Looking back at 2021 and forward to 2022 – what will it hold for Australia?

As we head towards a new year, we reflect on how the property and investment markets fared for 2021.

As we head towards a new year, we reflect on how the property and investment markets fared for 2021.

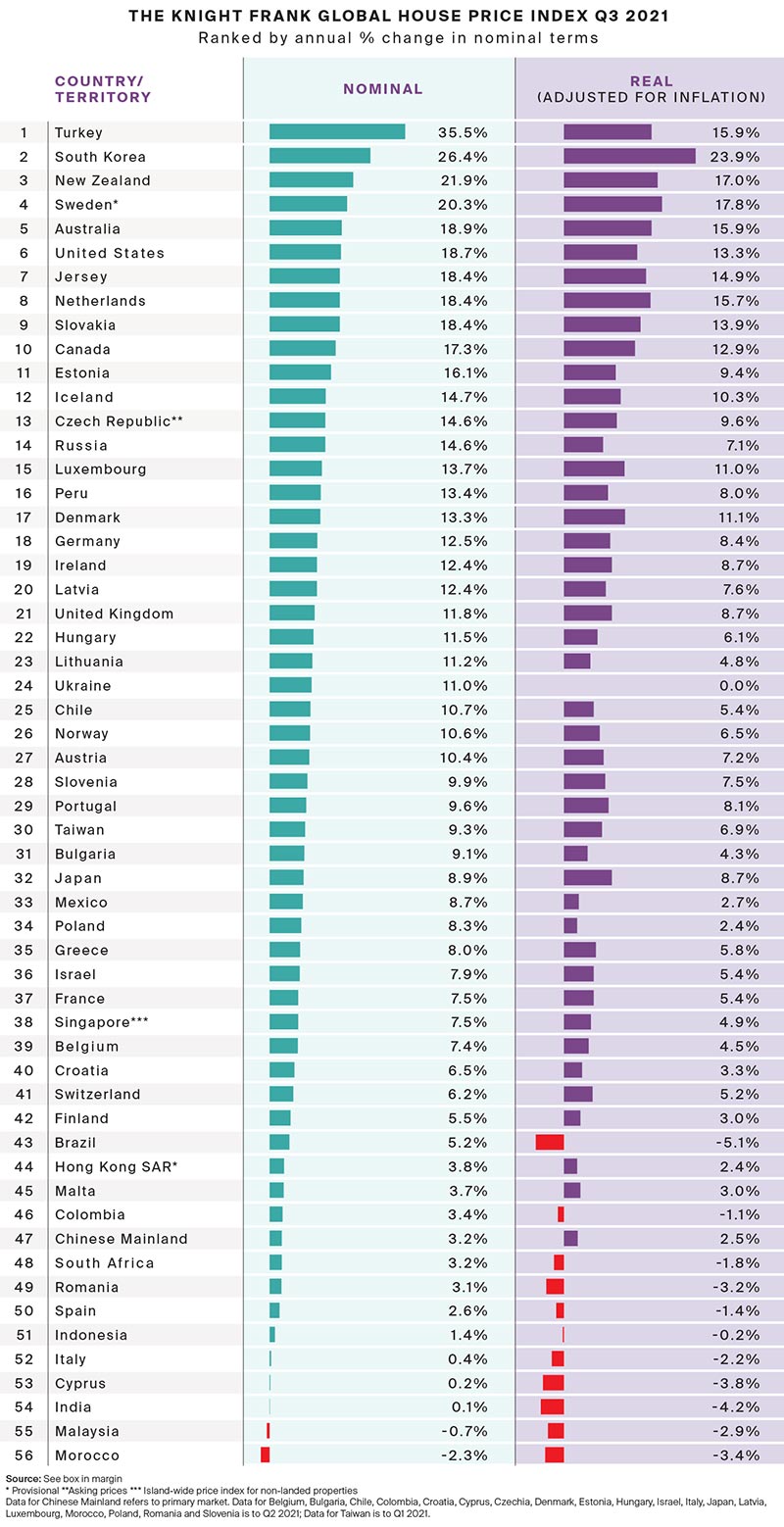

Australia in Top 5 for global house price increases

In Knight Frank's Q3 Global House Price Index, which tracks the movement of mainstream house prices across 56 countries and territories worldwide; Australia was ranked 5th globally in house price increases.

