Property Sentiment

Report

Q2 2023

Data collected between

26/06/23 and 17/07/23

from 735 respondents.

Key findings

1. Size matters once again

Property buyers have decided that, once again, size matters.

The relative success in terms of houses delivering more capital growth than units has seen them emerge strongly in the past quarter as the favoured property acquisition target of our respondents.

Houses are now the preferred intended purchase over the next 12 months among 37 per cent of respondents, a seismic shift from the mere 21 per cent with that intention just three months ago.

While units have shown recent signs of capital growth, the rate of loss-making sales over the past three months was most concerning in the unit market and is likely weighing on the minds of property buyers.

While our survey of 735 readers showed a small decline (23 to 19 per cent) in the proportion of owner occupiers and investors intending to buy, there was a marked decline in the interest levels of developers who, deterred by building sector cost woes, have declined from 16.5 per cent to just 9 per cent of those planning to procure a property.

It wasn’t until March 2023, at the conclusion of our Q1 survey reporting period, that units enjoyed their first monthly price increase in 11 months.

Units are becoming more attractive as buyers make compromises over space for location in the face of rising interest rates but as rates near their perceived peak, our respondents are sending a signal that space may be making a comeback.

2. Onlookers are keeping their ammunition dry

In asking survey respondents about what property transactions they had made in the last year, activity in the residential market was largely unchanged from the previous quarter, while commercial sellers (5 per cent) were sitting in the sidelines compared to last quarter, when 10 per cent had sold a property.

Our respondents of Q2 2023 have been the most inactive since our surveys began, in a clear sign that economic turbulence and market uncertainty has kept so many on the sidelines. The proportion of people saying they’d made no property moves in the past year soared from 13 per cent to a remarkable 30 per cent in just three months.

Those who invest did so with fervour. Of the 70 per cent of respondents who transacted on property in the past 12 months, 63 per cent of those did so on more than one property.

Intentions don’t always equate to action, but more people seem intent on transacting in property in the coming 12 months. Yet, that reticence seen in the past year is still evident, with almost three times as many respondents as the previous quarter saying they plan to sit on their hands when it comes to property. The last survey saw just 3 per cent of people saying they had no property activity planned, compared to a sizeable 8 per cent this time around.

While there are signs of the property market recovering its losses of the past year or two and inflation and interest rates are gradually coming to heel, property remains a wait and see proposition for many – whether buying or selling.

3. Interest rate worries not abating

By the midway mark of 2023 borrowers’ heads were collectively bowed, weighed down by the burden of 12 rate rises in almost as many months. By that stage, $15,168 had been added to the average Aussie mortgage since rates were last at 0.10 per cent in April 2022.

So it’s little surprise that interest rates remain, together with the associated difficulties caused by a lack of finance availability, the biggest concerns confronting survey respondents. The two factors combined were equally prominent as the driving influences behind almost a quarter of respondents’ property decision-making for the coming 12 months.

Those figures are similar to the corresponding survey at the midway point of 2022 but interest rates are steadily growing in influence in determining how people will shape their investment decision-making in the year ahead.

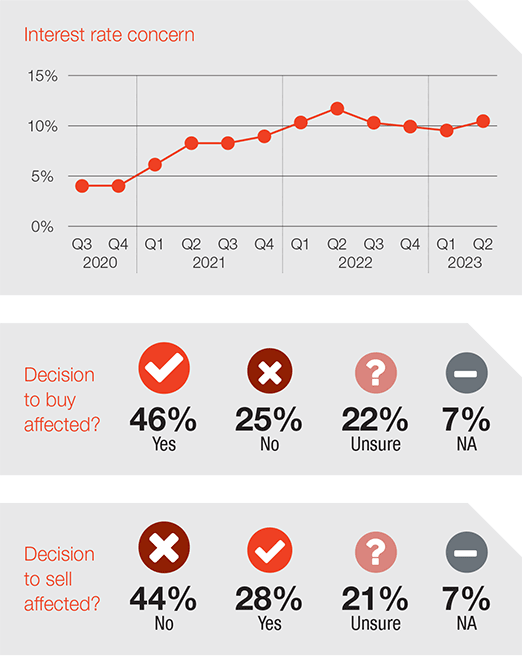

When asked outright if interest rates would impact their decision to buy property in the next 12 months, that figure has continued its steady climb, up another 4 per cent over the quarter to almost half of respondents saying it would have an impact (46 per cent).

