In the face of so much property negativity, hope still abounds

With so many forces at play to stifle the property market it's easy to assume it's all bad news (or good news for those wanting prices to fall), but there are some telling signs that the real estate market woes will be relatively short-lived.

As a property owner or investor, you could be forgiven for thinking the sky is about to fall in.

There’s near-certainty of numerous rate hikes this year, the rate of profit-making real estate resales has plateaued and property prices continue to tumble.

As they would say in the popular kids’ show Horrible Histories, “but wait, there’s more”.

Household wealth fell 3.3 per cent ($484 billion) in the June quarter 2022.

Inflation is around 30-year highs and appears unlikely to be untamed in the near-future, regardless of the RBA’s robust efforts.

People are still spending heavily, which will do nothing to stem inflation and therefore interest rates. In the face of mortgage rates chewing hundreds more dollars from monthly household budgets, consumers still managed to spend an extra 0.6 per cent in the shops in August, according to the Australian Bureau of Statistics.

Yet, somehow, there is still a glimmer of hope for borrowers and property owners.

History repeats

Nationally, Australians remain an optimistic bunch.

A survey by ANZ and the Property Council of Australia showed an uptick in confidence this month in house price growth prospects.

While West Australians are the only ones expecting property prices to actually increase in the next 12 months, the proportion of people in New South Wales and Victoria who thought they’d decline was far fewer (at around -35 to -25 respectively, with zero being the point where prices were overall expected to remain the same).

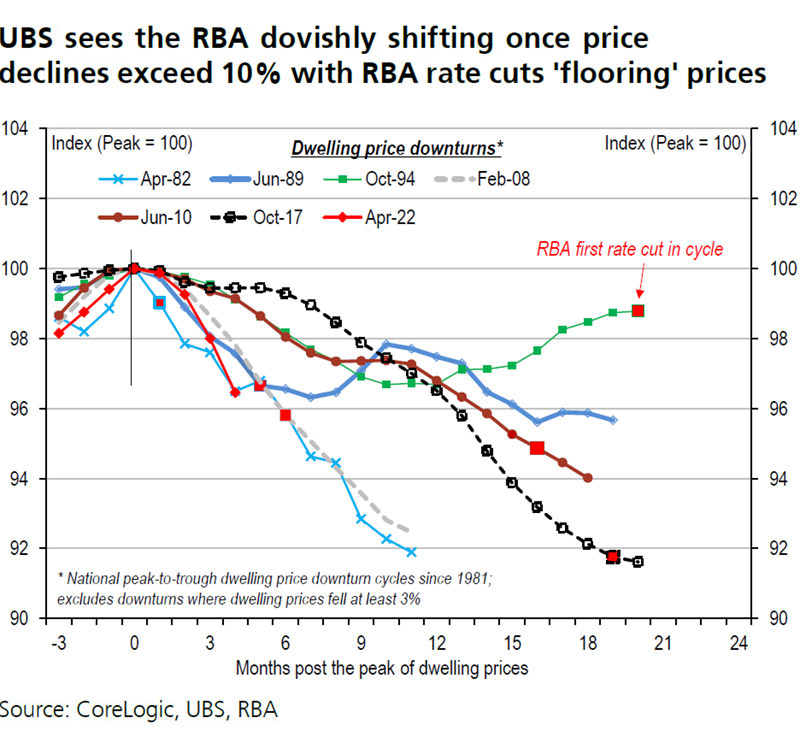

Financial services company and investment bank UBS has also suggested that, if history repeats, the Reserve Bank of Australia (RBA) will step back from the interest rates lever before inflation peaks.

“In the past 30 or so years, policymakers have almost always avoided a housing hard landing and, if it started to occur, they shifted their reaction function (and) we see history repeating, provided our inflation view is right (peaking in last quarter of this year and sharply dropping to around 3 per cent by the end of 2023),” Tom Bodor, Analyst at UBS, said.

