")

")

Political parties ignoring elephant in the unaffordable room

Both major parties have made major policy announcements around housing and affordability but neither has addressed what most industry experts regard as the biggest issue of all.

In the week leading up to the federal election, the Liberal Party has announced two more policies around housing and superannuation.

The first was lowering the age threshold for those who could access downsizing contributions to superannuation. The second was branded the Super Home Buyer Scheme, which would allow Australians to borrow up to 40 per cent of superannuation to purchase their first home (capped at up to $50,000).

The policies have met with qualified support from many industry stakeholders, most of whom welcomed the addition of another demand-driven initiative.

But whether referring to the coalition’s latest policies or Labor’s home shared equity scheme, the property industry has been united in bemoaning the lack of attention being paid to the elephant in the unaffordable room.

Supply of housing remains largely unaddressed.

The Government’s own official forecasts predict that housing supply is set to drop by around 35 per cent right at the time population growth is resuming, with the National Housing Finance and Investment Corporation forecasting that by 2032 Australia will be 163,400 homes short of demand.

While the Government’s first announcement is an extension of the downsizer scheme introduced in 2017-18, the second is another attempt at helping first-home buyers enter the property market.

It allows first-home buyers to invest up to 40 per cent of their superannuation, up to a maximum of $50,000, to help with the purchase of their first home. The scheme will apply to both new and existing homes with the invested amount to be returned to their superannuation fund when the house is sold, including a share of any capital gain. The money taken out of the super fund to buy the house will be put back into people’s superannuation funds should the house be sold, including a share of any capital gain.

The Coalition says this will protect people’s long-term savings ahead of their retirement.

Labor has promised to cover 30-40 per cent of the cost of a property while retaining that same stake in the asset. When a property was sold, the government would also claim its portion of whatever capital gains were achieved.

But there are fears both parties are only fuelling house price increases while offering temporary or limited respite to a long-term issue, without addressing the lack of supply that is at the core of the affordability issue.

Scott Morrison on Monday (16 May) said his policy would help first homebuyers “get off the sidelines where they see house prices go up” but would not hurt their super balances because the investment in the home would go back in after it was sold.

But the Coalition’s superannuation minister, Jane Hume, admitted there would likely be “a bump in house prices” in the short term, as “a lot of people bring forward their decision to buy a house”.

Ray White Chief Economist Nerida Conisbee was critical of both parties’ policies.

“Giving first home buyers more money than they otherwise would have means that prices will rise,” she said.

“A similar scheme in the UK to Labor’s “shared equity” proposal led to a six per cent increase in prices there and it is likely similar increases would be seen from either the Labor or Liberal proposals.”

She said using superannuation for buying owner-occupier housing should not be encouraged.

“The family home is not an asset that can be easily cashed in at retirement.

“Often the equity in the home is used to move into more appropriate accommodation, such as retirement homes or aged care facilities.

“Using superannuation from early on in a person’s lifecycle for a home can also lead to far less at retirement, particularly if the family home can’t be easily sold to downsize or does not increase in value as hoped,” Ms Conisbee said.

Super demand

Eliza Owen, CoreLogic’s Head of Research, said the provision within the Liberal’s policy that any funds taken from superannuation, along with proportional capital gains, must repatriated to the superannuation fund at the time of selling the property would help safeguard the primary aim of superannuation: saving for retirement.

“However, there are some downsides with relation to stimulating more housing demand and creating inequities with regards to accessing home ownership for lower income households who may not have accrued a sizeable level of superannuation savings.

“Allowing first-home buyers to access superannuation for their upfront housing costs on a broad basis will add to demand and this could increase the cost of housing.

“This may be good news for homeowners looking to protect their wealth, or sellers in an environment where housing market conditions are starting to soften, but for first-home buyers it could erode some of the benefit of dipping into their super.

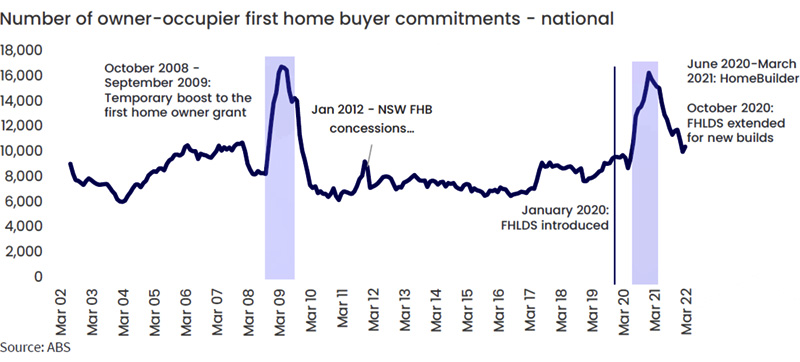

"Historically, first-home buyer activity has been elevated when first-home buyer schemes are enacted.

