Shock as inflation hits highest level since 1990

A February interest rate rise now appears a near-certainty after the latest inflation figure came in well above expectations.

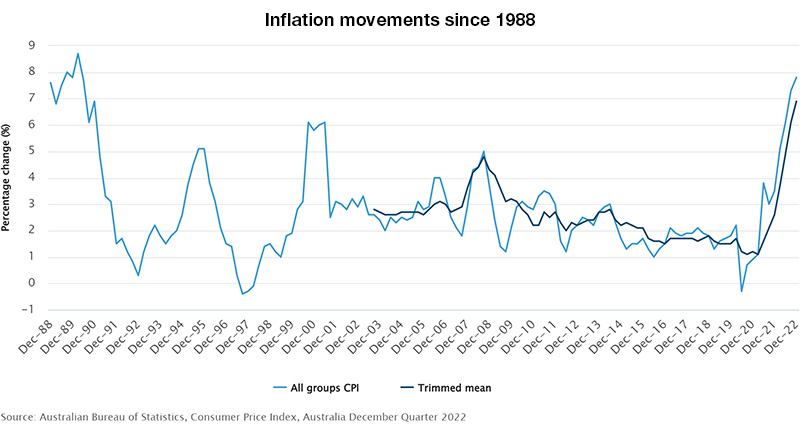

In 1990, the last time inflation was at the levels it has hit today, Australians were watching Graham Kennedy's Funniest Home Video Show, playing with Nintendo Gameboys, in love with Prime Minister Bob Hawke and listening to Milli Vanilli.

A 7 February interest rate hike now appears a near-certainty following the announcement that inflation had leapt a massive 1.9 per cent in the December quarter to hit 7.8 per cent over year.

Michelle Marquardt, Australian Bureau of Statistics’ head of prices statistics, on Tuesday (25 January) said, “This is the fourth consecutive quarter to show a rise greater than any seen since the introduction of the Goods and Services Tax (GST) in 2000.”

The main catalysts over the quarter were domestic holiday travel and accommodation (+13.3 per cent), electricity (+8.6 per cent), and international holiday travel and accommodation (+7.6 per cent).

Growth in prices for new dwelling purchases by owner occupiers (+1.7 per cent) slowed relative to recent quarters (+3.7 per cent in September and +5.6 per cent in June) but remained stronger than historic norms.

Annually, the CPI rose 7.8 per cent, with new dwellings (+17.8 per cent), domestic holiday travel and accommodation (+19.8 per cent) and automotive fuel (+13.2 per cent) the most significant contributors.

The annual change is higher than the government expected, but lower than the Reserve Bank’s upper forecast of 8 per cent. The Treasury forecast in the October budget predicted inflation would rise to a peak of about 7.75 per cent for the December quarter.

Underlying inflation, which excludes one-off price impacts, also rose in the December quarter, up by 1.7 per cent to reach an annual rate of 6.9 per cent, which is the highest level since the ABS first published underlying inflation in 2003.

The Reserve Bank of Australia’s board will be standing like meerkats surveying the savannah as they try to protect the economy from the inflation predator.

Canstar’s Editor-at-Large and money expert, Effie Zahos, Consumers will continue to feel price pressure on key household bills for at least the first half of this year.

“The December inflation numbers all but confirm another ‘business as usual’ interest rate hike of 0.25 percentage points in February as the RBA continues to grapple to bring inflation into line.

“Borrowers need to be prepared to juggle this alongside other price rises.”

RateCity.com.au research director, Sally Tindall, agreed that Australians are now looking down the barrel of the ninth rate hike since May of last year.

“Australia has a serious inflation problem and it’s not going away without a fight.”

“The RBA has little choice but to serve Australians with yet another cash rate hike,” she said.

“After a break in January, the RBA is unlikely to leave the cash rate on hold for two months in a row.”

“Australians are now looking down the barrel of the ninth rate hike since May of last year.

The market odds for another official interest rate rise next month jumped from around 55 per cent immediately before the data release to more than 75 per cent shortly after, according to Refinitiv data.

Supporting the view of the one quarter minority was Hayden Groves, President, Real Estate Institute of Australia.

