How much pain can Aussie borrowers tolerate?

As Australians grapple with yet another interest rate increase, API Magazine sought answers on who was most susceptible, how much more pain was in store, and when property markets might stabilise.

Another month and another interest rate rise.

So, just how much can Australia’s increasingly stretched household budgets tolerate in the face of borrowing costs rising at a record pace, pricier goods and services, and wages being corroded by inflation and flatlining for several years?

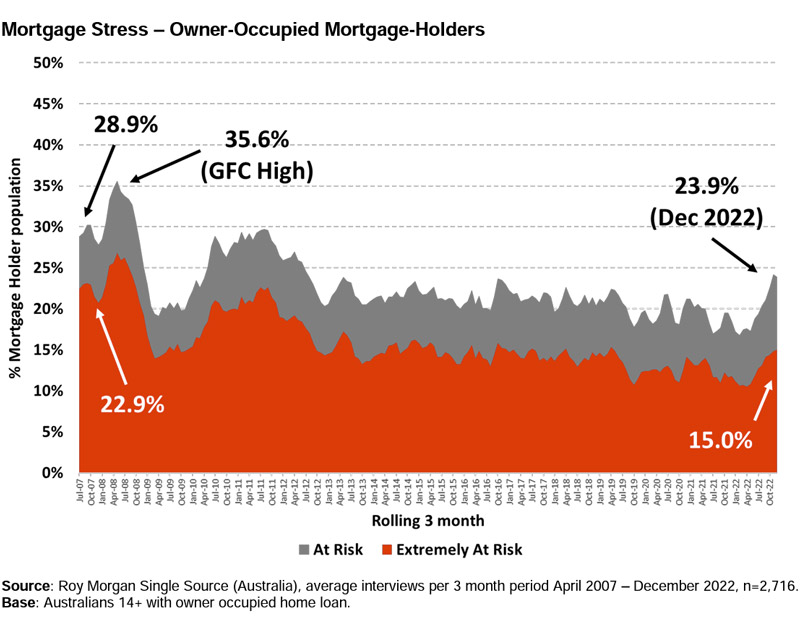

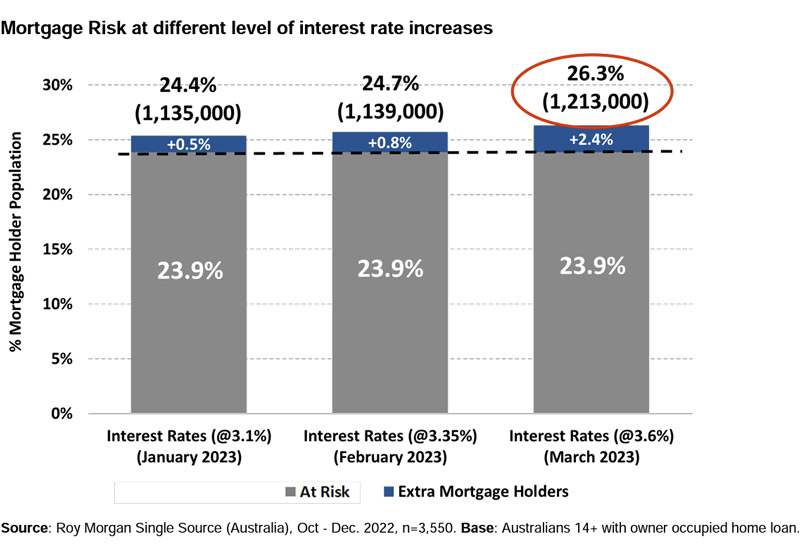

While we’re not at Global Financial Crisis (GFC) levels of mortgage stress, for the first time in this nine-month cycle of interest rate increases the proportion of mortgage holders now considered ‘At Risk’ of mortgage stress (23.9 per cent) is above the long-term average of 22.8 per cent stretching back to early 2007.

The Roy Morgan data shows that mortgage stress, whereby households are spending more than 30 per cent of their income servicing their rent or mortgage, is increasing rapidly but is still well shy of 2009’s GFC-induced level of 35.6 per cent (1,455,000 borrowers).

A wide variety of experts, academics and industry professionals spoke to API Magazine to shed some light on just how much pressure borrowers, renters and property markets could withstand or expect.

First home buyers were widely seen as those facing the most pressure, while renters looked set to be caught in the RBA’s crossfire as collateral damage.

Perth-based CEO of Property Powerhouse, Garth Davis, said new and established buyers and investors were under pressure from rising interest rates.

“Yes, some mortgage holders are ahead of their mortgage repayments and have built themselves up a cash buffer during Covid, however, there are now more than a million mortgage holders under mortgage stress.

“First home buyers and people with the biggest percentage mortgages are the ones feeling it the most.