“Admittedly the effect seems most concentrated when the schemes are temporary, and interest rates are low,” Ms Owen said.

She said temporary, demand-side first homebuyer incentives coincided with a surge in demand, as the table below highlights.

All demand, no supply

Since mid-2019, the average loan for a first-time buyer in both NSW and Victoria has climbed by $100,000 to almost $600,000 in NSW and just above $500,000 in Victoria.

Supply of new dwellings dropped 36 per cent in the last 12 months and interest rates are on the rise.

The introduction of a range of demand-driven policies has done nothing to improve affordability. Despite the first home loan deposit scheme, the new home guarantee, the family home guarantee, the first home super saver scheme, and the HomeBuilder grant, the median price for a house is $1.4 million in Sydney and $1 million in Melbourne.

The Property Council said it welcomed both parties’ targeted and responsible demand-side policies that help first time homebuyers bridge the deposit gap and yet a proper national focus on housing supply was still needed.

“The need remains for broader action on supply so that older Australians who do right-size, have an appropriate supply of townhouses, apartments and importantly retirement living options,” a statement read.

Executive Director of Retirement Living at the Property Council of Australia Ben Myers said the Liberal’s announcement was an important step in encouraging older Australians to find a home that suits them better, while freeing up housing supply for younger, growing families.

But the neglect of any attention on property supply was again at the forefront.

“Incentivising older Australians to unlock their home equity and right-size into more suitable housing options, especially purpose-built age-friendly communities, is a wise move by government,” Mr Myers said.

“We know many older Australians face barriers to right-sizing their housing and today’s announcement will provide real incentives to encourage people to unlock their home equity and move into a home that supports them to live independently for longer.

It's now 10 times easier for Scott Morrison or Anthony Albanese to become prime minister of Australia than an average Australian of securing a rental property.

- Kevin Young, founder of the Australia-wide Property Club

Mr Myers said there was still a need for broader action on housing supply, especially to encourage the supply of purpose-built age-friendly communities, to ensure Australians have affordable and accessible choices.

“Unless Australia is able to better provide the housing supply and choice that our ageing population needs, affordability and accessibility will be an increasingly dire social and economic issue,” he said.

Kevin Young, founder of the national Property Club, said the election represented Australia’s last chance to fix property mistakes from the past.

He said Government charges such as the GST, stamp duty, headworks, and infrastructure costs account for around 50 per cent of the cost of buying property in Australia.

“Those costs are being passed on to first-home buyers and others and it has locked them out of the market.”

He said both major political parties in the Federal election had ignored the rental crisis that has resulted in rents surging by more than 15 per cent during the past year in capital cities and regional throughout Australia.

It was now at least 10 times easier for Scott Morrison or Anthony Albanese to become prime minister of Australia than an average Australian of securing a rental property, he added.

“Property Club has on average 40 applications for every property that is advertised for rent.

“Tenants therefore have a one in 40 chance of securing a property, which compares to the latest betting odds of one in four for Scott Morrison to become PM and one in 1.25 for Anthony Albanese,” he said.

The Urban Development Institute of Australia was another to welcome both parties’ initiatives but rebuked them for overlooking the supply issue.

Max Shifman, UDIA National President, said the Liberal’s superannuation plan could mean the difference between getting into a home sooner or, for some Australians, spending more time in an uncertain rental market.

But he was quick to add that more properties were desperately needed.

“UDIA National State of the Land research indicates that new housing supply will slump as much as 43 per cent in the coming year from a lack of land supply.

“With costs and prices exacerbated by continued shortages of materials and labour, we need policies that assist with capacity and demand to be linked with those that support more of the right housing being built,” Mr Shifman said.

“Federal political leadership should incentivise states and territories to boost development ready land, fast-track enabling infrastructure and streamline planning and approvals to maximise housing affordability.

“This includes complementary initiatives that incentivise state and territory governments to increase stamp duty thresholds, so selling a house is not penalised by high transaction costs,” he added.

")