Borrowers are also more sensitive to the size of prospective rate rises, with a rapidly rising number of respondents saying a hike of 0.25 to 1 per cent is enough to stifle their buying plans (up from 21 to 29 per cent).

Those concerns appear unlikely to abate.

The prospect of more interest rate hikes over the coming months remains very real. Economic factors that contribute to high inflation remain elevated. Inflation is still double the Reserve Bank of Australia (RBA) target band of 2 to 3 per cent, the unemployment rate remains close to a 50-year low and wages growth has picked up. While the latter two components sound positive, it’s bad news for inflation and therefore interest rates.

4. RBA falling out of favour fast

Ending months of speculation, the Federal Government recently confirmed Dr Philip Lowe’s reign in the RBA’s top job would end in September. For many of our respondents, it’s not a moment too soon.

The RBA is falling out of favour. A troubling 47 per cent of respondents gave the RBA a fail mark for having performed to a poor or very poor level. The amount that gave the RBA a mark of average or above was 54 per cent, well down from the 61 per cent of last quarter. Tellingly, the big shift was in the proportion that rated the RBA’s efforts as very poor, which took off from 15 to 25 per cent in the past three months. Conversely, a measly 3.7 per cent rate the RBA’s performance as very good.

Mr Lowe had been criticised for telling borrowers that interest rate rises were unlikely until 2024, which proved costly for many who acted on that guidance, and for the slow start to monetary policy tightening in early 2022. The RBA’s first female governor, Michele Bullock, will have a chance of resetting the public’s relationship with the reserve bank.

5. Signs of hope for hard-hit renters, borrowers

In a self-perpetuating and rather messy cycle, climbing rents are contributing to high inflation, leading to interest rates heading north, which in turn is driving investors out of the market, which is leading to lower vacancy rates and ever higher record rents, which feeds into the Australian Bureau of Statistics’ inflation data, again contributing to interest rates going up on an almost monthly basis.

It’s a vicious cycle the RBA hopes to break through the unpleasant side effects of higher unemployment and subdued consumer spending, even if it comes with the risk of fuelling a recession.