Prices increased on average by 9.4% across the 56 countries and territories with 96% (54 of 56) registering a positive price growth year-on-year. Australia's annual year-on-year growth alone was 18.9% in Q3 up from 16.4% in Q2 2021, signalling the mainstream market having had eight quarters of uninterrupted positive annual growth.

Shayne Harris Partner and Head of Residential, Knight Frank Australia said the last time Australia was in a top five position was at the end of 2015 prior to tightened lending restrictions being implemented.

"The impact that the pandemic has had on our house prices is clear, with Knight Frank data showing that our average annual price growth from 2015 – 2020 was 4.4%, which rose to average growth of 9.8% since the start of the pandemic. As at Q3 2021, the Australian market continues to heat up as much desirable stock is in short supply and interest rates remain at historic lows.

"However, we do expect the growth in Australia's house prices to slow in 2022, perhaps by as much as 10% (from 18% in 2021 to 8% in 2022), as we reach a tipping point for affordability. As we move into 2022, we expect Australians to be influencing by further restrictions of lending, an increase in house listings and different considerations about how they deploy their capital as international travel resumes and some elements of pre-COVID life return."

The proportion of housing markets witnessing annual price growth in excess of 10% now sits at 48%, up from 13% at the start of the pandemic, and as Knight Frank discussed in their Global Prime Residential Forecast for 2022, the real estate boom we've seen globally is expected to continue into 2022, Omicron and new variants permitting.

Housing contributing to Australia's economic recovery

The property market's fastest upswing on record, accompanied by a rapid increase in housing credit and highly elevated sales volumes has significantly supported Australia's post-pandemic economic recovery. CoreLogic's latest Economic & Property Review provides a national overview of the $9.4 trillion sector's performance within the current economic landscape.

National dwelling values rose 22.2%, comprised of a 25.2% lift across regional Australia and a 21.3% rise in combined capital city dwelling values in the 12 months to November 2021. In the same period, there were an estimated 614,635 dwelling sales across the country, which is the highest annual sales volume since December 2003.

Report author, CoreLogic's Head of Research Eliza Owen, said strong housing market activity has been supported by a combination of factors, including low interest rates and relatively subdued levels of available stock.

"Housing-related government support such as the First Home Loan Deposit and HomeBuilder schemes and non-housing fiscal stimulus, such as JobKeeper, helped many Australians service housing costs such as rents and mortgage repayments.

"Alongside home loan repayment deferrals, these household support measures stabilised the supply side of housing through 2020 by preventing distressed sales, and these repayment deferrals were reintroduced amid lockdowns in 2021," she said.

Australia's household savings rate also increased to 23.6% through to June 2020 against a then decade average of 6.9% on the back of strict pandemic lockdowns and inhibited short-term consumption spending.

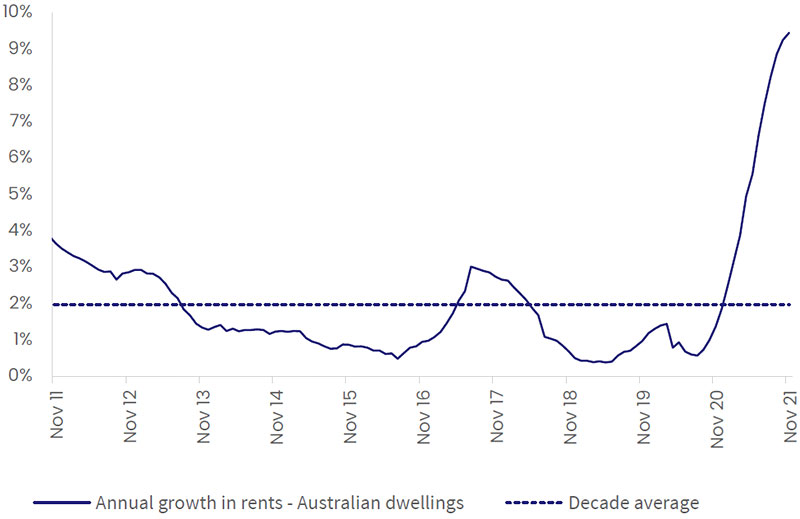

Australian rent values have also seen a strong uplift at the national level, increasing 9.4% in the 12 months to November 2021, which is the highest rate of annual appreciation since January 2008.

Annual growth in rent values

Source: CoreLogic

Ms Owen says there is evidence of growth rates easing in the Australian housing market and the broad-based upswing of early 2021 was no longer applicable due to the variation in dynamics across the states and territories.