“With the CPI having peaked within forecasts it is time for the RBA to listen to the chorus of economists calling for a pause on interest rate hikes at its February meeting and assess the lagged impact that past increases have had and not run the risk of grinding the economy to a standstill,” Mr Groves said.

“(The latest inflation figure) is in line with the Budget forecast of 7.75 per cent and just below the RBA’s forecast of 8.0 per cent and points to a slowing down in the rate of increase.”

Pressure on property prices

The extent to which inflation slows down in 2023 will determine whether the RBA needs to keep tightening, or can hit pause on rate hikes.

Head of Research at CoreLogic, Eliza Owen, said the inflation outlook remains important to the housing outlook.

“In the year ahead, inflation may be subject to the competing forces of falling global demand, but rising demand from China as the country moves away from zero Covid.

“The potential for extreme weather events should also be kept in mind, as this can impact production capacity, and lead to inflation spikes.”

Ms Owen added that interest rate hikes in February and possibly March would likely mean further falls in housing demand and values in the months ahead.

Eliza Owen, Head of Research, CoreLogic

“However, with inflation potentially moving through a peak, we are likely to see interest rates peak lower than some forecasters were expecting last year.

“Once interest rates stabilise, we would expect consumer sentiment to improve alongside a gradual stabilisation in housing prices.”

The HIA New Home Sales report, a monthly survey of the largest volume home builders in the five largest states, shows sales of new homes continues to decline sharply following the fastest increase in the cash rate in a generation.

Sales of new homes fell by 4.6 per cent in December leaving sales in the final quarter of 2022 a remarkable 42.0 per cent lower than at the same time in 2021.

Housing Industry Association (HIA) Chief Economist, Tim Reardon, said this slowing in sales will flow though to a slowdown in building activity in the second half of 2023.

“When this hiking cycle began, there was a significant pipeline of home building work under construction, and many more projects yet to even begin construction. This has created a significant lag in the RBA’s impact on employment across the economy.

“The rise in the cash rate has also seen many recent buyers of new homes unable to finance their new project.

“This resulted in one in five recent new home buyers having to cancel their new home building contract as their access to finance was reduced by the rise in the cash rate.

“With one in five customers cancelling their new home building project each month, the pipeline of building work will be eroded quickly.

“Once this pipeline of new home construction work is exhausted, the full impact of the RBA’s rate increases will become apparent. This is expected to occur in the second half of 2023,” Mr Reardon said.

Housing market downturn slowing

Domain’s House Price Report for the December quarter reveals that Australia’s housing market downturn has lost its momentum. Combined capital house prices have declined six times slower and unit prices three times slower than the previous September quarter.

Dr Nicola Powell, Domain Chief of Research and Economics, said sellers had been sitting on the sidelines to see how the housing market downturn unravelled and how high inflation and interest rates would land.

“The data suggests the peak rate of the quarterly decline has passed, as buyers have had time to adjust to the new norm of rising debt cost and reduced borrowing capacity,” she said.

Those with a $1 million mortgage are now paying almost $1,800 more on their loan than this time last year.

Lending indicator data released this month by the ABS shows a whopping $19.5 billion worth of mortgages were refinanced in November, the highest monthly amount in Australian history.

Property in bigger cities faring worst

Sydney led the nation’s loss of downturn momentum with house prices falling three times slower than the previous quarter. Despite an easing rate of decline, house prices have still fallen by about $181,000 below the March 2022 peak producing the steepest annual decline in prices in the city’s history.

Unit prices continued to fall over the December quarter by about $52,000 from the peak, according to Domain.

Melbourne’s housing market downturn lost significant momentum as prices stabilised. Over the last three months, Melbourne’s house prices have nudged slightly higher over the December quarter up by 0.7 per cent. However, despite this marginal improvement, house prices still experienced the steepest fall in three-and-a-half years with house prices now 5.6 per cent below the December 2021 peak, down by about $61,000 and back to mid-2021 pricing.

Unit prices recorded a marginal loss with prices now down by about $35,000 from its peak.

Brisbane and Canberra continue to slide quickly, with house prices now 6.6% below the June 2022 peak in the former and 6.7 per cent lower in the latter.

Further east, it’s a different story.

Perth and Adelaide smashed new records for house prices, while Darwin rebounded. Hobart’s market stabilised.