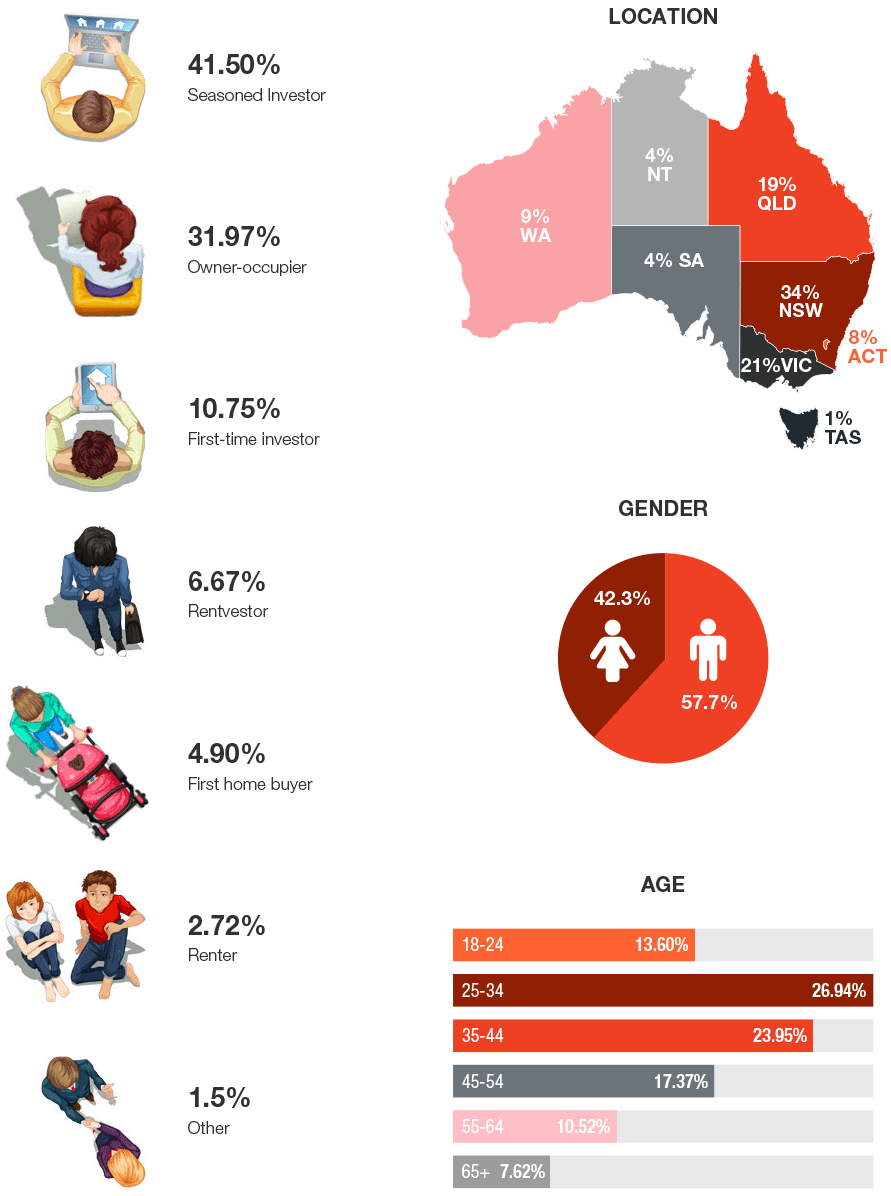

API Magazine’s survey report is well placed to take the pulse of investor sentiment, with three quarters of respondents being landlords and 41 per cent regarding themselves as seasoned investors.

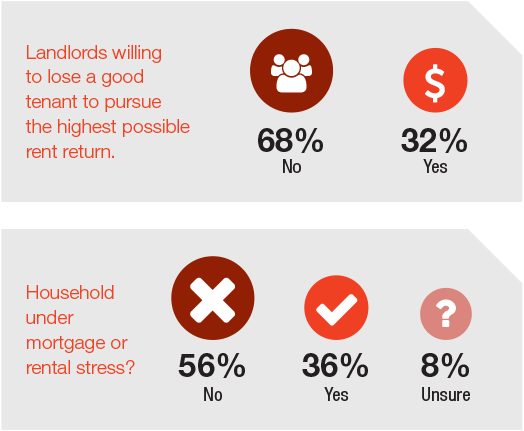

So renters can perhaps take some small comfort in the fact that despite landlords facing their own difficulties paying off higher mortgages, there was a large decline in the proportion of landlords who said they would be willing to lose a good tenant to pursue the highest possible rent return (down from 47 to 32 per cent over the quarter).

This could be attributable to a decline in the percentage of people who say they are under mortgage or rental stress. While still disturbingly high at 36 per cent, it was an improvement on the 43 per cent of the previous quarter. Disconcertingly, 79 per cent said their financial stress status had eventuated over the past 12 months.

Behind the numbers, real life stories are playing out too. Financial stress is often accompanied by unwanted changes in our lives. While more prosaic economic matters previously topped the list of reasons for not buying an investment property, in just one quarter ‘life circumstances’ has moved from a distant fourth to the number one reason (19 per cent of respondents).