"Momentum in the housing market is slowing quickly in Sydney and Melbourne, which is likely due to a relatively high number of listings now on the market and severe affordability constraints," she said.

"Across Melbourne, demand appears to be shifting to more affordable areas of the city, with lower value dwelling markets seeing a pick-up in quarterly growth rates. Similarly, value gains are accelerating across regional NSW, while affordability weighs on dwelling demand across Sydney."

In Brisbane and Adelaide value growth rates have reached the highest levels seen in more than a decade and are continuing to accelerate.

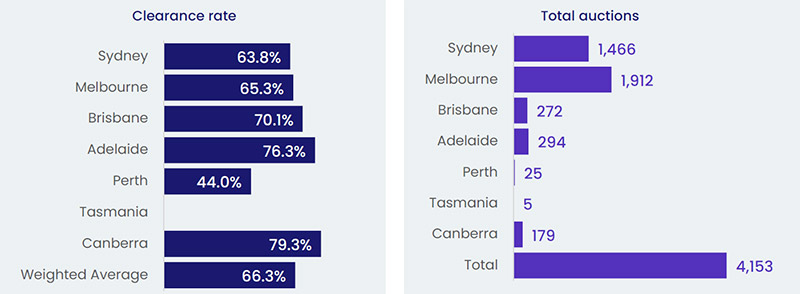

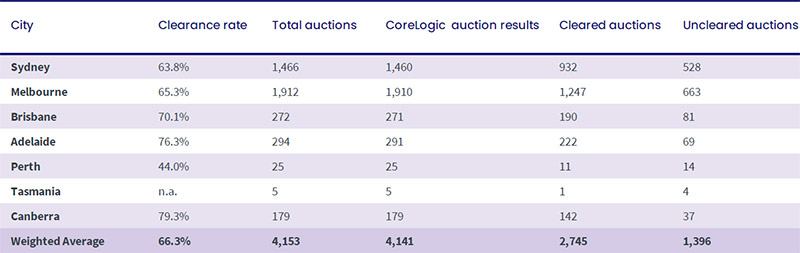

Capital city auction statistics - w/e 5 December 2021

Source: CodeLogic

Ms Owen warned the high value growth and above-average rates of housing turnover recorded in 2021 are unsustainable, particularly with forecast headwinds such as recent changes to mortgage lending conditions and signs of interest rate increases, both of which are likely to slow housing demand.

"As a result, it is expected that 2022 will see far milder rates of appreciation in Australian dwelling values."

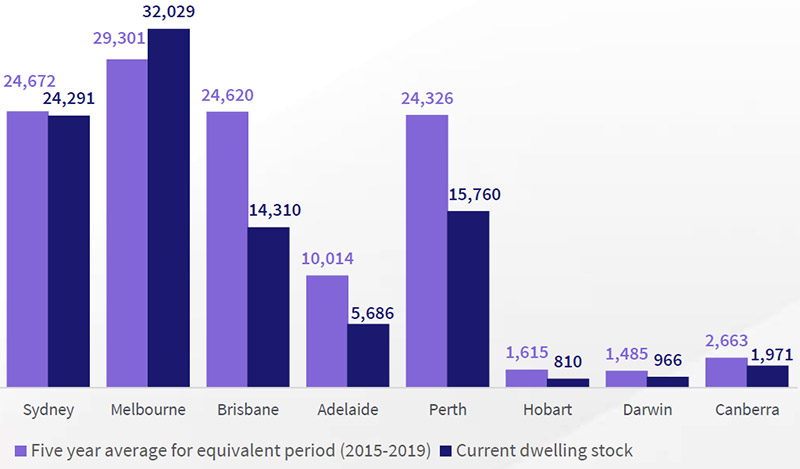

Count of listings in the four weeks to 28 November 2021, compared to previous five year average (2015-2019)

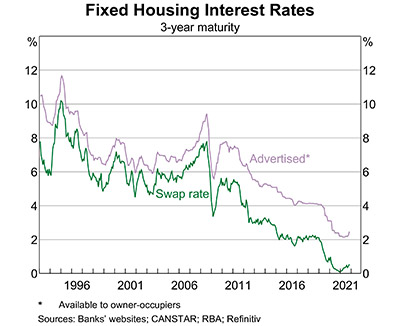

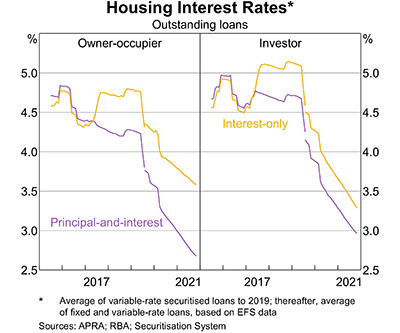

Interest rates

Finder RBA Cash Rate Survey, also highlighted the opinions of experts regarding the direction of interest rates coming into 2022.