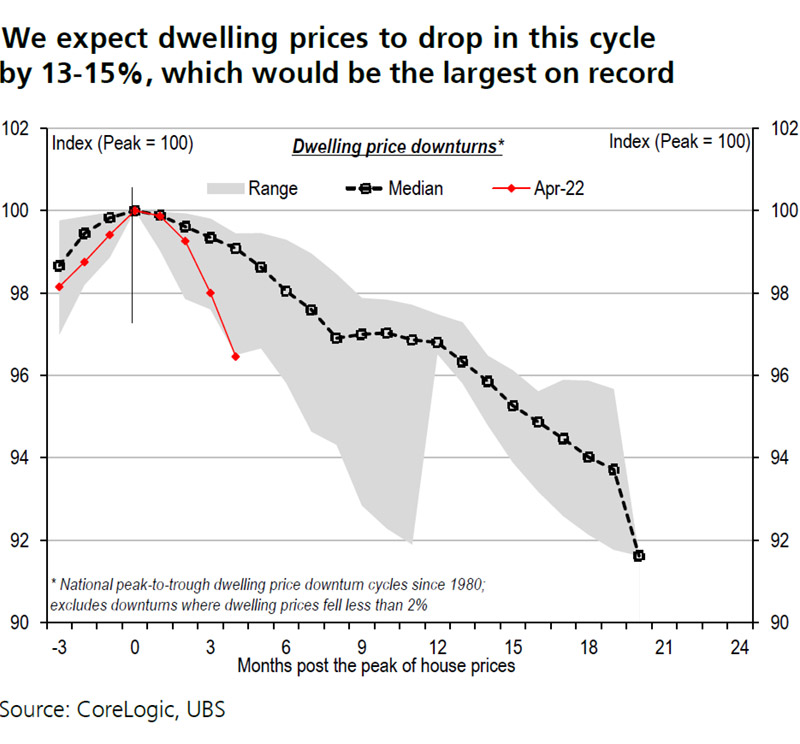

UBS is still arguing that property prices nationally will drop by a record 13-15 per cent from peak to trough but also said four major factors would prevent the worst-case scenarios espoused by other commentators from eventuating.

“A deep housing downturn is priced in, however, we see these factors supporting a recovery: one, low supply; two, a tight rental market with vacancy rates below 1.5 per cent; three, strong employment; and four, migration resuming,” Mr Bodor said.

UBS is forecasts for dwelling commencements to see a decline through 2023 but with the expectation of a sharp recovery in 2024.

Profit-making sales dip

Australian vendors seeking to profit from the resale of their property have seen the peak of the market come and go in the June quarter, as data shows the number of loss-making transactions are on the rise.

CoreLogic’s latest Pain & Gain Report, which analysed approximately 102,000 property resales that occurred in the June 2022 quarter, showed Australia’s profit-making sales plateaued at 93.8 per cent when compared to the previous three months.

However, the rolling quarterly rate of profit-making sales showed the three months to April reached a resale gain peak of 94.1 per cent, which coincided with the height of national dwelling values.

CoreLogic Head of Research Eliza Owen said the April peak for both profitable resales and national home values aligned with the first of several sharp and consecutive rate hikes.

What will a 0.5% rate rise cost?

| Cash rate | Average home loan rate* | Average monthly repayment | Average monthly increase | Average annual repayment | Average annual increase | |

|---|---|---|---|---|---|---|

| April 2022 | 0.10% | 3.45% | $2,231 | - | $26,772 | - |

| September 2022 (current) | 2.35% | 5.65% | $2,886 | $655 | $34,632 | $7,860 |

| October (full rate rise applied) | 2.85% | 6.15% | $3,046 | $815 | $36,552 | $9,780 |

Source: Finder, RBA. *Owner-occupier variable discounted rate. Repayments based on a $500,000 loan.

“This particular Pain & Gain report provides a line in the sand and confirms the moment when the housing market peaked and started to turn,” she said.

“The figures align with peak growth in our national Home Value Index and highlights the decline in the rate of profit-making sales, which has been largely influenced by an increase in the rate of loss-making resales in Sydney and Melbourne.”

Sydney’s rate of loss-making sales increased 160 basis points to 6.4 per cent, coinciding with a quarterly decline in home values of -2.8 per cent over the period. The portion of Melbourne loss-making resales were up 50 basis points in the quarter, to 5.3 per cent, as home values fell -1.8 per cent.

“Multiple interest rate hikes have led to a weakening in the home values in Sydney and Melbourne however residential resale results in some cities remain strong with significant gains across almost all resales,” she said.

“Resales data suggests a notable increase in loss-making unit sales across the Sydney council region, including in high-density city fringe markets like Waterloo, Zetland and Rosebery.”

The report isn’t wholly negative for vendors, with strong resale figures still prevalent in smaller capital cities including Canberra, Hobart and resource cities.

Hobart and Canberra topped the capital cities for the rate of profit-making sales, each with 99.1 per cent of resales achieving a nominal gain. Hobart has recorded four consecutive years of vendors recording the highest rate of nominal gain across the greater capital city markets.

Ms Owen said the improvement in some cities during the June quarter may reflect the actions taken by motivated sellers who took advantage of a recent high in dwelling values.