6. Incentivising build-to-rent

Build-to-rent (BTR) is still in its relative infancy in Australia but is growing in stature.

It’s a housing model in which only 20 of our respondents (1.7 per cent) say they will live in during the next 12 months, yet BTR has taken on significant status as a key weapon in the fight against diminishing housing supply and a rental crisis.

Despite 46 per cent of our respondents disagreeing with it (compared to 36 per cent in favour), reforms adopted by the Albanese Government in its Federal Budget reversed 2019 legislation that doubled the Managed Investments Trust withholding tax rate from 15 per cent to 30 per cent on payments to foreign investors from residential housing income. Overseas investors are the BTR industry’s primary funding source.

Either way, the BTR model of living is now firmly in the spotlight and earmarked as part of the solution to Australia’s housing crisis.

Survey respondent profile

Investor sentiment

What direction do you see property prices heading?

As an API Magazine article published, appropriately, on April Fools’ Day highlighted, making predictions about property price trajectories is fraught with danger.

In a study conducted this year based on forecasts made at the start of last year, 24 economists made property price predictions with only three anticipating the falls that materialised. That’s an unimpressive strike rate of 12.5 per cent.

But no number of studies will stop people from having an opinion.

What’s clear at the moment is that property has turned a corner, with most capitals close to erasing annual losses on the back of a quarter of solid growth. In the case of Perth and Adelaide, they have already done so.

Nationally, prices are up close to 3 per cent in the last quarter, suggesting the annual deficit of 5.3 per cent will be overhauled before 2023 is complete. Most regional markets are also trending higher.

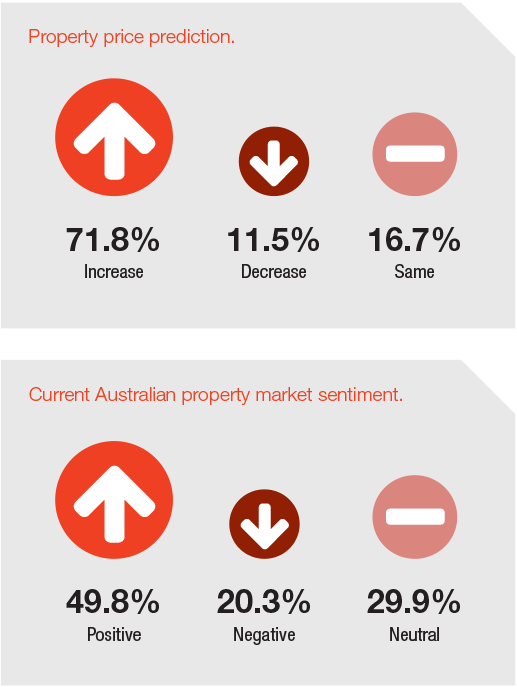

Our respondents believe there is plenty more upside in the property market, with 72 per cent expecting property prices to increase nationally, while 55 per cent believe regional property prices will increase.

When asked for an overarching opinion on the current state of the Australian property market fewer than half of respondents (49.8 per cent) had a positive outlook but it was still 6 per cent higher than last quarter. Only 20.3 per cent said they felt negatively, which was down 8 per cent from the previous quarter.

Investor concerns

What are your most significant concerns around the Australian property market?