Speculation is rife as to when and how much the RBA will raise rates; from inflation, unemployment and wage growth there are a number of factors and subsequent opinions for when and if rates will increase into 2022.

Shane Oliver of AMP Capital is suggesting an increase towards the end of 2022; "The combination of slightly higher than expected inflation than the RBA is anticipating, a decline in unemployment to around 4% over the next 12 months and a faster than expected pick up in wages growth taking it to near 3% are expected to see the RBA start raising interest in November next year."

David Robertson from Bendigo Bank agreed, "The economic recovery underway (together with rising inflation) will see pressure on the RBA to increase official interest rates by next December, although there is uncertainty around the new Omicron variant. Assuming vaccines and boosters are effective for Omicron, the recovery should continue and higher rates should be expected through Financial Year 22/23."

Many believe the RBA will wait until inflation is above 3% and wage growth is strong before making any changes. Headline inflation should start to ease but with the construction industry facing increased costs this could be the risk the RBA is expecting. In comparison Central Banks in other countries are starting to lift their rates so the RBA may have their arm twisted sooner than they would have liked.

Tom Devitt of the Housing Industry Association disagrees that the industry supply constraints will have an effect on inflation, "Current supply chain issues are still expected to be temporary and not feed into ongoing inflation, which means it will still take a while for the tightening labour market to generate sustained stronger wage growth and inflation."

Peter Boehm of CLSA Premium suggests rate rising will come down to timing. "The key will be the period over which the RBA increases rates to their neutral position of between 2.5% and 3.0%, and by what increments. Even a 0.25% increase could have negative impacts on the economy. The RBA will want to ensure any rate increases don't lead to material asset price deflation and/or recessionary impacts."

Whereby Saul Eslake of Corinna Economic Advisory doesn't think the RBA will be swayed by other leaders in the game. "I think the RBA's right that the data and forecasts don't "warrant" an increase in the cash rate in 2022 - but I think one will be "warranted" by Q2 2023. The RBA won't be influenced by other central banks including the Fed moving sooner indeed, they'd likely welcome the further fall in the A$ which would result from that."

"Interest rate noise is getting louder but the Reserve Bank has been clear in its communication that rates won't go up unless economic and inflationary pressures take an unexpected turn. The consistency of this position is appropriate." – Leanne Pilkington, Laing + Simmons

"Despite increasing inflationary pressures and ongoing property price growth, the RBA will continue to hold rates steady over the short term. The RBA is expected to raise rates once it is comfortable the Australian economy is back on a strong footing and the Omicron variant of COVID-19 doesn't present a risk to growth." - Mathew Tiller, LJ Hooker

The RBA won't increase rates until inflation is well entrenched and wages have risen and will keep growing. At present one-off factors are driving up inflation." - Michael Yardney, Metropole Property Strategists "

"The RBA is wanting to see improvements in the labour market lift wages growth and drive inflation. I expect it will want to gauge the state of the economy through 2022 as tailwinds fade and borders reopen before concluding it is on a sustainable path to achieving this objective." - Alex Joiner, IFM Investors

Following news that ANZ increased its 4- and 5-year fixed home loan rates by 40 points, making it the bank with the highest rates of any of the big four, it shows the importance of locking in a home loan rate as soon as possible, whether you're refinancing or buying.

"We see the current path to a 2024 rate rise as appropriate, though it will be interesting to see what 2022 brings. Tim McKibbin Chief Executive Officer REINSW concluded.