“Property investors are also feeling the heat though, because even though rents are increasing, they are not going up enough to cover the pace of interest rate hikes,” Mr Davis said.

He pointed out that as investors were deterred from holding or acquiring properties, the rental crisis could be exacerbated.

“If investors cannot continue to fund cash flow shortages on their properties, they will sell, and in most cases those properties get bought buy owner occupiers.

“With increasing interest rates there will be investors selling, which means less properties to rent, which means rents keep going up.”

Before this February rate hike, the number of mortgage holders considered ‘Extremely At Risk’, had increased to 666,000 (15.0 per cent).

Miriam Sandkuhler, CEO and Buyers Agent, Property Mavens, said interest rate rises will lead to more distressed property sales.

“Like Sydney, Melbourne’s trophy home section of the market has been hit hardest, with agents finding that selling multi-million dollar homes in areas like Brighton, Malvern and Toorak is much more difficult,” Ms Sandkuhler, the REIV Buyers Agent of the Year in 2021, said.

“But at the other end of the scale, some affordable options are doing comparatively well thanks to increased interest from budget-conscious buyers, including established 20th century apartments in inner and some middle suburbs and entry-level houses in middle to outer suburbs like Glenroy, Albion and Reservoir.

“Regional markets are also feeling the impact.

“The often over-estimated burst of new arrivals in 2020 and 2021 helped all regional markets, but the smaller centres are finding higher interest rates had led to a drop in buyer interest, which is biting hard.

“Larger regional centres like Ballarat, Bendigo and Geelong will weather this year much better and, in our opinion, are well placed to ride the next upturn in the cycle.”

Miriam Sandkuhler, CEO, Property Mavens

She also said renters were in for a hard time, with costs likely to soar another 10 per cent this as increased demand goes in search of for a decreasing number of listings, due to a return of international students, a slowdown in tenants becoming buyers and leaving rentals, and a drift of properties into the short-term accommodation market.

The RBA had a delicate balancing act to complete, according to Kristle Romero Cortés, Associate Professor at UNSW’s School of Banking and Finance.

“The RBA would reconcile the cost of living and the need to maintain price stability with potential gains from keeping interest rate levels low.

“Mortgage owners will absorb the increased costs, and historically on average in Australia, housing costs are not too different to normal.

“Extremely low rental vacancy rates may actually mean there will be fewer distressed sales, as homeowners may choose to rent their property out rather than sell it.

“Most likely there will be a decrease in spending and consumption, but that is the intention of the rate increases,” Ms Cortés said.

When will the rates pain be soothed?

There is a growing consensus that more interest rates rises are imminent, but opinion varies on whether it will be as few as one or as many as six.

Diana Mousina, Senior Economist, AMP Capital, said they expect inflation to fall to around 4 per cent by the end of the year, which is still above the RBA’s preferred band of 2-3 per cent.

Australian inflation looks to have peaked in the December quarter, which is later compared to our global peers.

“Australian prices lagged the initial rise in global inflation because wages growth in Australia has been lower compared to global counterparts, energy prices rose late in 2022 and flooding in eastern Australia resulted in additional upside pressure on food prices, Ms Mousina said.

“The RBA is better off pausing after the February meeting to assess the impacts of prior rate rises at a time when the inflation background is looking better.

“Rate hikes are working – housing prices are falling, lending growth is negative, credit growth is softening and consumer spending is weakening.

“Further rate rises risk slowing the economy too much,” she said.

Mr Davis, of Property Powerhouse, said he expects another two rate hikes of 0.25%, peaking at 3.85 per cent around June. He added that the national property market would subsequently stabilise two or three months later.

“The risk of distressed sales appears greatest in particularly in areas of high value mortgages, that being Sydney, Melbourne and Brisbane.”

Luke Parker, Director of OP Properties in Perth, said the interest rate peak was nearby.

“We are now seeing very real impacts on the economy the result of record rate rises and we know that rise takes about six months to actually flow through mortgages and the wider economy.

“The Reserve Bank needs to take some time to allow the full effect of rises to date to be known, as it’s much easier to tip the economy into recession than it is to kick start it again,” he said.

He pointed to employment and labour shortages as one of the underestimated factors in taming inflation.

“The elephant in the room with regards to the national inflation story is that the economy is beyond full employment, so it wants to grow but there isn’t the labour to support this growth.

“This means the cost of labour goes up because companies are poaching from each other, however, there is no actual increase in output, so everything just gets more expensive.

“It’s a pressure cooker.

“As the effect of increased overseas migration flows through the economy, the wheels will begin to turn again and this in itself will have a significant cooling effect on inflation.

“Hopefully, the record rate rises don’t completely crush investment by this time or else we’ll see a spike in unemployment and be in recession.”