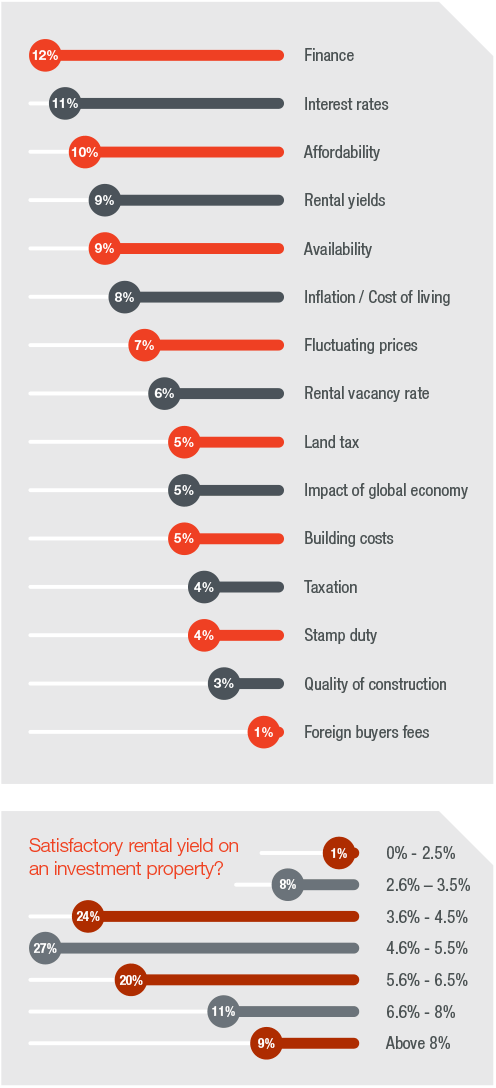

As the interest rates juggernaut continues its skywards path, they’ve overtaken property affordability in the minds of property investors and buyers around the country.

As the property market has arrested its slide, one of the other decision-making variables that has changed significantly is price fluctuation. Just three months earlier, it was third most important factor for those pondering a property transaction in the coming 12 months. This time around it is down at sixth.

Building costs have caused havoc in the sector, leading to the collapse in just one year of more than 2,200 building firms. A near doubling of the proportion of respondents identifying these cost blowouts as a concern when it comes to buying is the result.

As banks tighten their lending criteria and build in bigger interest rate buffers, finance availability remains the primary challenge when it comes to making a property move up to the first half of 2024.

Rental yields are another prominent factor among our survey respondents. A range of 3.6 to 6.5 per cent was generally regarded as a satisfactory rental yield on an investment property. The vast majority of respondents (27.3 per cent) indicated 4.6 to 5.5 per cent would be satisfactory, which corresponds with the national average for houses of 5 per cent, according to SQM Research.

Expert’s commentary: Andrew Bell OAM, Owner-operator, Ray White Surfers Paradise Group

It is no surprise that experienced investors see this as one of the greatest periods of time an investor has ever experienced. The best returns through the significantly high and ever-increasing rental returns and continual capital growth in their property’s values equate to investor utopia.

Investor finance

Plea to banks as property market sentiment improves

Real estate values have enjoyed a rebound after a sluggish start to the year and property market sentiment has ticked upwards as a result.

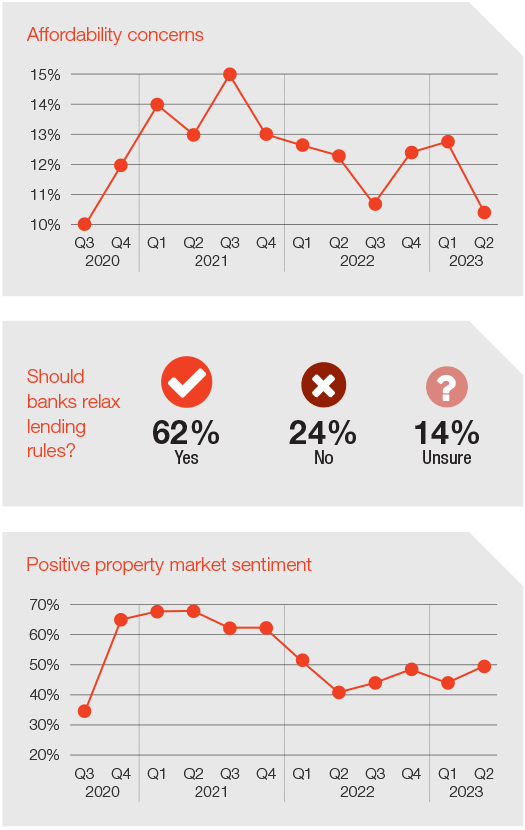

Despite many homeowners coming off low fixed rate interest loans for the remainder of 2023, affordability concerns actually waned among our respondents.

