At the midway point, are we climbing or falling from the mortgage cliff?

With the mortgage cliff around the halfway point of its gradual transition from low fixed to high variable rate loans, is a looming disaster unfolding or are borrowers proving to be more resilient than expected?

It’s late August and the midway point of what was dubbed the mortgage cliff.

This so-called cliff was named to denote the lemming-like fate that supposedly awaited all who had to move from super low fixed term loans secured from mid-2020 to mid-2022 to loans up to triple that interest rate.

While its progression is far from complete, and much of the impact of this mass switch may still be yet to play out in full, the doomsday scenarios have not eventuated at this stage at least.

There has been a slowdown in economic activity and housing market momentum in response to higher rates across all mortgage holders, while CoreLogic has recorded an unusual increase in new listings over the past few weeks.

But overall, the risk of arrears and default remains contained within Australia’s large mortgage market and a level of resilience demonstrated amid tight labour market conditions.

Property prices have remained resilient for most of 2023 but buyers and sellers alike are eyeing off a crucial spring selling season.

While homeowners are, in broad statistical terms at least, not selling up en masse, they are taking steps beyond trimming the socialising budget to meet these new, sometimes dramatically higher, repayment levels.

The mortgage cliff was all media hype.

- Helen Avis, Director of Finance, Specialist Mortgage

The number of Aussie home loan holders refinancing soared 13.8 per cent in the financial year just completed, while those signing new mortgages fell 20.6 per cent, new research from PEXA shows.

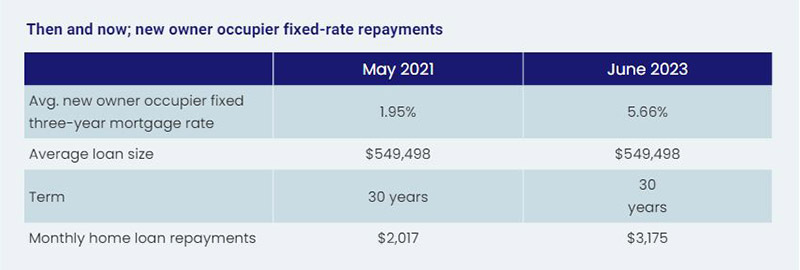

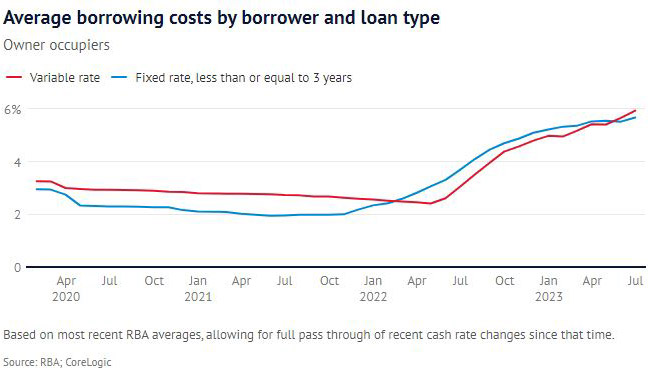

That comes as mortgage holders contend with a transition from interest rates on a loan of around 1.9 to 2.5 per cent leaping to between 6 and 7 per cent.

In terms of what that means to a household’s budget, the repayment on a $750,000 mortgage set at 2 per cent would soar from $3,180 a month to $4,830 a month – an increase of more than 50 per cent overnight, assuming a new rate of 6 per cent.

Yet it seems official data on mortgage stress has not seen a blow out in arrears amid the expiry of low fixed-term loans.

Portion of outstanding loans in arrears

Eliza Owen, Head of Residential Research Australia, said as home values rise, the risk of default also remains low.

“As what is likely to be the last of the RBA’s rate hikes is passed through to households with a mortgage, there may be a mild deterioration in housing market conditions if new listings decisions continue to rise.

“The good news for mortgage holders is that this period of economic slowdown will also take the RBA closer to its long-term inflation target, which could be the impetus for a reduction in the cash rate in the second half of 2024, as predicted by most major banks.”