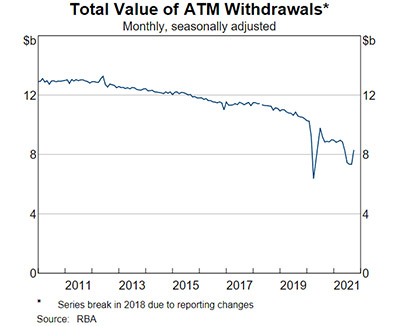

A cashless society

There has been an increased trend in electronic payments with the declining use of banknotes and greater use of digital wallets that one could argue started to increase due to the global pandemic and is likely to continue. There has been particularly strong growth in debit card transactions as people move from credit to debit and account-to-account transactions.

The value of ATM withdrawals over the past six months was around 30 per cent lower than the comparable period three years ago. While banknotes are still used for many transactions, the trend here is clear.

Another trend is smaller players entering the market that focus on specific elements of the payment value chain that brings with it increased competition and new business model with 'fintechs' driving innovation in areas including online payments, point-of-sale acceptance technology, cross-border retail payments and buy now, pay later (BNPL) services.

And lastly, cross-border payments; it still costs around 5% (and sometimes more) of the total payment to send money internationally from an Australian bank and takes more than a day to reach the recipient.

At the recent AusPayNet's annual Summit Philip Lowe Governor of the Reserve Bank of Australia (RBA) said more needs to be done to make cross-border payments cheaper, faster, more transparent and more accessible.

"The RBA is contributing to this effort and working with the Reserve Bank of New Zealand and other South Pacific central banks on a possible regional Know Your Customer (KYC) utility.

"We are looking for the Australian payments industry to support these and other initiatives to improve the existing infrastructure for cross-border payments. A large effort is required here, but it is one that we need to make to provide better services to customers and to meet our international commitments.

"To conclude, our payments system is changing quickly. Both the regulators and the government understand this and are seeking to put in place arrangements that encourage innovation and competition and make sure we have a secure and efficient system. We have work to do here, but are moving in the right direction." Said Mr Lowe.

Will crypto finally make a mark?

Cryptocurrency can be considered a digital token, that is not linked directly to the AUD or backed by a particular entity of asset.

Phillip Lowe Governor of RBA remains sceptical of cryptocurrency being used for general purpose payments.

"It is likely that the asset used for the settlement of most transactions in the economy will remain some form of secure fiat currency with a stable value, rather than cryptocurrency with a volatile price.

"That is not to say there is no role for crypto-assets. They can help support innovation, especially where they are linked to smart contracts and used in decentralised finance (or DeFi) applications. "There is value in experimentation to find out what works and what doesn't. But as the experiments are conducted, it is also worth considering whether the benefits of smart contracts and DeFi can be gained with some form of stablecoin or a CBDC, rather than a new unit of account with a volatile price."

Economists are split on the role that cryptocurrency will play in Australia's economy over the next few years, according to this month'sFinder RBA Cash Rate Survey, where 37 experts and economists weighed in on future cash rate moves and other issues relating to the state of the economy.

While all panelists correctly predicted a cash rate hold in December, almost half (46%, 17/37) are expecting a rate increase in 2022, with 42% believing cryptocurrency will have a greater role to play in the Australian economy over the next few years.

Dale Gillham of Wealth Within said that around 1 in 5 Australians are investing in or are looking to invest in cryptocurrencies in the near future.

"With the massive shift from being a cash society, Australians, like others around the world, are looking at alternatives that the government has little control over." Jeffrey Sheen of Macquarie University said private cryptocurrencies will remain speculative "meme" investments.

"They will never be able or allowed to compete with strong fiat currencies in transactions. Central bank digital currencies in some forms will become a significant part of the transaction landscape."

Following Commonwealth Bank's announcement to allow its customers to hold and trade Bitcoin and other cryptocurrencies via its banking app, the majority of economists who weighed in (77%, 20/26) are expecting other major banks to follow.

Graham Cooke, head of consumer research at Finder, said interest in cryptocurrency is showing no signs of slowing down.

"Finder's Cryptocurrency Adoption Index shows that Australia has the third-highest rate of cryptocurrency ownership. "It shows cryptocurrencies are more trusted in countries with less transparent economies."

The majority of experts (85%) believe that cryptocurrency is seen as a safe haven for people in countries with a less trusted economic system. Noel Whittaker from QUT noted that banks will push cryptocurrency further into the mainstream.

"Of course, it will depend on the type of cryptocurrency, but I noticed banks are starting to offer it. This will increase its popularity."

Like the currency itself, speculation is still very divided on its success and continues to be the centre of debate; one thing is for sure, no one is set on its future just yet.

And that's a wrap for 2021!