With the fixed loan interest rate generally higher than the variable loans it is no surprise that 52 per cent of respondents have chosen a variable loan structure. Of the 26 per cent that are locked into a fixed rate mortgage, 32 per cent said their strategy once the loan expires is to pay a lump sum to reduce debt, while 22 per cent said they plan to renegotiate the rate with their current lender.

There is still a lot of resilience in the market. Monthly repayment increases haven’t caused as much pain as predicted. Savings buffers were built up during the Covid crisis and the level of household income is only a little below a pre-Covid trend even after taking inflation and interest rate increases into account.

The lack of credit availability is stifling investor activity, reflected in the near two thirds of respondents wanting banks to ease their lending rules.

Refinancing hitting record levels also suggests troubled borrowers are searching high and low for a better deal too. Of those surveyed, 46 per cent indicated that rising interest rates would affect their intention to buy, with 53 per cent saying that an increase of 0.25 to 2 per cent would alter their decision making, however, 44 per cent said rising interest rates would not influence their decision to sell a property.

Unusually high inflation was the cause of a massive 71 per cent of respondents saying it will impact their ability to enter the property market or make a property transaction.

Expert’s commentary: Helen Avis, Director of Finance, Specialist Mortgage

By the end of 2023 another 40 per cent of fixed rate loans will expire and by the end of 2024 another 20 per cent, presenting what has been dubbed the mortgage cliff, and that could play out in stifled property price pressure. There’s a reason refinancing is at record levels and that’s because there’s significant money to be saved by doing so.

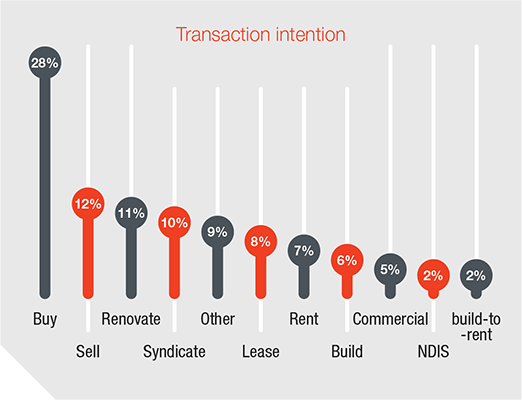

Investor intentions

What’s your next move within the coming 12 months?

It seems Queensland can never be written off when it comes to preferred property investor destinations.

Three short months ago this corresponding property sentiment report was declaring the love affair with the sunshine state was waning, if not necessarily over. Well, the Sunshine State is back.

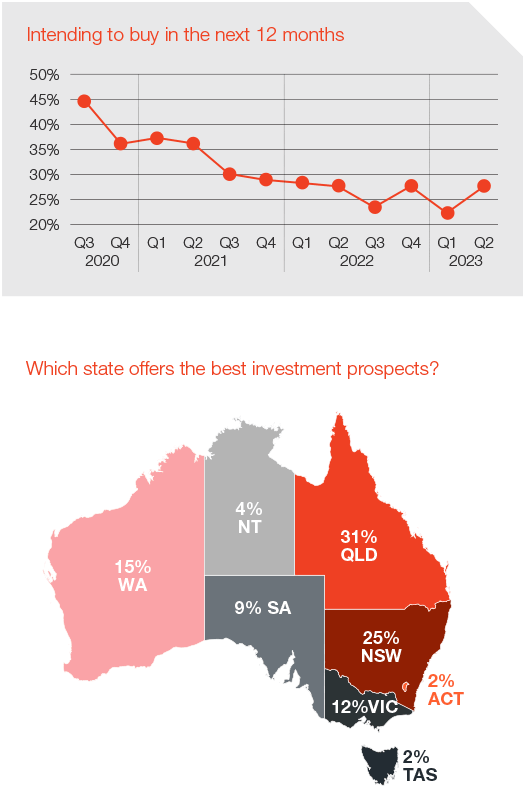

After the first quarter of 2023, New South Wales had taken the mantle as the prime state on the radar of property investors for the coming 12 months. But in an impressive comeback, Queensland has again usurped its more populous southern neighbour.

