manufacturing, with the Australian Industry Group’s performance index for the sector falling by 1.5 points in July.

The RBA’s August Monetary Policy Decision released on Tuesday (2 August) identified its biggest unknown in terms of managing inflation and thereby interest rates.

“A key source of uncertainty continues to be the behaviour of household spending,” the RBA noted.

The balancing act it had to control was the pressure on household budgets up against the economic power of record low unemployment.

“Higher inflation and higher interest rates are putting pressure on household budgets, consumer confidence has also fallen and housing prices are declining in some markets after the large increases in recent years.

“Working in the other direction, people are finding jobs and obtaining more hours of work.

“Many households have also built up large financial buffers and the saving rate remains higher than it was before the pandemic.

“The Board will be paying close attention to how these various factors balance out as it assesses the appropriate setting of monetary policy.”

The cash rate remains well below the pre-covid decade average of 2.56 per cent.

RBA under microscope

As the RBA hikes rates at eye-watering speed to control rampant inflation, there’s been no shortage of critics piling on to criticise their tactics and timing.

Former Labor Senator Stephen Conroy said Reserve Bank Governor Philip Lowe got the interest rate forecasts “dramatically wrong” the past few years.

He said what’s concerning is Mr Lowe is “getting it wrong again”.

“He is absolutely pulling the wrong lever and refusing to explain how he’s going to deal with the actual problem,” Mr Conroy told media.

Mr Lowe’s main misstep was to promise that interest rates wouldn’t rise until 2024, which was deemed misleading for borrowers.

Warren Hogan, chief economist at both ANZ and Credit Suisse, told media the RBA was guilty of some “pretty bad errors” in recent months.

“Australia’s central bank had taken on risky strategies, including spending lots on insurance and sinking funds into a bonds program that had not paid off.”

Mr Hogan, who was also the former principal adviser to federal treasury, said: “It’s unforgivable. I think they should resign – the whole board.”

“Mr Lowe should have the character to stand down,” Mr Hogan added.

Treasurer Jim Chalmers recently announced that the RBA will be subjected to a wide-ranging review looking into its core operations and culture, the first such independent review since 1981.

")