Melbourne houses better investments than apartments

Detached dwellings in Melbourne potentially provide stronger wealth creation opportunities than apartments, with asset appreciation more important for investors than cashflow.

Detached dwellings in Melbourne potentially provide stronger wealth creation opportunities than apartments, with asset appreciation more important for investors than cashflow.

If you’re looking to increase your long-term wealth by building a quality property investment portfolio, you should prioritise capital growth over rental yield.

In doing so, you should invest in the type of properties that increase the most in value over time: houses.

Land appreciates in value, whereas the dwellings that sit on land tend to depreciate in value. Think about why you get a property depreciation tax break when you rent out newly built properties.

Properties with reasonable land content such as houses or townhouses experience significantly higher capital growth than properties that lack land content such as apartments or units.

Most of us know this intuitively, but what does the data say?

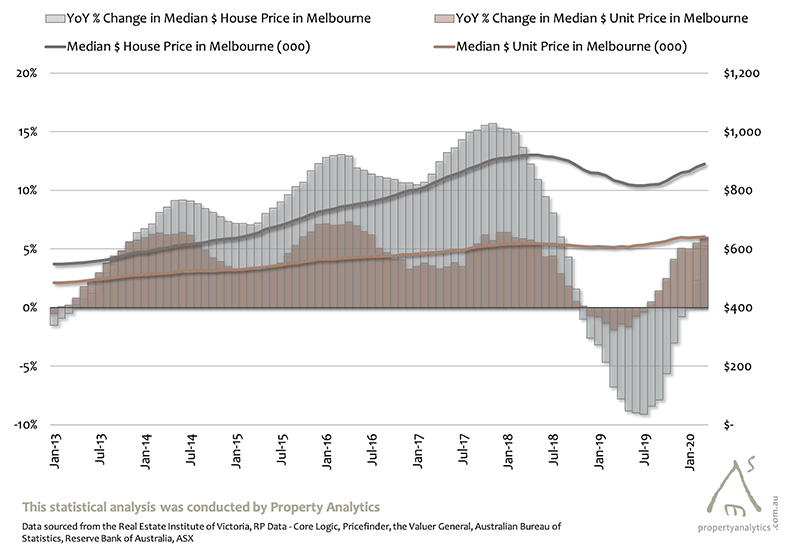

The below graph compares how house prices and apartment prices have fluctuated over the last seven years in Melbourne. The red and grey bars show the year-on-year price changes by percentage, whereas the red and grey lines show the actual prices.

When the Melbourne market was rising, house price growth was consistently two to three times greater than apartment price growth.

The market experienced its sharpest correction in living memory from 2018-2019, and house prices were affected significantly more than apartment prices. But, even allowing for the recent market downturn, houses still outperformed apartments by half.

Below are some case studies that prove the point:

There are 3 key metrics that every property investor should know:

- The equity (cash) needed to purchase and retain a property investment – based on the Loan:Value Ratio, mortgage repayments made after rental income, and various other purchase and holding costs (e.g. stamp duty, council rates, land tax, etc)

- The equity gained through capital growth

- The Net Position – difference between equity needed and equity gained

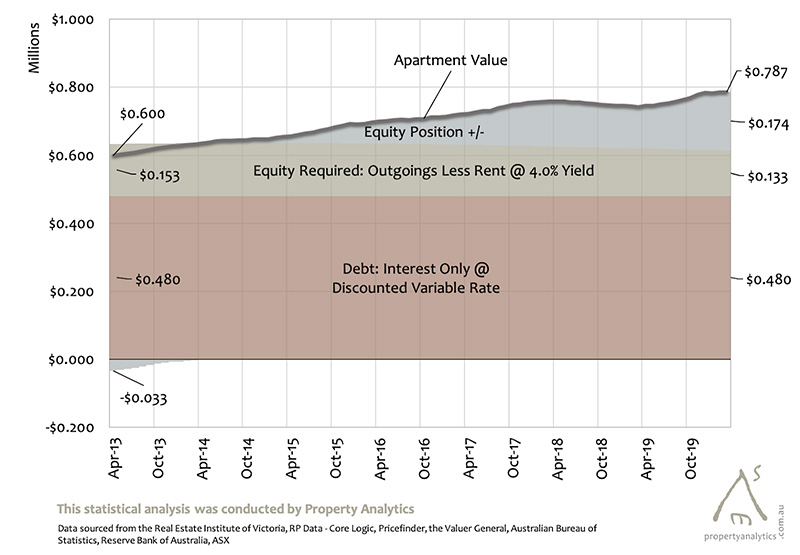

We’ve graphed these 3 metrics for an apartment purchased in early 2013.

An apartment purchased in April 2013 for $600,000 would have required about $153,000 in equity. The purchase costs (stamp duty, legals, finance) meant that the initial equity + debt exceeded the apartment value.

Over time, capital growth and declining interest payments (the RBA dropped rates continually through this period) delivered an increasingly positive equity position. In seven years, the apartment increased in value by 31 per cent. Net equity improved from $120,000 to $307,000 (+156 per cent).

The same 3 metrics are graphed for a house purchased in early 2013.

A house purchased in April 2013 for $600,000 would have required about $154,000 in equity. The purchase costs (stamp duty, legals, finance) means that the initial equity plus debt exceeded the house value.

Over time, capital growth and declining interest payments delivered an increasingly positive equity position. In 7 years, even allowing for the most severe price drops in living memory from 2018-19, the house increased in value by 61 per cent. Net equity improved from $120,000 to $480,000 (+307 per cent).

This analysis demonstrates that, despite lower rental yields, houses make far better investments than apartments.

It also demonstrates the huge benefits associated with debt leverage. Where the median house price grew by 61 per cent over the period, the equity gain was more than 300 per cent. This, fundamentally, is what makes property so appealing as an investment class.