Whether there is another 0.25 per cent increase in the official cash rate by the RBA is an even money bet. But the governor, Philip Lowe, used the just-released RBA Board Minutes for August to acknowledge the mortgage cliff was a consideration in their decision-making process around interest rates.

“Members noted that banks had continued passing increases in the cash rate through to their customers, and that outstanding mortgage rates and scheduled mortgage payments were set to increase further as a high share of fixed-rate loans roll onto higher rates through the rest of 2023.

“Scheduled mortgage payments as a share of household disposable income increased to 9.4 per cent in the June quarter, around its historical peak.

“Voluntary principal payments into borrowers’ offset and redraw accounts declined in the June quarter (while) net flows into these accounts had declined to be noticeably lower than the pre-pandemic average, consistent with pressures on disposable incomes.”

To be more concise, borrowers are hurting.

Finding more than $1,000 a month for mortgage repayments isn't easy for everyone.

Climbing or falling from the mortgage cliff?

Industry sources are divided on just how severe the implications of the mortgage cliff’s continued unfolding will become. Some argued it was driven by an excitable media while others declare it’s downward spiral with no imminent escape route.

In the former camp, Helen Avis, Director of Finance at Specialist Mortgage, said “the mortgage cliff was all media hype.”

“I cannot see rates rising too much further, and if that is the case then we should not see much more of an adjustment from where we are at now.

“I am not surprised with the lack of delinquencies, with the still relatively strong property market and borrowers able to handle the increases.

“That said some borrowers have been affected and are struggling but the vast majority seem to be coping.

“I know some first home owners who have rented their property and gone back to live with parents, capitalising on the acutely tight rental market to offset the stress of higher mortgage repayments.”

Joe White, President, Real Estate Institute of Western Australia (REIWA), said we are well into 2023 and we have not seen the apocalypse we were told was coming.

“While there have been constant predictions of a flood of forced sales, REIWA data does not yet show an increase in properties advertised as mortgagee sales or mortgagee in possession.

“There is no denying 12 interest rate increases have had an impact on households, but it is disingenuous to underestimate a homeowner’s capacity and willingness to adjust their spending habits.

“Many homeowners on fixed rate loans have prepared for the dreaded mortgage cliff.

“They have paid extra onto their mortgage to be ahead with their repayments, have created a savings buffer or have refinanced.”

API Magazine’s recently released Property Sentiment Report found that the percentage of respondents defining their situation as being in mortgage or rental stress was easing.

While still disturbingly high at 36 per cent, it was an improvement on the 43 per cent of the previous quarter. Disconcertingly, 79 per cent said their financial stress status had eventuated over the past 12 months.

Mark Bouris, Executive Chairman, Yellow Brick Home Loans, however, was far less optimistic than others, reporting that the consequences of the interest rate hikes won’t be fully laid to bear until Christmas this year, as more and more home loans move from cheap fixed rates to high variable rates.

“Expect families to be forced to sell their homes, many to property investors and foreign buyers, and end up in the already-crowded rental market that is driving up inflation.

“Otherwise, families will be forced to cut back their spending on everything from holidays to food to recreational activities and school fees – the list goes on.

“This will hurt the small businesses that rely on consumer spending to pay their bills, which are also rising.

“It’s a vicious cycle, and there’s no clear way out.”

Investors selling rental properties

One portion of the market that is voting with their feet is property investors.

There has been a sharp spike in landlord exits from the property market across Australia.

Victoria is the worst-hit state, with the latest PropTrack figures revealing 30.1 per cent of sales were properties that had been listed for rent since they were purchased.

That’s up from 24.7 per cent in July 2022, and 16.9 per cent in July 2019, before the pandemic. New South Wales followed at 28 per cent, which like Victoria, was also the state’s highest share of investment home sales since late 2018. Queensland was third with 27.15 per cent of sales in July being rental properties.

Regardless of which side of the fence you sit on in terms of the mortgage cliff’s ultimate impact, the rest of the year promises to offer compelling viewing of the economy, housing market, and the financial viability of renters, home owners and investors alike.