Despite Sydney property prices now outpacing growth in all other capitals, Queensland has taken a massive leap to command the attention of 31 per cent of respondents (24 per cent last report). This compares to New South Wales’ 25 per cent (down from 27 per cent).

Investors seem to be retreating from markets perhaps seen as more adventurous, with ACT, Northern Territory and Tasmania all at half or even a quarter of the interest level they commanded last survey.

Western Australia and South Australia, the two best performing markets over the past year, have only enjoyed a marginal increase in terms of perceived prospects.

Among the 52 per cent of respondents who said they are property investors, Queensland is where 26 per cent own investment properties, followed by New South Wales (22 per cent).

Respondents’ quotes

These were some among the hundreds of comments that demonstrated the diversity, disparity and breadth of opinion:

Australia’s real estate market will remain weak in the short term but in the long run will continue to face the test of insufficient housing supply. Real estate development is still a good choice.

Everyone seems to overlook the fact that when interest rates go up it affects landlords who ultimately have to raise rents or sell their property. Caps on rent increases will ultimately result in landlords having to sell their properties.

Something more needs to be done for our young first home buyers. The average income level is now the working poor due to high inflation and increasing property prices. Stamp duty is too high and the recent land tax in Victoria really is unfair.

Despite the more favourable returns at the moment, I am sick of the uncertainty of government actions and the constant demonisation of landlords and will be selling my investment properties over the next five years.

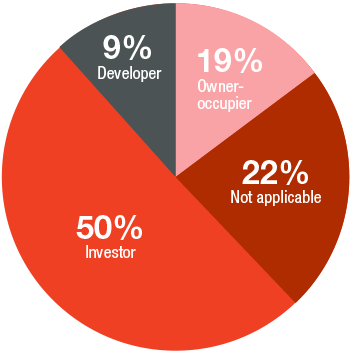

In what capacity will you purchase in the next 12 months?

Investors seem to be one cohort of the property market under pressure, with various states passing legislation that, reasonably or otherwise, is more renter-friendly, which along with higher repayments are driving many from the market.

In the face of these pressures, the proportion of survey respondents making a purchase in the next 12 months as investors still remains unchanged from last quarter at exactly 50 per cent. A couple of years ago this figure was around 75 per cent. Overall, 28 per cent indicated they plan to buy a residential property (up from 22 per cent last quarter), while 12 per cent are intending to sell (up by 2 per cent). A further 17 per cent plan to build, subdivide or renovate.

Over 12 months, rents have risen 9.7 per cent compared to Australia’s inflation rate of 5.6 per cent.

Investors paying off higher mortgage repayments every month would be hoping to recoup some of their expenses through higher rents. But national gross rental yields are actually inching lower and investors see little reason to pile into the market, leaving rental supply languishing.

What type of property are you considering in the next 12 months?

For the first time since API Magazine’s sentiment surveys have recorded this metric, units last quarter overtook detached houses as the property of choice when it comes to investment intentions.

Units’ tenure at the top was short-lived and its dethroning brutal.

Houses and apartment prices have broadly remained in step over the years, however, houses have generally been seen to deliver higher growth while units have experienced less volatility and been more resilient in downturns.

With property prices on the up, there’s been a major swing back to houses as the investment of choice. Units have even been overtaken by townhouses for the first since our reports began.

While assets such as medical centres and neighbourhood shopping centres have enjoyed high demand of late, the appeal of commercial assets has fallen from 16 to 9 per cent since the previous report.

Expert’s commentary: Hayden Groves, President, Real Estate Institute of Australia